Denison Mines

Denison Mines

My bet for the last uranium bull market

Disclaimer

LWS Financial Research is NOT a financial advisory service, nor is its author qualified to offer such services.

All content on this website and publications, as well as all communications from the author, are for educational and entertainment purposes only and under no circumstances, express or implied, should be considered financial, legal, or any other type of advice. Each individual should carry out their own analysis and make their own investment decisions.

Introduction and business model

Denison Mines is a uranium exploration company with assets in the Athabasca Basin in Canada. They own 95% of the Wheeler River project, the largest undeveloped deposit in this region, which, along with Australia and Kazakhstan, are the geographical areas with the highest amount of uranium worldwide.

I believe we are at the beginning (probably, a little beyond the beginning right now) of the last major uranium bull cycle, and Denison Mines is one of the most interesting investment ideas to take advantage of it. As with almost all explorers, the company's fundamental analysis has a short scope, beyond the study and valuation of its undeveloped assets, and what is truly interesting is understanding the macro landscape in which it operates.

Uranium: the last dance

The market balance outlook for uranium, from a commodity investor's standpoint, is the most positive I have come across to date, with all elements aligned for an explosive situation:

Tailwinds and significant demand growth.

Supply issues and massive deficits.

Significant catalysts in the form of secondary demand.

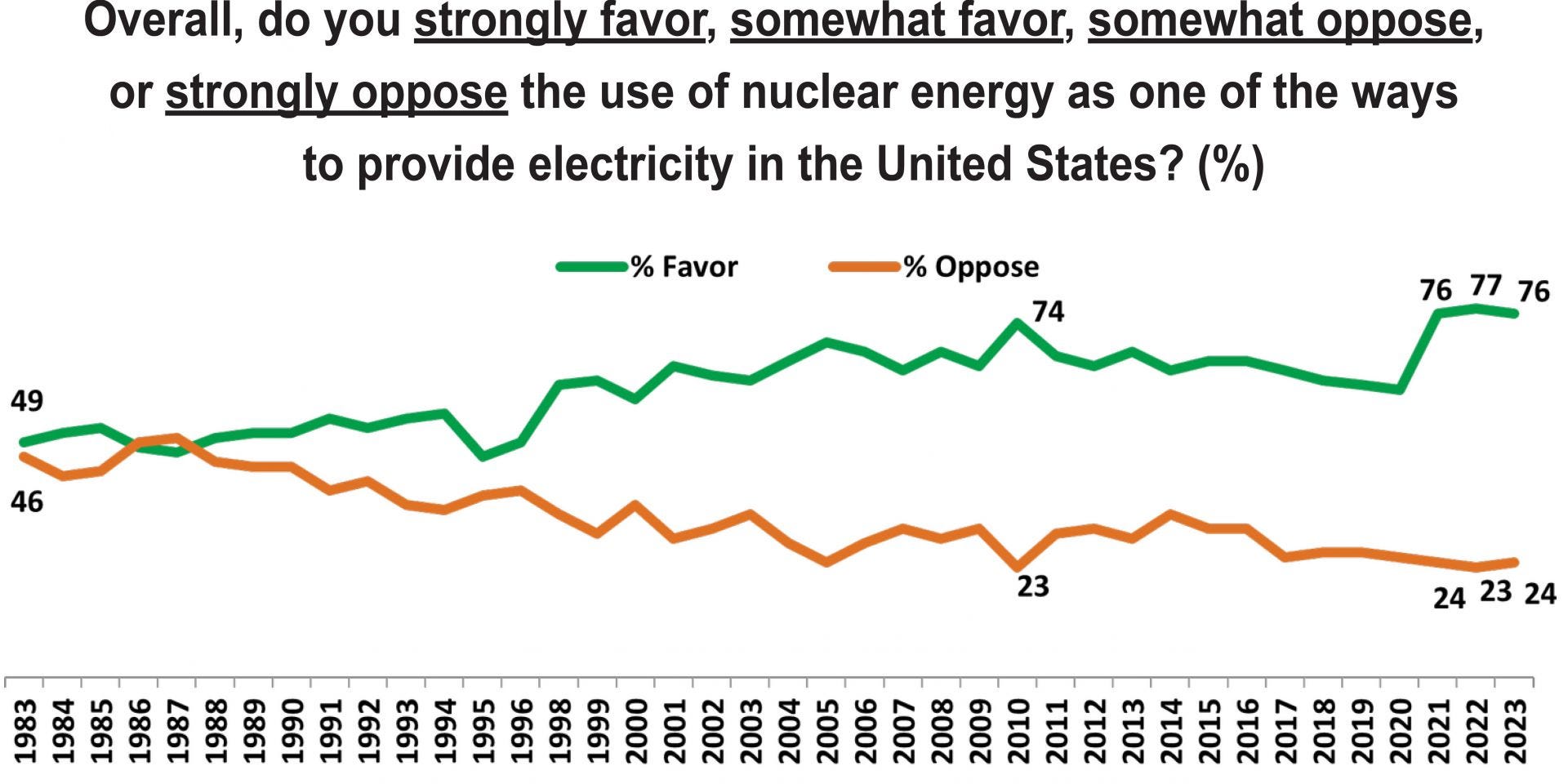

To understand the current situation and the derived prospects, it's interesting to first go back 20 years, to the previous nuclear bull cycle. In the early 2000s, a large amount of secondary supply, stemming from nuclear de-escalation after the end of the Cold War, posed a too heavy obstacle for nuclear demand, which, though growing, couldn't absorb such volumes, greatly limiting the development of new mines. In 2003, the flooding of McArthur River, one of the world's largest mines, was one of the first supply shocks of what was to come, which, combined with an explosion in reactor demand from China, initiated a major bull cycle where uranium prices reached $140/lb (inflation-adjusted, $183/lb).

The Great Financial Crisis and, above all, the Fukushima nuclear accident, ended this bullish period, curbing demand in a market balance with a lot of new supply, and uranium prices plummeted to levels where very few producers were profitable, creating a primary supply deficit compensated, as 20 years before, by secondary supply from Japanese inventories. Since 2011, the sector has operated in a constant decline, with no investor appetite. Everything began to change in 2018.

New nuclear spring

After the Fukushima accident, Japan, one of the biggest proponents of nuclear technology, shut down almost all of its reactors, and Europe and the United States, influenced by environmental lobbies (with a very poor understanding of reality, considering that nuclear energy should be the cornerstone of any reasonable decarbonization plan), also began a campaign to close operational plants, reducing the energy autonomy of both regions. On the other hand, China, India, and other non-OECD countries continued to push for nuclear capacity construction, helping to keep global demand levels afloat.

China remains the largest source of growth, and it is expected that over half of the 76 reactors under construction will be located in the Asian giant; the anticipated growth in demand implies consumption of 254 million pounds in 2025 (compared to the current 175 million pounds), and it is likely that the figures, as in recent years, will continue to surprise on the upside. Sentiment regarding nuclear energy is changing, and regions historically opposed to it, such as Germany, the United States, and other European countries, are now prioritizing energy security and economic efficiency, promoting the commissioning and reactivation of nuclear plants.

Extensions of the life of current reactors will require replenishing inventories, which are at least three times the annual consumption requirements, and the rest of the operational plants have been negligent in recent years, showing a complacent attitude towards weak prices, covering only 40% of their future needs

A multipolar world

The outbreak of war in Ukraine drastically changed the supply landscape, as the world seemed to split into two, with a clear separation between the Western bloc and the rest of the world, which took a much more neutral and accommodating stance regarding the armed conflict. The emergence of this multipolar world is especially relevant for the uranium market, since Russia operates 46% of the world's uranium enrichment capacity (the process of transforming the ore into nuclear fuel), and one of its satellite countries, Kazakhstan, is the leading producer of U308. Although these flows have not stopped due to sanctions (it seems that now the United States government wants to act on this front), the search for Western suppliers (with a focus on the enrichment process) has greatly increased the cost of these services in the past year. Whenever barriers and inefficiencies are created in a global commodities market, pressure on prices tends to rise, as energy security becomes more important than pure economic return.

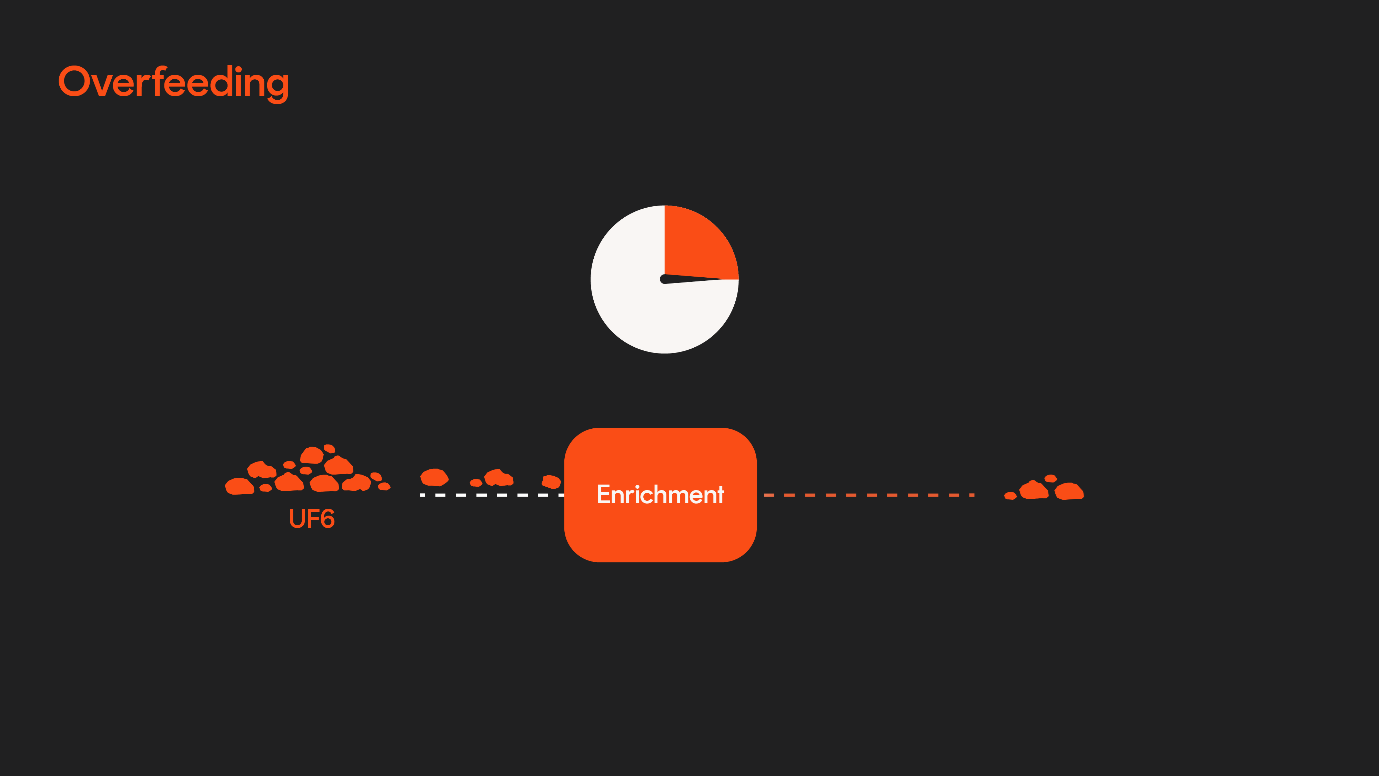

This disruption is deeper than it appears at first glance, as it is not only about a change of suppliers, but also affects total volumes, due to the concept of overfeeding. Initially, yellowcake, the resulting yellowish paste from ore grinding, is transformed into UF6, which then, through enrichment, becomes nuclear fuel; in recent decades, since there was excessive enrichment capacity, underfeeding was practiced, meaning less UF6 was provided to the process, but it was carried out for a longer period, making more use of the input and achieving the same result. Now, where enrichment capacity is scarce, we are likely to see the opposite, a situation of overfeeding, with shorter processes but more input material, which is estimated to add demand equivalent to 20M lb - 30M lb, that is, an additional demand of 11%-17%.

Market balance

In 2023, primary uranium production is estimated to have been 141 million pounds (+9% compared to 2022), while utilities' demand was 198 million pounds (+3% YoY), creating a primary deficit of 57 million pounds (29% of the market), which is unimaginable in any other commodity market, only sustained by the contribution of secondary supply, although both this and inventories show clear signs of exhaustion. Future projections, if anything, are much more worrying and require a giant increase in supply to prevent market breakdown.

The uncovered demand between 2024 and 2040 is 2.2 billion pounds of U308, and without adding new sources of production, the annual gap in that year would be 150 million pounds. One of the main bearish arguments for the sector was the theoretical infinite capacity of Kazatomprom to increase its production at will, thus preventing a sustainable bull market. However, this hypothesis has been practically discarded with the announcement of the main nuclear producer earlier this year: they greatly lowered their production guidance for 2024 due to lack of basic materials (specifically, sulfuric acid), and they will also do so for 2025, where the market consensus expected a strong increase in supply volumes. As always in the mining sector, which is one of the worst for most of the time, negative surprises are the norm, and supply is not very elastic over time (a new mine decided to start now would take about ~5 years to become operational), while surprises for demand remain positive.

Coupled with the tailwinds of demand we have already seen, the situation is explosive. At the recent climate summit in Dubai, this change in nuclear sentiment was reflected in the commitment of 20 of the wealthiest nations on the planet to triple their atomic capacity in the next 25 years, which further exacerbates the current projected deficit.

The lack of precise information on supply and demand (there is a lot of opacity around secondary supply and the actual inventories of utilities, for national security reasons) makes it difficult to make accurate predictions, but the rough numbers and main ideas are much clearer:

There is a large deficit in the market, and the tailwinds of demand are enormous.

New sources of supply require incentive prices of $75/lb.

Geopolitical uncertainty creates inefficiencies in the market.

As always in the mining sector, negative surprises and delays are common, and only add fuel to the fire.

Additional catalysts

A deficit market, no matter how significant, is not enough to generate investment opportunities, and often a catalyst is needed to ignite the first spark of the fire. In the case of uranium, it has been financial actors through uranium trusts.

These ETFs, popularized in 2021 with the launch of the Sprott Physical Uranium Trust, issue shares to purchase pounds of uranium that, in theory, remain locked away forever, and facilitate institutional investors in betting on physical material. They compete with traditional uranium clients, reducing effective supply, and their effect on the price has been clear so far.

Following the success of Sprott and Yellow Cake, we have seen the launch of several additional funds (ANU, UAMC, PFYN...), and they are creating a virtuous circle (flywheel effect) as the spot price increases. They represent a non-negligible percentage of the annual supply, with an average annual demand of 20M lb (out of 150M lb of total supply).

Market interest

During the year 2023, the spot price of uranium rose from $48/lb to $91/lb (it continued to grow in early 2024), surpassing the estimated incentive price to encourage new supply, which is around $80/lb. However, sector stocks have generally lagged behind this 90% increase. Despite the significant increases in the past two years and the spectacular macroeconomic and market environment, as we have seen, investor interest is still very low, and in my opinion, the opportunity and potential still exist. Some specialized consulting firms, such as Haywood, are beginning to update their tables and valuations, and they are already assuming equilibrium spot prices of $85+/lb, which would leave very interesting potentials in the main companies of the sector.

The last dance

Although the fundamentals of the sector are spectacular, and everything seems to indicate that the cycle still has room to run, some recent technological developments point to a material disruption in the fundamentals, which could render uranium mining obsolete, despite the success of nuclear energy. Specifically, the two advances that concern me the most are:

Implementation of fourth-generation reactors, which are capable of utilizing the entirety of supplied nuclear fuel, unlike current ones, and therefore could recycle nuclear waste created to date to operate for decades, greatly reducing the need for fissionable material.

New fuels and technologies, such as thorium reactors, which have already been used satisfactorily (and more efficiently than those based on the uranium cycle) on a small scale and in experimental settings.

At the moment, these are not imminent threats, and they would become operational by the end of this decade, so they will not have an effect on this cycle.

If this is indeed the last major uranium bull cycle, we are going to try to make the most of it. The last dance.

Investment thesis

Once the uranium market balance is understood, it is not straightforward to translate it into a conservative investment idea, as there are only two reasonable options for publicly traded producers already in operation (there are more options, such as CGN, BHP, or Paladin, but their jurisdiction, size, or product focus do not make them as attractive):

Cameco

Kazatomprom

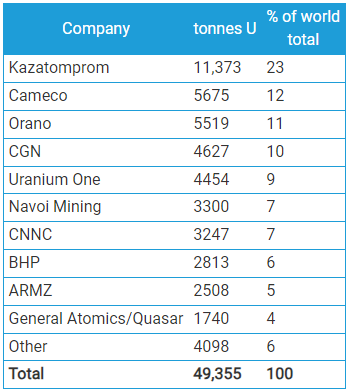

Between these two companies, they account for 35% of the world's uranium production. Due to Kazakhstan's political alignment, a country politically close to Russia, the most reasonable option for a Western investor is Cameco. However, its valuation and recent restructuring, becoming a full-cycle company, more akin to a utility than a miner, make it less attractive.

In this context, Denison offers a good balance between potential and security, and next, we will see the main points on which this investment thesis is based.

Keep reading with a 7-day free trial

Subscribe to LWS Financial Research to keep reading this post and get 7 days of free access to the full post archives.