G&R Q323 analysis

Disclaimer

kairoscap is NOT a financial advisory service, nor is its author qualified to offer such services.

All content on this website and publications, as well as all communications from the author, are for educational and entertainment purposes only and under no circumstances, express or implied, should be considered financial, legal, or any other type of advice. Each individual should carry out their own analysis and make their own investment decisions.

In this deep dive, we are going to analyze the Q323 commentary of Goehring&Rozencwajg, an American investment firm specialized in commodities, which always has a very interesting and groundbreaking vision. In this case, they delve into the thesis of energy consumption and the energy demand curve and what to expect in the coming quarters in the natural gas, copper, gold, fertilizers and grains markets. This installment is one of the most interesting so far, and some of its ideas will have a significant influence on our positioning for 2024.

The magnificent seven (Microsoft, Apple, Amazon, Alphabet, Nvidia, Meta and Tesla) dominate the headlines, indices and performance tables, and owning these names has become mandatory to survive, as a fund manager, in today's world. Between them, they comprise almost 30% of the S&P500 and determine its performance; on the other side of the spectrum, if a manager considers the energy sector, it is almost always to bet against it, and that, according to the consensus (e.g. the IEA's benchmark World Energy Outlook reports), there is going to be a dramatic decline in its consumption and importance, accentuated even more so in the case of fossil fuels. Despite having vastly outperformed technology stocks since 2020, their aggregate weight is less than 5%, whereas historically their weighting has been 14%.

The Jevons Paradox

In 1865, an English economist, William Stanley Jevons, formulated a theory (which gives its name to his paradox), which has since been proven, and which is being ignored by the IEA and its faithful in its forecasts: efficiency gains translate into higher energy demand. Jevons had observed how improvements in steam engine efficiency translated into higher coal consumption, and deduced that technological improvements drove its adoption (increased use) and, in addition, allowed for an acceleration of economic growth, further spurring demand. This side of the balance, unlike supply, is very difficult to model, as it depends on how societies evolve, regions urbanize and individuals consume, yet it is a critical element in addressing the future.

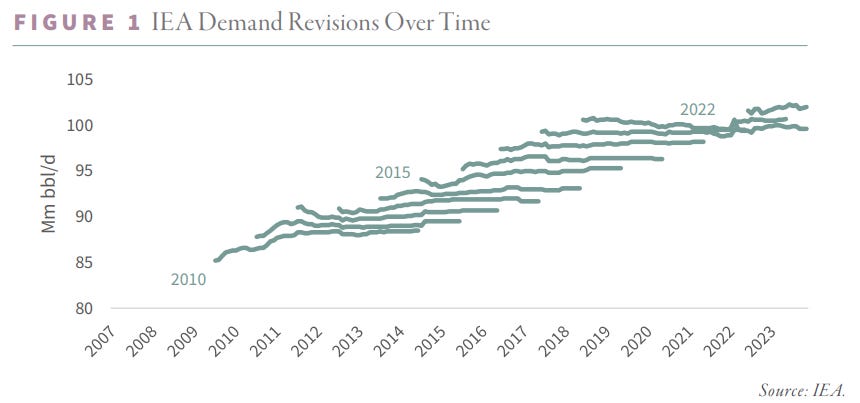

The IEA, in fact, has a history of being extremely pessimistic in its forecasts: out of the last 14 years, it has underestimated demand in 12 of them (by an average of 820kb/d, a real barbarity). G&R believe that this time they are wrong again, and that their forecast for the phasing of fossil fuels in this decade is wrong and has important implications for markets.

The IEA estimates that total energy demand will fall by 1% (from 2022 levels) by 2030, rising to 3.2% by 2040, which is impossible with a reasonable analysis of energy consumption and trends. Energy intensity (energy required to generate $1 of GDP) has improved dramatically from 1965 (13MJ/1$) to 2022 (7MJ/1$), a reduction of 40% (1% per year); now, the IEA expects this trend to accelerate dramatically, and energy intensity to start falling at 3% per year, dropping by almost half by 2040. From this premise, which G&R considers erroneous, derive all the conclusions on the reduction of energy consumption, which are the basis for the pessimism surrounding energy companies in the markets.

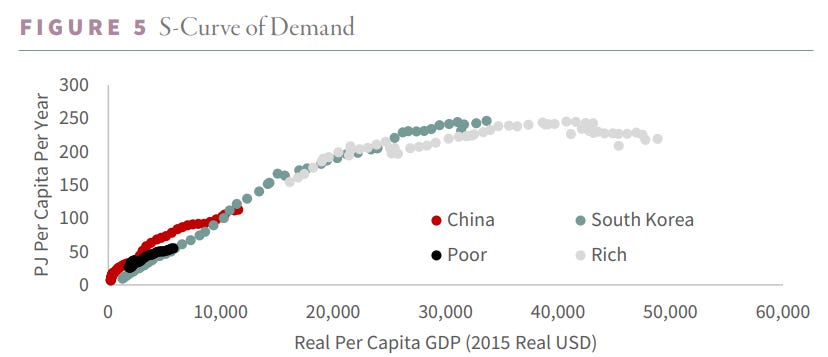

The IEA seems to be overlooking the biggest growth driver for energy demand: the rise of emerging markets. For decades, they have represented a low (30%) and constant percentage of world GDP, but in recent years their growth has accelerated, and they now account for 45% (soon to exceed 50%), which has a gigantic effect on the energy consumption S-curve: as an economy increases its GDP per capita, its demand profile forms an S, with the saturation point around $25k/year. When a country has a figure below $5,000/year it is irrelevant, but between $5k-20k/year it enters the sweet spot, where increases are more material, as this is where the middle class is growing the most; a third of the world's population is now in this phase, and the effect this is going to have on demand growth is not being well calibrated.

Renewable energy: the biggest malinvestment in history

At the end of 2021, G&R predicted that the huge amount of capital being poured into renewables would, in the future, be seen as the biggest malinvestment in history. Three years later, the market seems to be proving them right: in recent months, several companies involved in wind and solar energy have gone bankrupt or are applying for subsidies worth millions to make their operations profitable, while many projects that only made sense in an artificial zero-rate environment are being cancelled.

Keep reading with a 7-day free trial

Subscribe to LWS Financial Research to keep reading this post and get 7 days of free access to the full post archives.