Weekly summary 05/10

Weekly summary 05/10

Middle East tensions

Disclaimer

LWS Financial Research is NOT a financial advisory service, nor is its author qualified to offer such services.

All content on this website and publications, as well as all communications from the author, are for educational and entertainment purposes only and under no circumstances, express or implied, should be considered financial, legal, or any other type of advice. Each individual should carry out their own analysis and make their own investment decisions.

This week has been full of macro events that deserve analysis and monitoring, even though not all are immediately actionable: elections, geopolitical tension, strikes... With just one month to go before the U.S. elections, we will prepare a comprehensive report in collaboration with Aleix Amorós, which we will publish soon on the Substack platform.

Weekly macro summary

There have also been quite a few interesting events to analyze, and below I list the most noteworthy news. Let's get started:

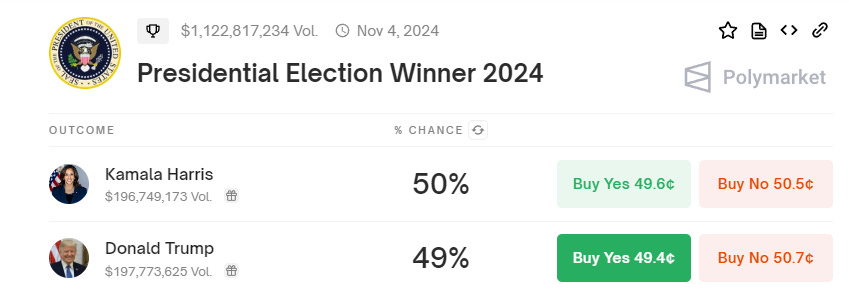

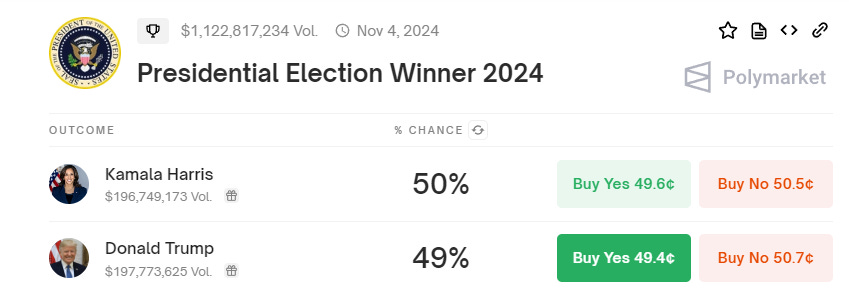

The debate between Democrat Tim Walz and Republican JD Vance, despite the previous tensions in the electoral campaign, was surprisingly civil. Although both have harshly attacked their opponents during the campaign, in the debate they focused on criticizing the presidential candidates of their respective parties, Kamala Harris and Donald Trump.

The most tense exchange occurred when Vance avoided answering whether he would challenge this year’s election results if Trump loses, leading Walz to criticize the false claims of electoral fraud that fueled the attack on the Capitol in January 2021.

During the debate, Walz criticized Trump’s handling of issues such as immigration and labeled him an unstable leader, while Vance attacked Harris for failing to address problems like inflation and the economy during her time in the Biden administration.

Despite the confrontation, the overall tone was calmer than what has characterized the campaign, which has been marked by incendiary rhetoric and two assassination attempts. Both candidates represent opposing visions of the heart of the American Midwest, but the debate was more focused on highlighting ideological differences on issues such as abortion, the crisis in the Middle East, and the economy.

The consensus was fairly clear about Vance's victory in the debate, and the odds of a Republican presidency slightly improved, although Trump remains somewhat behind in what appears to be a close race.

Shigeru Ishiba, who will be Japan's next prime minister, announced a general election for October 27 following his narrow victory in the internal contest of the Liberal Democratic Party (LDP). The election, which comes a year ahead of schedule, will determine which party will control the Lower House of Parliament.

Ishiba justified his decision by emphasizing the importance of having his administration evaluated by voters as soon as possible. In a press conference in Tokyo, following his victory in the party elections, he stressed that he needs legitimacy to lead the country in this new phase.

Markets reacted immediately to his victory. Japanese stocks fell more than 4%, while the yen strengthened, as Ishiba is seen as a "hawk" on monetary policy. His leadership could signal significant changes in the country’s economic policy.

The hawk Ishiba Japanese investors appear to be losing their historic preference for foreign assets. In the first eight months of 2024, they invested ¥28 trillion ($192 billion) in Japanese government bonds, the largest amount in at least 14 years, while purchases of foreign bonds were nearly halved to just ¥7.7 trillion, and less than ¥1 trillion was allocated to foreign stocks. With $4.4 trillion invested abroad, any significant withdrawal could impact global markets. Although Japanese interest rates remain low compared to other economies, the capital repatriation has been gradual.

The potential impact is enormous, as Japanese investors are the largest foreign holders of U.S. Treasury bonds and have significant stakes in markets such as Australia and Europe. A retreat by these investors could trigger turmoil similar to what occurred in August when concerns over Japanese rates and the U.S. economy led to massive liquidations of carry trade positions, affecting both the Nikkei and Wall Street.

Despite Japan's monetary policy normalization, foreign assets continue to attract investors seeking higher returns, such as the Government Pension Investment Fund (GPIF), which holds around 50% of its investments in foreign bonds and stocks.

The strike involving 45,000 port workers on the East Coast and Gulf Coast of the U.S., which halted the shipping of key goods ranging from food to automobiles, has ended after three days of disruptions. The strike, called by the International Longshoremen's Association (ILA) union, highlighted the workers' dissatisfaction with the lack of progress in negotiating a new six-year contract.

The conflict centered around wage demands and resistance to automation, which the union views as a threat to jobs. The workers were seeking a $5 per hour annual wage increase over six years and protection against automation projects at the ports, which they see as a direct threat to their jobs. According to union leader Harold Daggett, they were prepared to stay on strike as long as necessary to secure these protections.

The strike, the largest of its kind since 1977, affected 36 key ports in U.S. maritime trade, including New York, Baltimore, and Houston. It is estimated that this shutdown cost the U.S. economy approximately $5 billion per day. Although the immediate impact on consumer prices was limited, a prolonged conflict could have led to price increases for essential goods like food.

Ultimately, the parties agreed to extend the current contract until January 15, 2025, allowing them more time to negotiate. However, the issue of automation remains a central point of contention, as port operators see it as a way to improve profitability, while unions view it as a long-term threat to jobs.

The return of nuclear energy is gaining momentum. Following the announcement of the restart of Three Mile Island, in partnership with Microsoft, now comes the news that Holtec will reopen the Palisades nuclear plant in Michigan, backed by a $1.52 billion loan from the Biden administration. The goal is clear: to triple nuclear capacity in the U.S. as energy demand grows and climate concerns intensify. This could include the reactivation of other decommissioned reactors, like Three Mile Island itself, which suffered the worst nuclear accident in the country's history.

The process will not be easy or cheap. Although Holtec estimates that the restart of Palisades will take less time, authorities have already indicated that it could take up to two years before it is operational again.

The key point here is not just the expansion of nuclear capacity, but what it strategically represents for the administration: quality jobs and, above all, support for local economies.

Meanwhile, Pennsylvania is pushing for the quick restart of Three Mile Island. Governor Josh Shapiro has asked PJM Interconnection, the grid operator, to prioritize its reconnection. Microsoft has already signed an agreement to purchase its energy, further speeding up the timelines.

Nuclear energy is making a strong comeback, and it’s not just about energy supply. This is about securing jobs, stabilizing key regions, and following the narrative of energy transition. The administration knows this and is betting big.

Amid a growing environment of volatility in the oil and natural gas markets, geopolitical uncertainty has reached a new peak following Iran's recent attack on Israel on October 1st. This situation reflects a significant increase in regional tensions, and the market has already started to react. The price of crude oil has risen by 10% in just a few days, reflecting fears of a broader military escalation that could have deep consequences not only for the countries involved but also for global energy markets. This reaction highlights the risk that the conflict could spread beyond the borders of Israel and Iran, affecting major oil supply routes. Below, I’ve included Aleix's analysis shared on our Discord, in a condensed format.

This scenario isn’t entirely new. Last April, Israel carried out an airstrike on Iranian diplomatic facilities in Syria, resulting in the deaths of seven officers from the Iranian Revolutionary Guard Corps (IRGC). In response, Iran launched a coordinated offensive with drones and missiles, but Western powers helped Israel neutralize most of the projectiles, significantly limiting the impact. Despite the tensions, these events did not cause major disruptions in energy markets, as the market did not anticipate a larger-scale conflict.

However, the October 1st attack was much more severe and involved ballistic missiles, a more lethal and harder-to-intercept technology. Despite the intervention of Israeli defense systems and U.S. destroyers in the area, at least 30 missiles hit key infrastructure, including the Nevatim and Tel Nof airbases, as well as the outskirts of Tel Aviv.

The fact that tensions have not dissipated quickly this time suggests that the market perceives an imminent and potentially more aggressive response from Israel.

Possible scenarios: impacts and geopolitical risks

With the imminent possibility of Israeli retaliation, different scenarios could unfold in the coming days or weeks. Each of these has different implications for regional stability and oil prices.

Attack on Iranian military assets (40%)

The most likely option, in line with what happened in April, would be for Israel to strike Iranian military assets, such as airbases or even naval bases like Bandar Abbas. This type of attack would restore deterrence without necessarily escalating the conflict into a full-blown confrontation. However, since Iran has previously evacuated some of these strategic sites, including moving its naval fleet into the open sea, the military destruction would likely be limited.Impact on oil: While the market might initially react nervously, the impact would be temporary. Once the risk of a more severe escalation is neutralized, the geopolitical premium on oil prices would likely gradually diminish.

Attack on Iran's nuclear program (20%)

Another option Israel might consider is attacking Iran’s nuclear facilities, such as the Natanz enrichment complex or the Nuclear Technology Center in Isfahan. While this would make it harder for Iran to advance its nuclear program, key facilities are likely deeply protected underground, reducing the effectiveness of an airstrike.Impact on oil: This type of attack wouldn’t have a direct impact on oil supply but would increase market uncertainty due to the possibility of Iran accelerating its nuclear program. This would keep upward pressure on crude prices due to long-term risk perception.

Attack on Iran's energy infrastructure (30%)

A more drastic scenario would be Israel attacking Iran’s energy infrastructure, including pipelines, refineries, and export platforms in the Persian Gulf. An attack on the Abadan refinery, Iran's largest, with a processing capacity of 630,000 barrels per day, could significantly disrupt domestic oil supply. Even more serious would be an attack on export platforms on Kharg Island, which handles between 90% and 95% of Iran's crude destined for Chinese refineries. This option gained traction after Biden’s statements acknowledging that he was discussing the possibility with Israeli leaders, although he later clarified that his stance opposed this course of action.Impact on oil: Such an attack would have a massive impact on the global oil market, with risks of supply disruptions that could trigger a disproportionate spike in crude prices. If the Strait of Hormuz, one of the main oil transit routes, were temporarily closed, the global energy crisis could reach historic proportions.

Attack on Iran's political leadership (10%)

An attack on key figures in Iran's leadership, such as senior IRGC commanders or even Supreme Leader Ali Khamenei, would be a high-risk option. While not the most likely scenario, it could trigger a spiral of reprisals that would be difficult to contain, increasing geopolitical tensions across the region.Impact on oil: This would be one of the riskiest scenarios, as an Iranian retaliation would be almost inevitable. The impact on oil prices would be extremely high, with prolonged uncertainty and potential disruptions to global supply.

Currently, the global energy market is in a state of latent uncertainty. Israel’s response will largely determine whether oil prices continue to rise or if geopolitical tensions can be contained without significant disruption to supply flows. Although the focus is on crude oil, we should not overlook the behavior of natural gas in Europe. The TTF benchmark index closed today at around €40.98 per MWh, its highest level so far this year. The risk in the Middle East, especially related to Qatar's LNG supply, is a key factor, but most notably, Europe’s gas reserves have stopped growing.

This week, we saw an increase in U.S. oil inventories: +3.89Mb of crude, +0.84Mb in Cushing, +1.12Mb of gasoline, and -1.28Mb of distillates, largely influenced by the impact of Hurricane Helene on refineries, which demanded much less oil. Fundamental indicators (time spreads and refining margins) have rebounded along with the price, showing that the rise in crude is not solely (although mostly) due to the geopolitical premium.

The oil market is experiencing a paradoxical situation. Despite the overall narrative, it seems that nothing is priced into the current market levels. Speculative positioning is at historic lows, with fund managers shorting both diesel and Brent, reflecting a broadly bearish sentiment. Just a few months ago, in April, everyone was talking about the possibility of crude reaching $100 per barrel. Today, however, the perception has completely reversed, and many see $50 as an inevitable destination.

From the geopolitical side, which I always like to ignore (it rarely materializes), it’s relevant to understand how, since Biden's arrival at the White House, sanctions on Iran have been overlooked, allowing it to freely export oil at very high levels. If Trump wins, or if Israeli pressure intensifies, we could see these figures drop again as they did in 2019.

The EIA also released its monthly data for July, where I highlight the robustness of demand and the weakness of production (the perfect combination). The growth of U.S. shale oil production in 2023 has been overestimated, partly because the EIA underestimated 2022 production levels and then overestimated 2023 figures starting in June. This created an inflated growth rate that many analysts used in their projections for 2024 and 2025. In reality, oil production has remained flat over the past year, far from the consensus expectation of reaching around 13.5 million barrels per day by the end of 2023.

Additionally, associated gas production in the main shale oil basins has been outpacing crude oil production growth, which is a clear sign that these basins, particularly the Permian, are maturing and nearing their production peak. Despite the recent rebound in crude prices, they have only returned to last month's levels and still show an annual decline of more than 10%. Meanwhile, gasoline prices in the U.S. remain near eight-month lows.

Model Portfolio

The model portfolio's return is +19.74% YTD compared to +19.26% for the S&P500, and +57.44% versus +40.61% for the S&P500 since inception (September 2022). The model portfolio, as of Friday's close, is as follows:

Keep reading with a 7-day free trial

Subscribe to LWS Financial Research to keep reading this post and get 7 days of free access to the full post archives.