Gulf Keystone Petroleum

Gulf Keystone Petroleum

Open the gates

Disclaimer

LWS Financial Research is NOT a financial advisory service, nor is its author qualified to offer such services.

All content on this website and publications, as well as all communications from the author, are for educational and entertainment purposes only and under no circumstances, express or implied, should be considered financial, legal, or any other type of advice. Each individual should carry out their own analysis and make their own investment decisions.

Introduction and business model

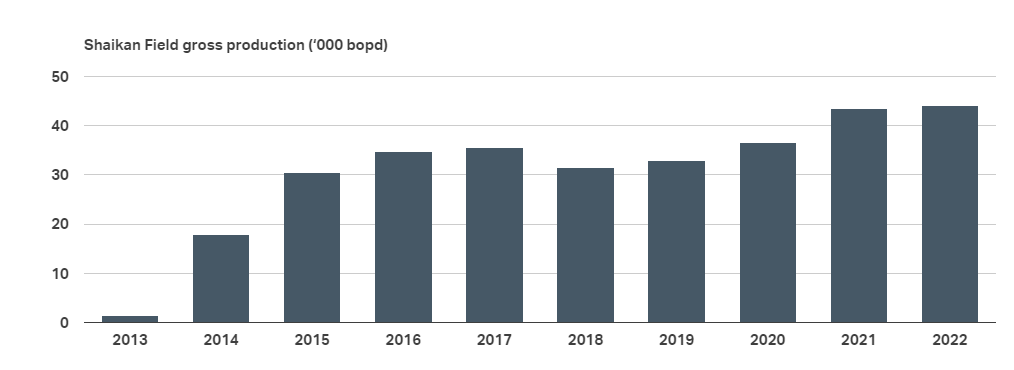

Gulf Keystone Petroleum (GKP) is an oil and gas operator with assets (Shaikan) in the Iraqi Kurdistan region. The company began commercial production at this field, which is one of the largest in the region, in 2013, and since then they have scaled operations and created incredible value for shareholders. Their equity in Shaikan is 80%, and with the 2022 production figures (44.2k boe/d), they estimate that the field's reserves would cover 28 years of exploitation.

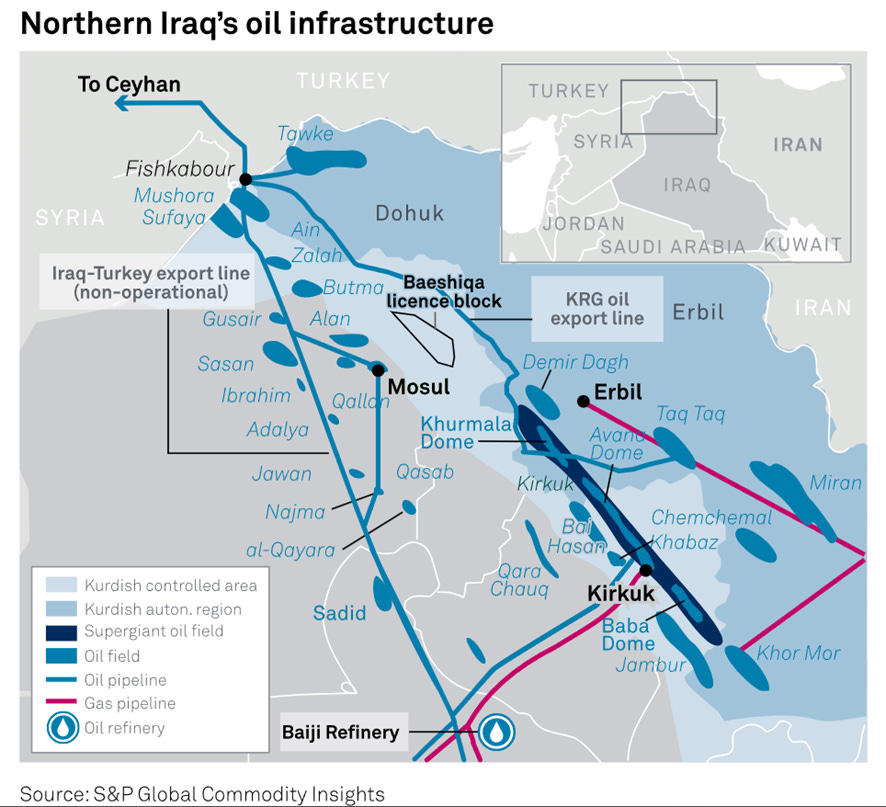

The commercialization of their product was conducted through the Iraq-Turkey Pipeline (ITP), a pipeline that connected Erbil, the capital of the region, with the port of Ceyhan, which, as we will see later, has been the subject of dispute and political conflict in recent years.

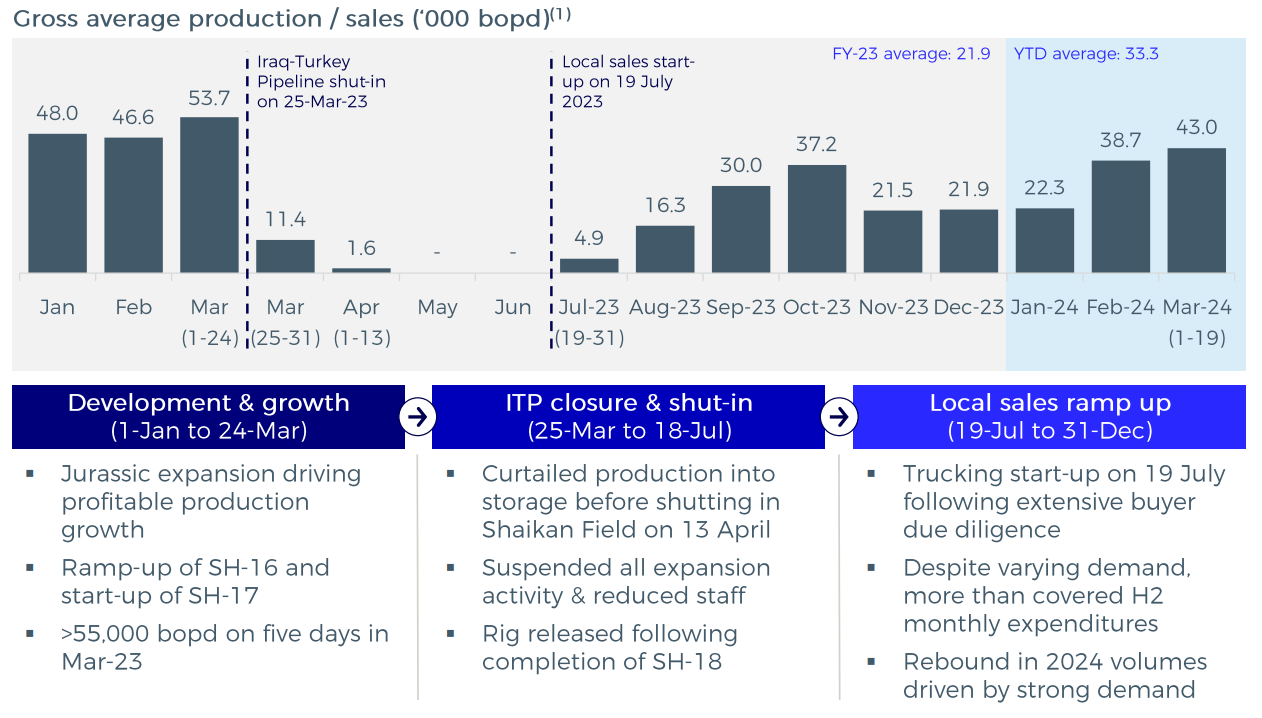

GKP's strategy, until last year, had a clear focus on growth, with an ambitious drilling and ramp-up campaign that allowed them to reach 55k boe/d of production in March 2023. However, this was abruptly and traumatically disrupted on March 25th last year. With the ruling of the International Chamber of Commerce in favor of Iraq (again, more details later), the flow through the ITP dried up, causing a total disruption of GKP's operations. Shaikan was completely shut down on April 13th, and all expansion activities were quickly reduced to cut expenses and preserve liquidity. Since then, they have managed to redirect part of their volumes to the local market, although the selling prices are much lower (~$28/b).

What can we expect from now on in terms of production, price, and shareholder return for $GKP?

Investment thesis

To understand the investment idea of Gulf Keystone Petroleum, we will focus, as we always do, on the main drivers of value creation. Specifically, the main aspects influencing the valuation and its realization are as follows:

Geopolitical context

Operations and financials

Balance sheet

Shareholder returns

Let's dive in.

Geopolitical context

To address this complex aspect, which is crucial for this investment idea, we have the genuine privilege of collaborating with Aleix Amorós (@aleix_amoros), one of the best geopolitical analysts and a regular contributor to our Discord. I extend my gratitude and recognition for his generosity. The following content has been entirely prepared by him and serves as an ideal framework for evaluating the possibilities, obstacles, and timings of conflict resolution.

Irak, lights and shadows

Few regions in the world are more volatile and complex than Kurdistan. This transnational territory, which spans up to four countries south of the Transcaucasia, is home to the largest stateless community on the planet, composed of more than 25 million people.

Historically, the nationalist aspirations of the Kurdish people have been fiercely persecuted and combated by their host nations, especially in Turkey. Ankara has been involved in a low-intensity asymmetric war with the Kurdistan Workers' Party (PKK), the armed wing of the Kurdistan Communities Union and the main Kurdish party in the country, since 1978, leaving more than 40,000 dead to date. This situation similarly echoes in northern Iran and in the eastern bed of the Euphrates in Syria, where Kurdish communities mostly coexist marginalized by the state.

The only example of certain prosperity and territorial consolidation at all levels has occurred in Iraq, whose capital, Erbil, performs all pertinent administrative functions. The case of Iraqi Kurdistan is certainly peculiar, as it enjoys a unique semi-autonomous status in the region and has managed to maintain good relations with the central government in Baghdad. Additionally, it played a key role in expelling the Islamic State from the north of the country in the mid-2010s through its defense forces, the Peshmerga, earning them not only internal recognition but also that of important international supporters such as the United States.

The nexus of this romance between Erbil and Baghdad, in any case, does not lie so much in good intentions or social identity, but in something much more primary—and profitable—oil. It is estimated that there are still about 45 billion barrels of reserves in this region, which, to put these figures in perspective, is more than four times the discoveries in Guyana in recent years, which have been the largest new proven reserves found in decades.

Until 2014, and despite Iraq's tumultuous contemporary history, the business was running smoothly. The prolific fields around the Kirkuk governorate attracted the attention of numerous foreign companies, which settled in the Kurdistan Regional Government (KRG) and energized the local economy. The bulk of the production was then sent to the city of Baiji through a pipeline, and from there it flowed to Fishkabour, the last enclave on Iraqi soil before crossing the Turkish border. Ultimately, the branch on the other side of the border extended to the port of Ceyhan on the Eastern Mediterranean, thus allowing the crude to reach international markets. The State Organization for Marketing of Oil (SOMO) handled the transportation and mediation between the parties, ensuring that producers operating in the KRG paid the respective tolls and royalties to the central government. It was, in essence, a non-zero-sum arrangement, benefiting all parties.

The emergence of the Islamic State in Iraq in January 2014 turned the status quo upside down. Fallujah, near the capital, was the first city to fall, and from there the Islamist group spread like wildfire through much of the country. On June 10, the insurgents managed to take control of Mosul, Iraq's second-largest city, after less than a week of fighting. In this situation, and anticipating a collapse of the central administration, the Peshmerga captured Kirkuk two days later. Between June 17 and 18, the Islamic State launched offensives against the city, but they were successfully repelled. Despite this feat, the transportation of oil through the Kirkuk-Ceyhan pipeline was completely disrupted, among other things due to significant damage to the infrastructure.

It so happens that in May 2012, the Turkish government and its counterpart in Erbil reached an agreement for the construction of a gas pipeline and two oil pipelines directly from the Kurdistan Regional Government to Turkey without Baghdad's approval, thus cementing the rapprochement that began between the two in 2009.

As a result, during the second half of 2014, operations began on the first—and to date only—alternative pipeline that was built. This pipeline also converged in the town of Fishkabour, where it connected to the main branch, thus bypassing SOMO’s supervision and enhancing trade between Iraqi Kurdistan and neighboring Turkey.

Baghdad did not stand idly by. Immediately after the first shipment of crude oil through the new pipeline, it initiated arbitration proceedings against Turkey at the International Chamber of Commerce (ICC). This Paris-based organization ruled in favor of Iraq on March 23, 2023, stating that the country led by Recep Tayyip Erdoğan’s government had breached the agreements signed in 1973 regarding the Kirkuk-Ceyhan pipeline. The ICC imposed a $1.5 billion fine for the damages caused between 2014 and 2018. The next day, oil flows from Iraqi Kurdistan ceased completely after Turkey shut down the pipeline, thus expressing its disagreement with the court's verdict.

Fifteen months have passed since then, and the situation remains stalled. There are many interests at stake, often antagonistic to each other, which only complicates a potential negotiated resolution. Moreover, the tribunal's ruling was not made public, further complicating the verification of the various parties' claims about the content of the judgment.

Turkey, an uncomfortable but necessary partner

Starting with Turkey, the government distanced itself from the outset from the International Chamber of Commerce's ruling, which pointed to it as the main party responsible for the dispute by having improperly allowed the Kurdistan Regional Government to independently commercialize and export its crude oil outside of SOMO’s supervision. Ankara justified the unilateral cessation by citing force majeure, resulting from the damages caused by the strong 7.8 magnitude earthquake that struck northern Syria and southern Turkey on February 6, 2023, thus avoiding potential claims for breach of contracts with the private contractors operating in Iraqi Kurdistan.

Keep reading with a 7-day free trial

Subscribe to LWS Financial Research to keep reading this post and get 7 days of free access to the full post archives.