G&R Q124 analysis

G&R Q124 analysis

On LNG, AI and natural gas supply

Disclaimer

LWS Financial Research is NOT a financial advisory service, nor is its author qualified to offer such services.

All content on this website and publications, as well as all communications from the author, are for educational and entertainment purposes only and under no circumstances, express or implied, should be considered financial, legal, or any other type of advice. Each individual should carry out their own analysis and make their own investment decisions.

In this deep dive, we are going to analyze the Q124 commentary from Goehring & Rozencwajg, an American investment firm specializing in commodities, known for their very interesting and groundbreaking perspectives. In this instance, they delve into the natural gas thesis, the shift from structural surplus to deficit in the American market, and the potential impact of AI on the demand for this commodity.

In these commentaries, which they publish once a quarter, they tend to present an excessively optimistic bias, especially regarding timing, so it is important to critically evaluate their statements. Their data and theses are original and groundbreaking, and I have the sense that the market operates independently of the conclusions they offer, which I consider valid. Therefore, it is crucial to understand and apply them.

LNG, AI and natural gas

In their Q120 letter, G&R predicted the beginning of a massive bull market for natural gas, which finally materialized in the summer of 2022 (timing…) when Henry Hub gas prices multiplied by 6x due to Russia's invasion of Ukraine (not for the reasons they had anticipated). However, two consecutive warm winters and a fire at a Freeport export facility reversed this bullish trend. Everything points to the fact that, this time, we are indeed on the verge of the long-awaited bull market for natural gas.

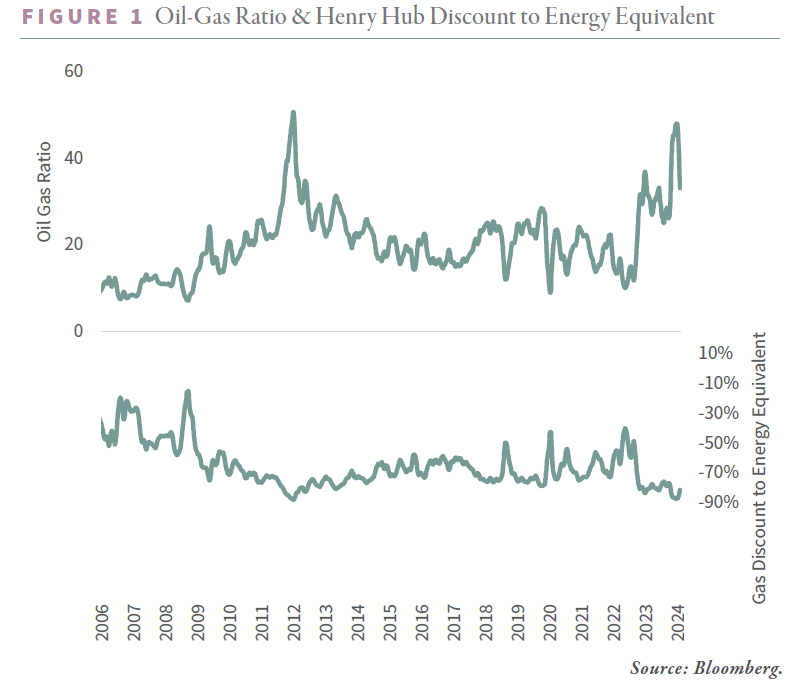

Currently, Henry Hub gas is the cheapest energy molecule on the planet, trading at a 90% discount to its energy equivalent in oil.

Historical context

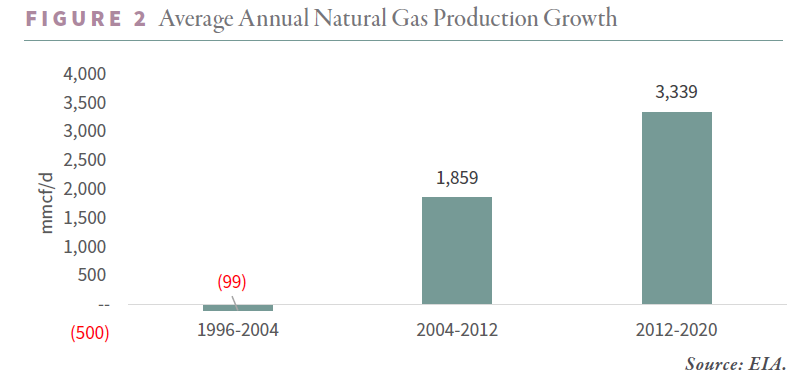

Gas production in the U.S. experienced an unprecedented boom due to the shale revolution. Between 2012 and 2020, gas supply grew significantly, surpassing 32 bcf/d. However, conventional production continued to decline by 32% during the same period. This growth was primarily driven by the Marcellus, Haynesville, and Permian fields, where productivity has significantly decreased in recent years. This explosion of growth could not be absorbed by the country’s domestic consumption, and due to the lack of necessary infrastructure to export the surplus, prices collapsed; it seems that the growth of the shale basins is rapidly slowing down.

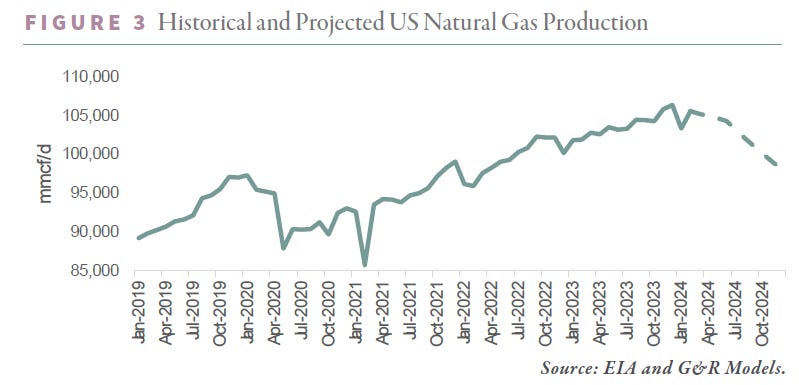

Bearish sentiment peaked in the first quarter of 2024. A warmer-than-normal North American winter reduced heating demand and pushed gas prices down, reaching a low of $1.48 per mcf in March 2024.

Outlook

Their models indicate that gas reserves could be depleted more quickly than anticipated. Despite the EIA forecasting a recovery in U.S. dry gas production in 2025, reaching a new all-time high of 105 bcf/d, they consider this prediction too optimistic. The capacity of LNG terminals is a critical factor. LNG exports are expected to increase significantly in the next 18 months with new projects coming online, bringing total exports to 20.4 bcf/d by mid-2027. To meet the EIA's forecasts, shale fields would need to reverse their declining trend and add 1 bcf/d each month over the next year; at the same time, the agency expects an average price of $3.1/mcf during 2025, 46% less than in 2022, where growth was only 380 mmcf/d per month, highlighting how unrealistic these forecasts are. In fact, in their latest STEO analysis, this same organization already predicted a 1% year-over-year decline in production in 2024; for this to happen, production must fall by 7 bcf/d by the end of the year.

In addition to export demand, domestic gas consumption for electricity generation will increase significantly, driven by the proliferation of data centers and artificial intelligence. It is estimated that AI data centers in the U.S. will consume 400 TWh of electricity, requiring seven bcf/d of natural gas. This growth would represent the largest increase in gas-fired power generation capacity in U.S. history. To meet this development, there are three options available: coal, nuclear energy, and natural gas; the improbability of the first alternative and the long development time associated with nuclear reactors make natural gas the ideal candidate.

Natural gas demand in the U.S. is set to grow at the fastest rate in history until 2030, while gas production appears to have peaked. Although some analysts are optimistic about a recovery, they share a more cautious view. The shale gas revolution has resulted in a dramatic increase in supply, but immense does not mean infinite. We are in the early stages of a possible production decline, and the market will need to adjust accordingly.

Oil

Keep reading with a 7-day free trial

Subscribe to LWS Financial Research to keep reading this post and get 7 days of free access to the full post archives.