Weekly summary 06/07

Weekly summary 06/07

What can be, unburdened by what has been

Disclaimer

LWS Financial Research is NOT a financial advisory service, nor is its author qualified to offer such services.

All content on this website and publications, as well as all communications from the author, are for educational and entertainment purposes only and under no circumstances, express or implied, should be considered financial, legal, or any other type of advice. Each individual should carry out their own analysis and make their own investment decisions.

This week in the markets has been shorter than usual (holiday in the U.S. markets on July 4th, Canada Day on Monday), but very positive for our tracked ideas, practically eliminating the declines of the last month and bringing us back to new highs, just as we enter the seasonally most positive period.

The return of the model portfolio for the week (open positions and a repositioning movement) has been 5.91%. We have also published a new investment idea, Gulf Keystone Petroleum, with a very asymmetric return profile and top-notch geopolitical context and introduction, prepared by Aleix Amorós. I encourage you all to read it!

Weekly macro summary

There have also been quite a few interesting events to analyze, and below I list the most noteworthy news. Let's get started:

Everything seems to indicate that Biden will be replaced as the Democratic candidate, and with so little time left until the elections, the only viable option is Kamala Harris, who compares very poorly against the Republican candidate in the polls-

With Trump as the most likely presidential option, Asia is already preparing for the possible reimposition of significant tariffs on its exports. It seems likely that Europe will follow suit (as they have already advanced, for example, in the field of electric cars), and in this region, the effects would be much more detrimental, further reducing their economic growth.

The labor component, until now the FED's support for interpreting that the economy was still resilient, is beginning to crack at an accelerated pace. Job creation figures in the most cyclical sectors, such as hospitality or retail, have reversed all the gains of 2021-2022 and present a worrying picture. My opinion is that we will see a very significant deterioration in the June data, and that the first cuts, almost in a context of panic, will come either in July or September.

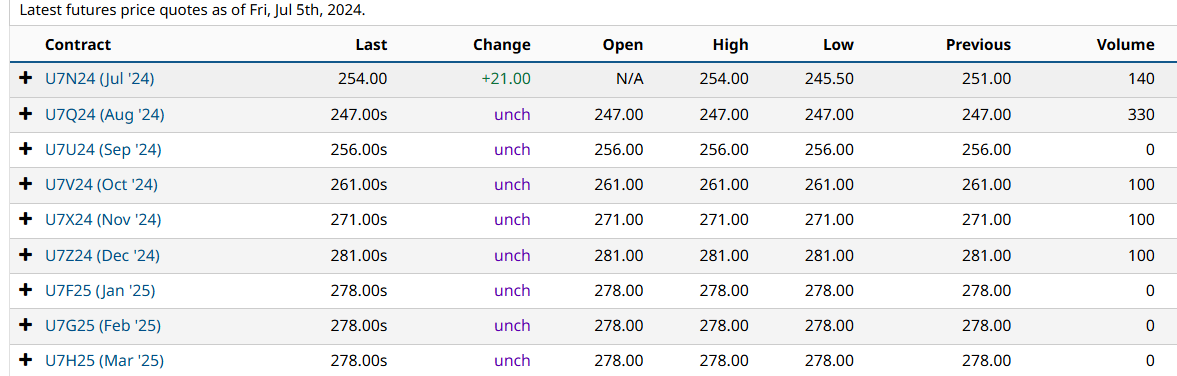

Over the weekend, one of Anglo American's coal mines (Grosvenor), which produced ~3Mt of high-quality metallurgical coal, caught fire, and it appears it will be out of service for a long time (possibly forever). These types of accidents are very difficult to remedy due to coal being the combustible material and the difficulty of accessing the facilities (typically, nitrogen is injected to displace the oxygen). As always, problems never come alone, and another similar incident has also been reported at the Century mine. This comes in a tight market, just as we enter the restocking period. Prices have moved up 20% this week, and this has been reflected in the sector's stock prices as well. While it is unlikely that we will go much higher than $300/t this year, this event has raised the theoretical floor of the futures curve.

India, the largest source of demand growth (both for coal and many other commodities), continues to show great economic strength (in stark contrast to the weak Western economies and even China itself), with its monthly PMI above 60.9, reflecting strong economic expansion, and the manufacturing component showing the fifth consecutive month of growth.

Despite the collapse of the real estate and construction sector in China, its imports of metallurgical coal, a proxy for steel, continue to grow. However, the composition and mix of suppliers have changed significantly in recent years: in 2020, China imposed a ban on Australian coal imports due to Australia’s request to investigate the origins of COVID, which was not relaxed until 2022. Meanwhile, the Asian giant has increased its dependence on Mongolia (lower quality) and Russia. In any case, in a global market, only the total volume matters, and any change in traditional trade routes tends to be very positive for prices.

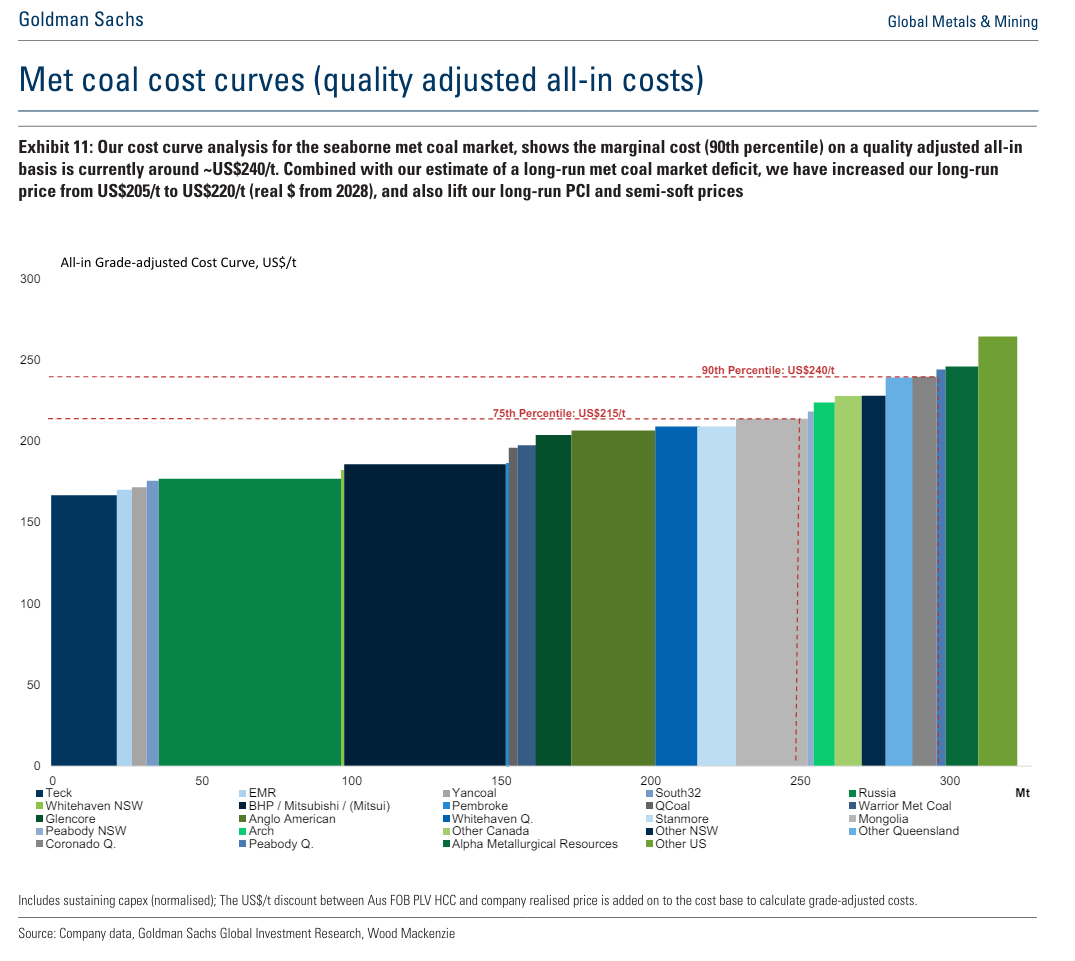

The following chart quite illustratively reflects the investment thesis in metallurgical coal companies and why, barring some specific macroeconomic hiccup, prices can no longer sustainably fall below $215/t. When 25% of the cost curve is above this price, barring a technological disruption that completely alters demand prospects, it is not sustainable to think of price scenarios below that threshold.

Even in thermal coal, with a much more uncertain terminal value than in the case of metallurgical coal, Western utilities, which are under the most political pressure, no longer see a clear path for an immediate phase-out.

When we were looking at emissions reduction, it was based on running our coal-fired power plants less at the end of the decade […] we don’t see a pathway for that now.

— Brian Tierney, CEO of FirstEnergy

Sentiment in the crypto ecosystem is at its lowest point of the year, and it seems that only negative catalysts are on the horizon. It’s always darkest before the dawn. Ten years after its bankruptcy, the exchange MtGox will soon begin distributing 120k BTC, equivalent to $9 billion, which many analysts expect will add more downward pressure on the asset’s price. My opinion, however, is the opposite:

Most of the distribution has been bought by institutions, which have offered to purchase the retail investors' share as well, but they have declined the offer, showing some resistance to an immediate sale.

The users affected 10 years ago are early adopters, demonstrating a higher-than-average predisposition and knowledge, making a complete exit much less likely. In fact, it is most probable that this new money, while it may leave BTC, will stay within the crypto ecosystem.

The German government continues to sell its BTC inventory, with a recent sale of 1,300 units. How can we tell that this government is not financially qualified? They do not understand the concept of asymmetry nor have training in game theory; similar to fund managers, short-term incentives and vision prevent them from making the right decisions:

The country’s ANNUAL fiscal deficit is €87.4 billion, and they currently have 43,459 BTC which, if sold, would bring in €2.5 billion. This means that if Bitcoin ultimately fails, the current benefit to the country would be 2.8% of the annual budget deficit.

If Bitcoin ultimately succeeds and becomes the cornerstone of a new monetary system, Germany would already be out of the game. For a handful of dollars.

At the same time, Donald Trump proposes, for the first time in the country’s history, studying the possibility of establishing a Bitcoin reserve as a strategic asset. The contrast with his OECD peers is stark. Being the first mover would give them an enormous, perhaps insurmountable, advantage, which might be the only option to lead the next geopolitical and monetary cycle.

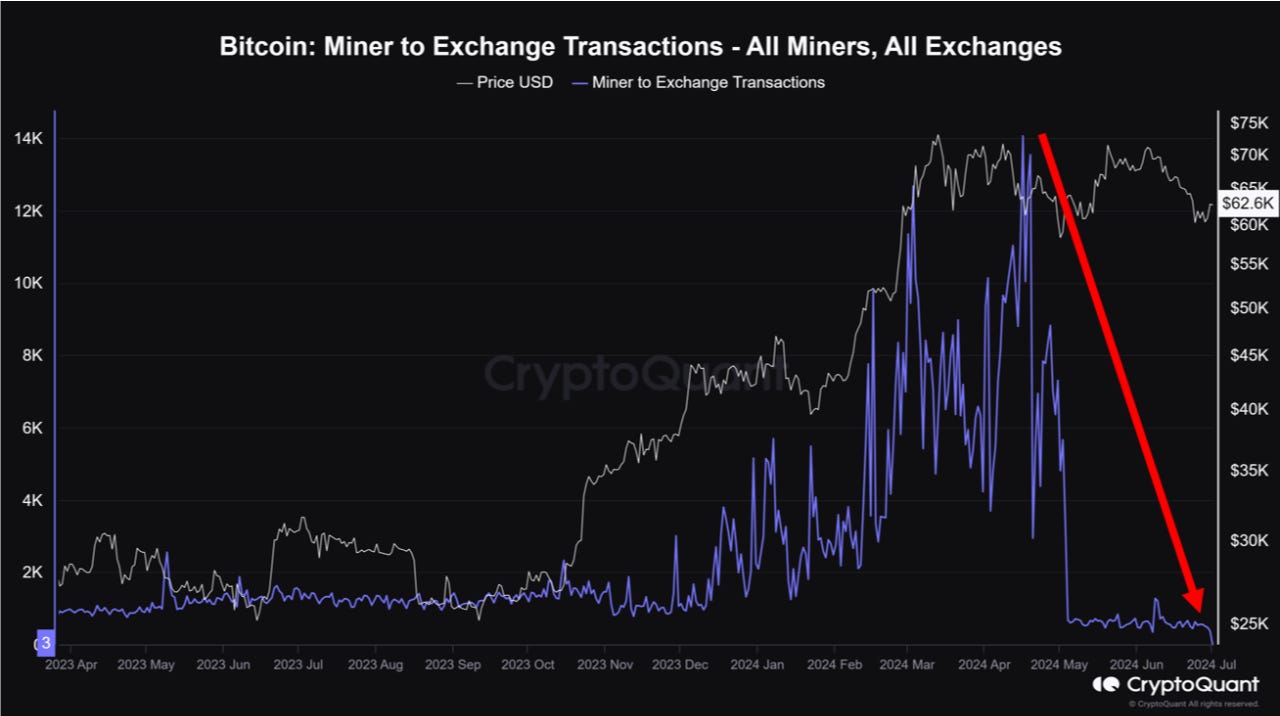

Bitcoin miners, especially the less efficient ones, are struggling greatly to keep their operations profitable, as rewards have been halved (after the halving) and the price has significantly corrected from its highs. Paradoxically, to stay afloat, they have had to liquidate much of the BTC they had in their inventories, causing more downward pressure on the price, thus aggravating their problems. Recently, in the OTC markets where they conduct their operations, buyers have absorbed all the pending volume, showing a greater appetite at these prices.

Bitcoin is what can be, unburdened by what has been.

Reality cannot be avoided forever, and eventually, it must be confronted. After several EIA inventory reports where the figures didn’t add up, everything collapsed in this week’s report: -12.16Mb of crude, +0.345Mb in Cushing, -2.21Mb of gasoline, and -1.535Mb of distillates. With the trend in prices and if inventories continue to fall, as would be normal, the USA will be forced to release inventories from its SPR again, which would allow OPEC+ to extend their cuts for another quarter. Demand is at its highest in recent years, and none of the economic problems on the horizon are yet taking a toll.

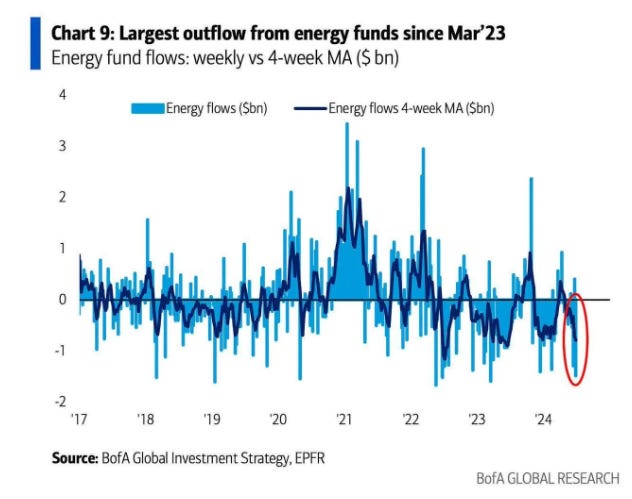

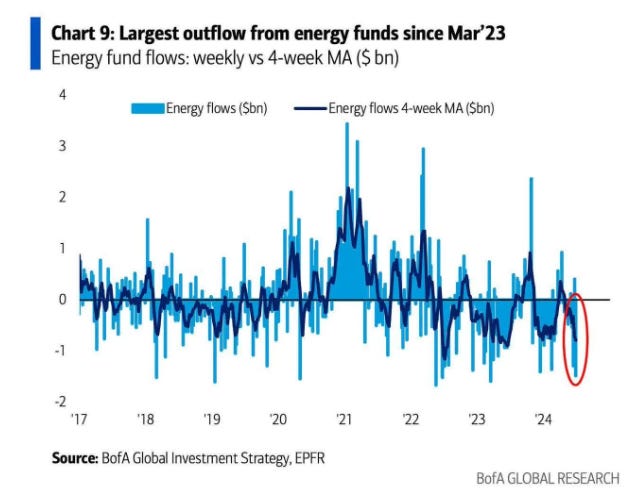

In contrast to these positive developments in the physical market and fundamentals, stocks have not taken off (in fact, they have even performed negatively), explained by the large capital outflow from energy-themed funds, the largest since 2023. Currently, sentiment is very bad, and it seems that only technology and AI are investable, but eventually, this will reverse, and what is now an obstacle will become a tailwind. This too shall pass.

Strong rumors have emerged about the intention of China’s state-owned oil companies to acquire ~60Mb for their SPR. If oil prices remain at these levels (>85$/b Brent), it is highly likely that the USA will release barrels from its SPR this summer, aiming to prevent a significant price increase for the end consumer before the elections. Wouldn't it be ironic if the barrels released by the United States were taken advantage of by China to fill their own reserves at a lower price?

The United Kingdom has established quotas requiring zero-emission vehicles to represent 22% of manufacturers' sales this year, increasing to 80% by 2030. Dealers who do not comply face fines of £15,000 for each non-compliant vehicle sold. So far, electric vehicles have accounted for only 16% of car sales in the UK in the first five months of the year. Most of these vehicles have been purchased by corporate fleets, and retail demand is likely lower than the official figures suggest due to "pre-registration." Last week, the owner of Peugeot and Citroen threatened to halt vehicle production in the UK in protest of these targets, and their CEO, Carlos Tavares, called the policy "something terrible for the UK."

Among the new categories of low-emission vehicles, we have been highlighting for weeks that the one showing the most growth is plug-in hybrids, which offer many of the advantages of BEVs but with much greater convenience. It is important to recognize this reality to adapt in two of our major ideas, such as oil and PGMs.

Climate fanaticism, which is insatiable and contrary to the ideal of human progress, is not limited to the transportation sector. It has taken another step in Denmark, where a new carbon tax on agriculture will be implemented starting in 2030, requiring farmers to pay $17.3/t for each ton of CO2 emitted. Let’s see who proposes the biggest nonsense.

Model Portfolio

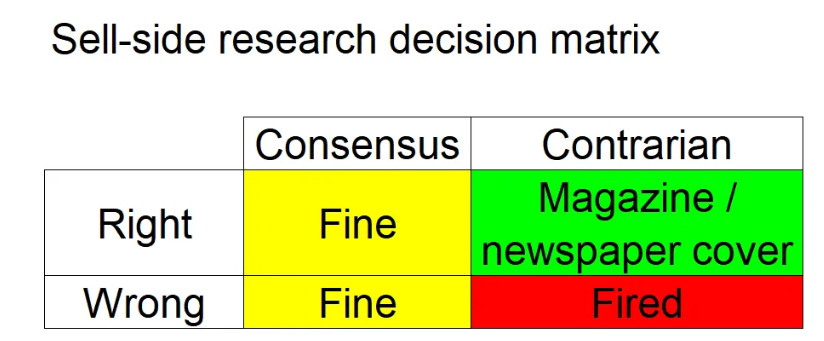

From this publication, we have always advocated that a contrarian mindset is necessary to achieve extraordinary results. However, it is not about fighting against all consensus narratives simply for the sake of being contrarian, but rather about having the right mentality. In this regard, it is important to understand what consensus is, how it forms, and what incentives analysts have for their recommendations.

No sell-side analyst, and practically no investment firm, lives off their returns or performance, with reputational risk being the priority. The following matrix clearly defines their incentive system.

If we understand how the game works (hence their recommendations and price targets always adapt the narrative to the price), we can truly generate alpha and separate our returns from the crowd. We must cultivate independent thinking, based on data, and be flexible and agile to adapt to the ever-changing reality.

The model portfolio's return is +16.52% YTD compared to +13.81% for the S&P500, and +53.39% versus +35.19% for the S&P500 since inception (September 2022). The model portfolio, as of Friday's close, is as follows:

Keep reading with a 7-day free trial

Subscribe to LWS Financial Research to keep reading this post and get 7 days of free access to the full post archives.