Warrior Met Coal

Disclaimer

kairoscap is NOT a financial advisory service, nor is its author qualified to offer such services.

All content on this website and publications, as well as all communications from the author, are for educational and entertainment purposes only and under no circumstances, express or implied, should be considered financial, legal, or any other type of advice. Each individual should carry out their own analysis and make their own investment decisions.

Introduction and business model

Warrior Met Coal is a metallurgical coal mining company located in Brookwood, Alabama. They have two producing assets, Mines 4 and 7, with combined capacity of 8Mt per year, and with 89Mt of reserves and 25 years of life under the current scheme. As we saw in the article on Alpha Metallurgical Resources, one of their competitors, their product is a critical component (and with no economically viable technological substitute, at the moment) in steelmaking.

In fact, in the recent EIA report, which already incorporates an important political bias in its methodology and conclusions, under its base projection scenario (STEPS), they assume that the demand for metallurgical coal will remain stable until 2050, so there seems to be no terminal value risk in the short and medium term.

As a second derivative, steel will continue to play a key role in economic development and benefits from many of the emerging megatrends: population growth and economic development in Asia and Africa, construction and maintenance of housing and infrastructure, energy transition and electric vehicles... This fact is known and shared by most governments, and the pressure for its phase-out is very low (until an economically and technologically viable alternative appears), unlike for thermal coal.

As we introduced at the beginning, it has two assets in production, and is developing a third one that, once in operation, will be the jewel in the crown (in this sense, if you follow the oil&gas space, it has a profile similar to that of $IPCO). Specifically, its assets produce the highest quality metallurgical coal (HCC), and are:

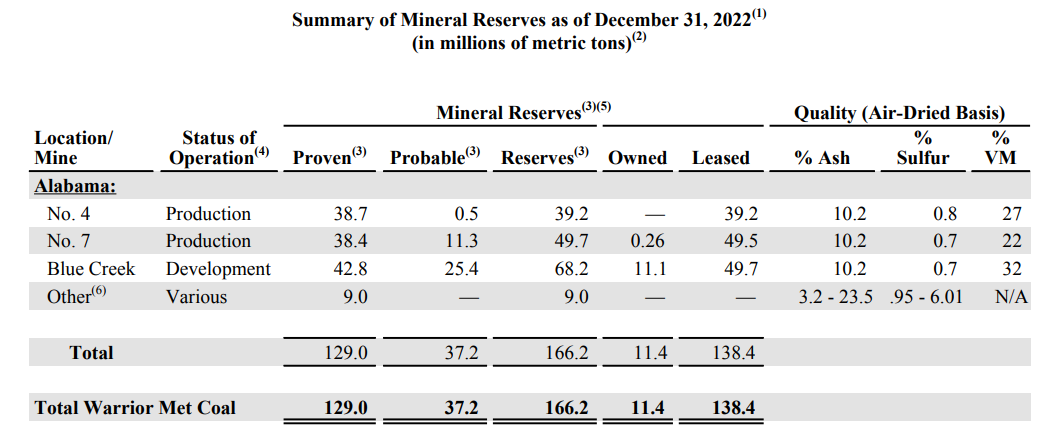

Mine 4: It began operations in 1974, under the control of Jim Walter Resources, and Warrior acquired it in 2016, following the 2015 bankruptcy of Walter Energy. It has a maximum production capacity of 2.4Mt per year, and 39.2Mt in reserves.

Mine 7: It has a maximum production capacity of 5.6Mt per year and 49.7Mt in reserves. Its product is sold at a premium compared to the rest of the coal specifications produced in the USA.

Blue Creek: It is one of the few high-vol A metallurgical coal deposits still undeveloped. It is expected to produce 4.8Mt per year, and has reserves of 68.2Mt. In addition to the defined reserves, they have 38.2Mt of resources, bringing the total to 107.4Mt, which, with the development they are carrying out, would allow them to operate the mine for 30 years (additionally, they see potential for expansion through exploration, which could extend the life of the asset up to 40 years).

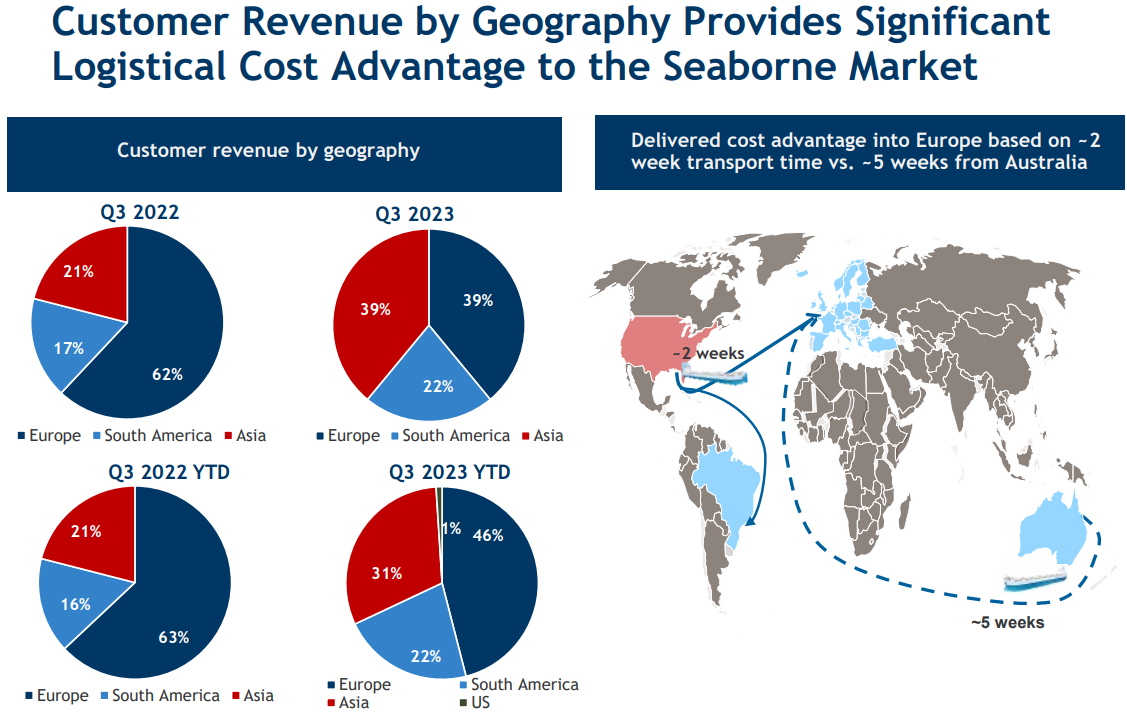

The coal they produce is processed in plants they own, and both mines (and Blue Creek as well) are about 300 miles away from their export terminal (in Mobile, Alabama); this proximity to the port and logistical flexibility gives them a cost advantage over other US competitors. They are a pure play metallurgical coal company, and the contribution of the thermal segment is negligible; the quality of their coal and their location makes them an ideal exporter, with access to all major demand centers (Europe, South America, USA and Asia), and gives them flexibility to rebalance those routes in a short time: last year, 63% of their product was exported to Europe, but with the economic weakness of the old continent in 2023, they have moved much of their exports to Asia, where demand is being much more resilient.

Despite the quality of their product, which in many cases is sold at a premium over the indices, their commercial relationships are usually through medium-term contracts (1-3 years), which they close well in advance, which sometimes prevents them from capturing all the upside of the spot market (also, of course, protects the downside if there is weakness in prices), especially if there are sudden and aggressive rises such as those of recent months.

Investment thesis

As I have made public on several occasions, I am very bullish on the metallurgical coal industry, and it has been my main position over the last year. Specifically, my main bet (and portfolio position) was AMR 0.00%↑ , which seemed to me to be the best vehicle to play this idea, in that its shareholder return program and balance sheet are unparalleled; however, after rising over 60%, the risk/reward profile is no longer as attractive, so other options seem more interesting to me. Next, let's review all the key points of the $HCC investment thesis.

Keep reading with a 7-day free trial

Subscribe to LWS Financial Research to keep reading this post and get 7 days of free access to the full post archives.