Weekly summary 04/05

Weekly summary 04/05

The worse it gets, the better

Disclaimer

LWS Financial Research is NOT a financial advisory service, nor is its author qualified to offer such services.

All content on this website and publications, as well as all communications from the author, are for educational and entertainment purposes only and under no circumstances, express or implied, should be considered financial, legal, or any other type of advice. Each individual should carry out their own analysis and make their own investment decisions.

The Q124 earnings presentation season has already begun for our portfolio, and it has come loaded in its first week. Tomorrow you will receive the first analysis publication of these presentations (and conference calls), where we will provide coverage for all the companies in the model portfolio and others that, although not included, belong to the tracking universe of LWS Financial Research.

Weekly macro summary

There have also been quite a few interesting events to analyze, and below I list the most noteworthy news. Let's get started:

The May FED meeting (and subsequent press conference) were extremely uneventful. The governors decided to keep the benchmark interest rates unchanged, and the same messages as always were repeated: they will not lower rates until they have more confidence that inflation is progressing in the right direction, and they do not yet see enough deterioration in the economy to justify this first mandate. In fact, the only relief for the stock market was the acknowledgment (logical, on the other hand) that they were not considering further rate hikes.

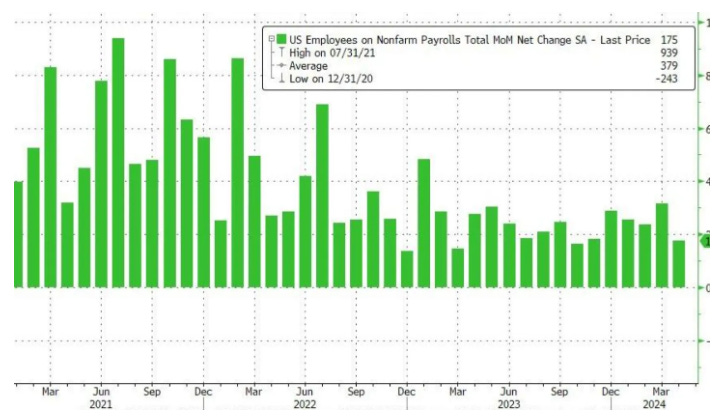

However, on Friday, a weaker-than-expected employment report (only 175,000 jobs were added in April) once again put the ball in the FED's court, giving them an excuse and cover to carry out the actions they really want to take, namely, to cut rates before the presidential elections in November.

Following this jobs report, interest rate futures are already forecasting 2 rate cuts in the year, bringing forward the first one to September. Although it is an improvement (for the conditions of restrictive monetary policy) compared to the beginning of the week, expectations have collapsed from the market's initial bet of 7 rate cuts for 2024.

In this case, it seems that the worse, the better, as any negative economic data appears to bring rate cuts closer, which is the major event eagerly awaited by the market.

The US Senate has formalized the ban on importing Russian uranium, which until now accounted for 25% of American volumes. Unlike with oil, these sanctions will be difficult to evade, as the traceability and monitoring of the product are much more comprehensive, thus complicating the supply landscape for the OECD significantly. To add fuel to the fire, we had the earnings report this week from the world's second-largest uranium producer, Cameco, which once again disappointed:

The achieved sales prices were very low ($55/lb vs. $90/lb in the spot market), confirming that their strategy of hurriedly signing contracts during the low point of the cycle was incorrect. Since the existing contracts entail volumes greater than what they produce, they will need to be a net buyer in the market to fulfill their commitments. Everything is going wrong.

Production at their Canadian assets met expectations, but not their joint venture with Kazatomprom (Inkai), which seems unlikely to reach its annual guidance, and with supply problems of sulfuric acid from the Kazakh giant, it seems it won't be an easily solvable obstacle.

Despite these difficulties, several countries, such as Italy or the United States itself, are considering reactivating (once again) nuclear power plants they had decided to shut down, underscoring the triumph of reason over politics.

The parliament of Georgia has approved, in the first round (two more confirmations will be needed to formalize it), the law on foreign agents, which has sparked strong protests in a country that is deeply divided and politically polarized, between those in favor of closer ties with the West and those in favor of maintaining a pro-Soviet culture.

With this law, perceived by Washington and Brussels as a move towards Moscow, organizations that receive more than 20% of their funding from foreign sources will be required to declare it publicly, in order to monitor their activities and influence more closely. Of course, any protest, especially when it pits two equally populous sides against each other, runs a great risk of escalation, but the reaction of the stock markets seems exaggerated to me for an event of little real impact, beyond market sentiment.

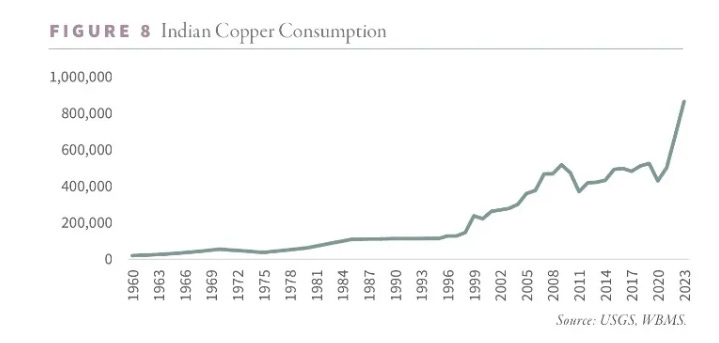

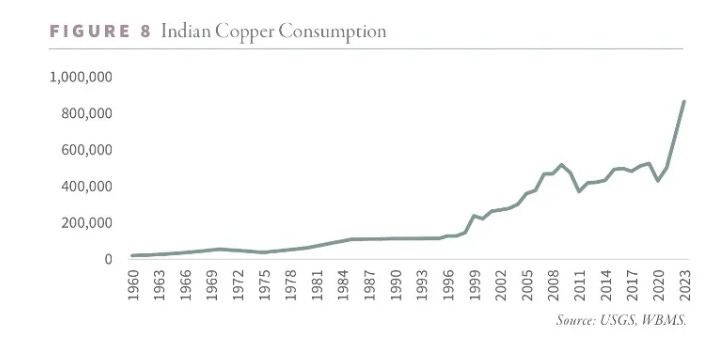

The growth of renewable energy and the electrification of the economy are driving demand for copper in a market context of deficit, where forecasts already point to a giant and growing shortfall. Some countries, like India, are offsetting the weakness of China and registering very significant growth as their economy expands.

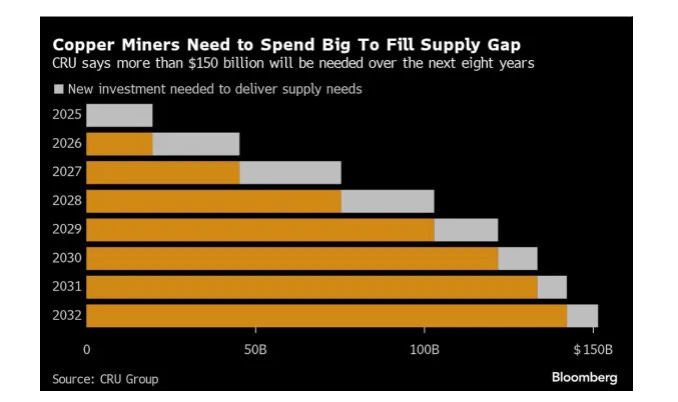

The easily accessible and higher-grade deposits have already been exploited (at least those identified with current technology), and the remaining greenfield projects are associated with higher costs and regulatory hurdles, which suggests higher prices in the short term. In fact, to meet demand estimates, it is calculated that an investment of $150 billion will be necessary over the next 8 years.

For the more optimistic, data from countries like Sweden, where the pause in interest rate policy has been sufficient to provoke a reacceleration in manufacturing and industrial indices, suggests a positive contribution from Europe and the United States as monetary policy in both blocs loosens.

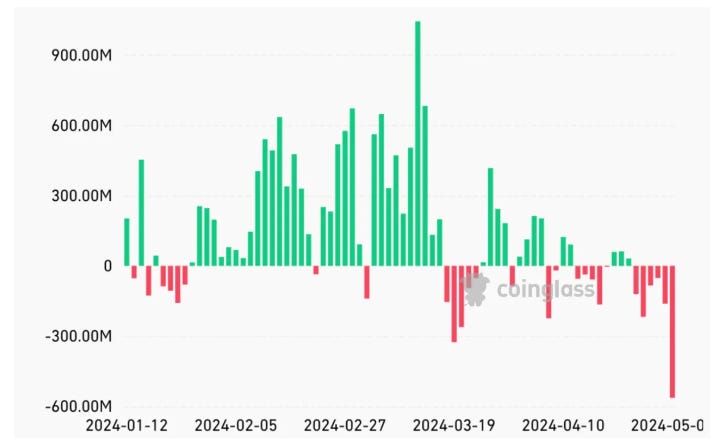

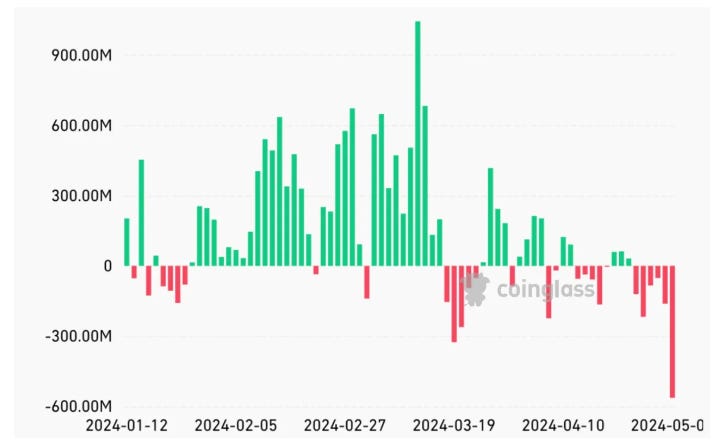

As we warned a few months ago, Bitcoin ETFs, although very positive in the long term as they open a gateway for institutional investors who were previously excluded from the market, can be a double-edged sword, helping to amplify downward movements in the short term as well. Over the last month and a half, with the exception of some sporadic days of positive capital flows, there has been a constant outflow of capital from these vehicles, which has weighed heavily on the price of the orange asset. As expected, the halving has added short-term selling pressure, causing a negative effect on price and sentiment, but it is a giant supply shock (-50%), which will be a huge tailwind in the medium and long term.

After the mandatory 3-month waiting period following its launch, new institutional investors are beginning to arrive with an appetite for exposure to these ETFs, such as the bank BNP Paribas, which has started to add shares of $IBIT. Registered Independent Advisors (RIA) are also starting to come in.

Meanwhile, the mysterious agent (likely an as yet unidentified state) popularly known as Mr. 100 (due to the standard size of his purchases) returned to market-buy BTC on Thursday, accumulating a total of 4,000 BTC worth $240 million, which is 9 times the new daily supply produced.

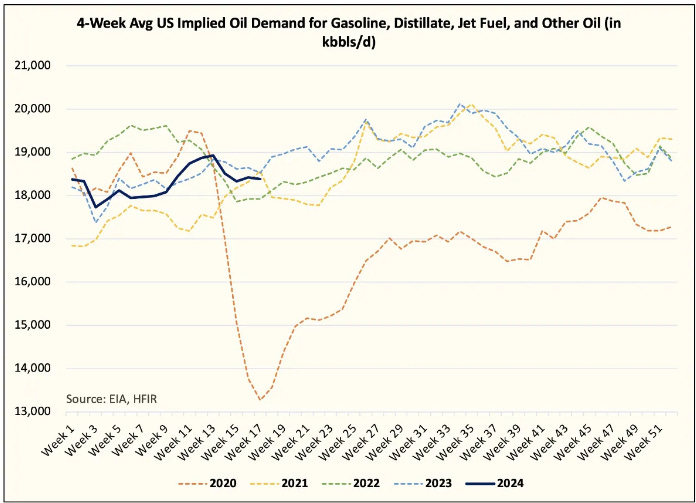

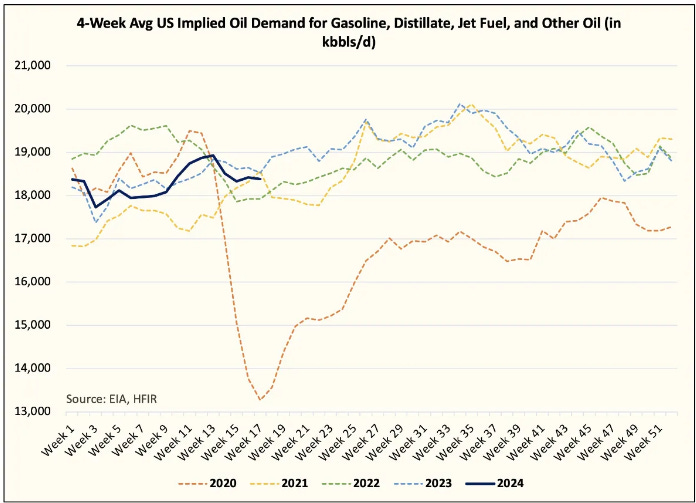

After last week's positive oil inventory report from the EIA, we return to negative (and very negative) data this week: +7.265 million barrels, +1.089 million barrels in Cushing, +0.344 million barrels of gasoline, and -0.732 million barrels of distillates. Total implied product demand was 2% higher than in 2019, although gasoline demand surprisingly fell (-6% vs. 2019). In fact, the current weakness in prices has been accompanied by lower refining margins and physical timespreads, suggesting a notable weakening of the physical market.

On the positive side, the weight of liquids (actual oil) in shale production continues to decline, and it is doing so at an accelerated pace. The shift towards more gaseous production is a bad sign for volume growth expectations, which seems to validate the Goehring&Rozencwajg thesis on the stagnation of growth; if confirmed, the world would lose the only source of growth (ex-OPEC) in the last decade. This fact coincides with very bullish demand estimates from OPEC, which would imply a deficit of >2 million barrels starting in the second half of the year, which seems certainly exaggerated; in fact, if they are right, the only way to prevent crude oil prices from skyrocketing would be to voluntarily return sequestered volumes to the market, an event for which we are already positioned in the model portfolio.

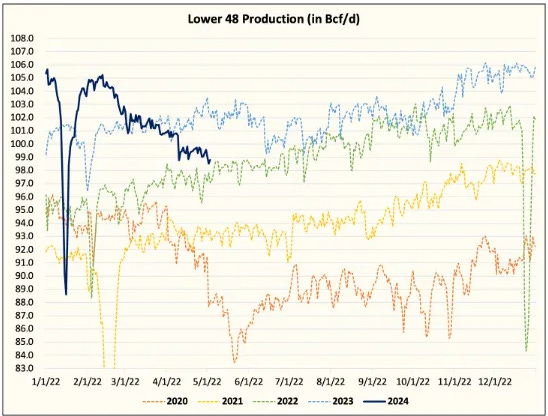

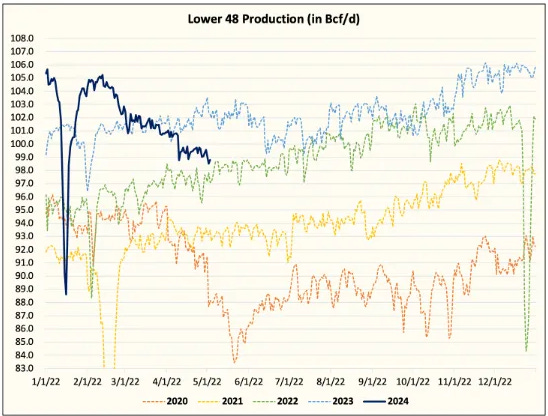

In the natural gas segment, the recent period of low prices is already affecting fundamentals, with two of the largest producers (Chesapeake and EQT) announcing that they will reduce production, which is already below 100 billion cubic feet per day (Bcf/d).

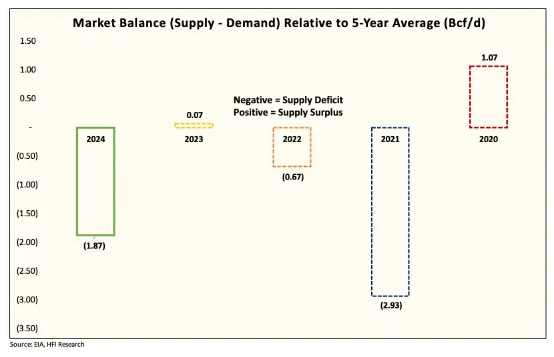

Although demand, both atmospheric and industrial, is not keeping pace, the reduction in supply and the expansion of LNG export capacity are projecting a deficit of 1.87 billion cubic feet per day (Bcf/d) for 2024, which, although positive, will not be enough to counteract the high level of starting inventories; however, all the pieces are falling into place to enjoy a great bullish market in the second half of this decade.

Model Portfolio

With the immense amount of liquidity and capital that has entered the markets in the last four years, one would expect that all asset classes would have benefited, to a greater or lesser extent, highlighting those with better performance. Of course, that has not been the case. As almost always, commodities have remained very lagging, and excluding the anomaly that was 2022, capital outflows from the space since mid-2020 have been consistent.

This fact has several positive readings for us, and it is that we have managed to achieve outstanding performance despite these headwinds, and if the market context changes, to an environment of high inflation and slower growth, it is likely that institutional investors, who have so far mass exodused from this sector, will return, pursuing (as always) the highest returns.

This too shall pass.

The model portfolio's return is +18.93% YTD compared to +7.52% for the S&P500, and +55.80% versus +28.90% for the S&P500 since inception (September 2022).

Keep reading with a 7-day free trial

Subscribe to LWS Financial Research to keep reading this post and get 7 days of free access to the full post archives.