Weekly summary 07/09

Weekly summary 07/09

Peak bearishness

Disclaimer

LWS Financial Research is NOT a financial advisory service, nor is its author qualified to offer such services.

All content on this website and publications, as well as all communications from the author, are for educational and entertainment purposes only and under no circumstances, express or implied, should be considered financial, legal, or any other type of advice. Each individual should carry out their own analysis and make their own investment decisions.

Weekly macro summary

There have also been quite a few interesting events to analyze, and below I list the most noteworthy news. Let's get started:

In case it wasn't already clear, the next interest rate move in the United States has been sealed this week. Following very weak manufacturing PMI data, with quite negative sentiment and making the current economic slowdown evident, Friday's employment data confirmed that the FED, as always, is behind the curve.

The latest employment data in the United States shows a mixed picture that points to a significant weakening of the labor market, especially in the private sector. Non-farm payrolls grew less than expected, with an increase of 142,000 jobs compared to the 164,000 forecast, and a downward revision of the previous month's figure, which went from 114,000 to 89,000.

The private sector also reflected a slowdown with 118,000 jobs created, below the 139,000 forecast. Last month's downward revision, from 97,000 to 78,000, further highlights this trend.

On the other hand, average hourly earnings increased by 3.8% year-on-year, slightly exceeding the 3.7% expectations, which could put pressure on inflation. The unemployment rate dropped to 4.2%, a figure already anticipated by many analysts, preventing the data from being entirely negative.

As of yesterday's close, the markets are giving a 50% chance of a 50bp cut in 12 days

In a surprising move, Swiss luxury watch brands are seeking financial assistance from the government to cope with the drop in demand. Girard-Perregaux and Ulysse Nardin, part of the Sowind Group, have been the first to confirm the use of a state program that allows reducing working hours without permanent layoffs.

It’s a small watch crisis, slightly disconnected from the economy.

This state program covers up to 80% of workers' salaries, a measure that was also used in 2020 during the pandemic, allowing the industry to quickly ramp up production when demand recovered.

The collapse in demand, especially in China, has affected mid-range watch brands more, while luxury brands like Rolex and Patek Philippe have shown greater resilience.

Joe Biden has decided to block the acquisition of US Steel by Nippon Steel, which valued the steelmaker at $14.9B, after concluding that the deal poses a risk to national security. The decision comes at a key moment for Kamala Harris's campaign in Pennsylvania, one of the states that could decide the upcoming U.S. elections. In this matter, there is bipartisan support, as Trump has also announced that, if elected, he would immediately block the deal.

The Committee on Foreign Investment in the United States (Cfius) had already warned Nippon Steel that the transaction raised security concerns, significantly lowering the chances of the deal going through. US Steel shares dropped 18% after the news, reflecting the potential impact of the administration's intervention.

What is surprising in this case is that Japan is a key strategic ally of the United States in the Asia-Pacific region, and many question whether this acquisition truly poses a risk. However, political calculations seem to prevail, and both parties have used the issue to appeal to steel industry voters in a critical state. Without the deal, it is likely that United States Steel will have to close part of its operations to balance the market: job losses do not seem like good news heading into an election cycle.

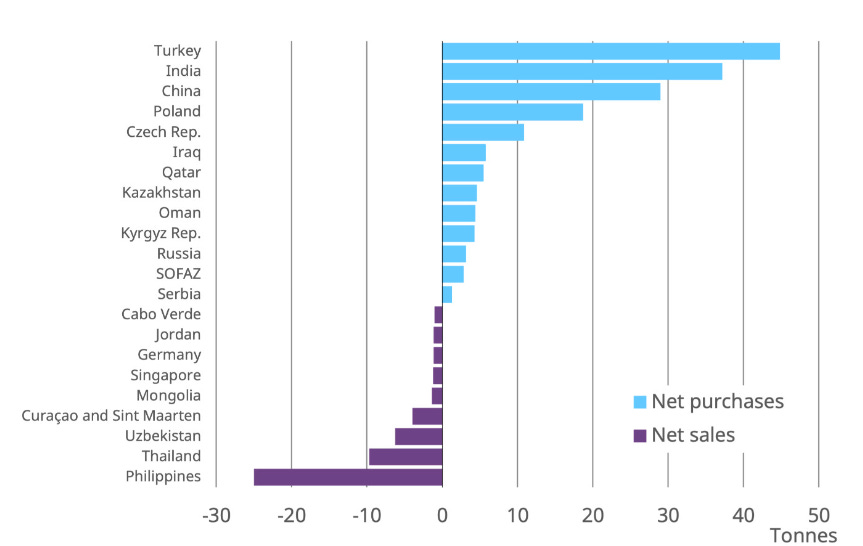

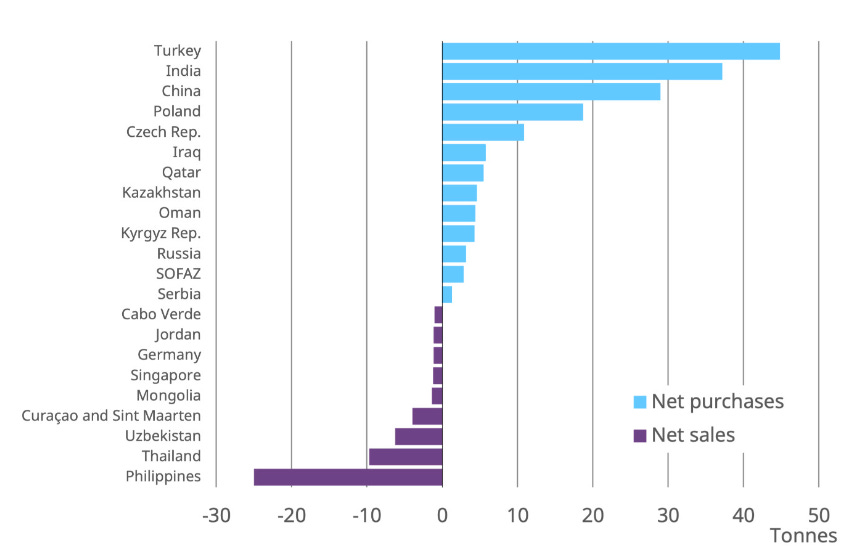

The Russian Ministry of Finance has announced an exponential increase in its gold purchases, which will rise from 1.12B rubles daily to 8.2B per day over the next month. Russia, which has been a net buyer of gold throughout 2024, has added about 4 tons of the metal to its reserves. This move is part of a broader strategy, which began in 2013, to decouple its economy from the U.S. dollar, and in 2022, it established a new gold standard for the ruble.

As the second-largest gold producer in the world, with 321 metric tons in 2023, Russia is taking advantage of high gold prices, which are hovering around $2,500 per ounce. This strategy aims to strengthen the Russian economy amid the war in Ukraine and international sanctions.

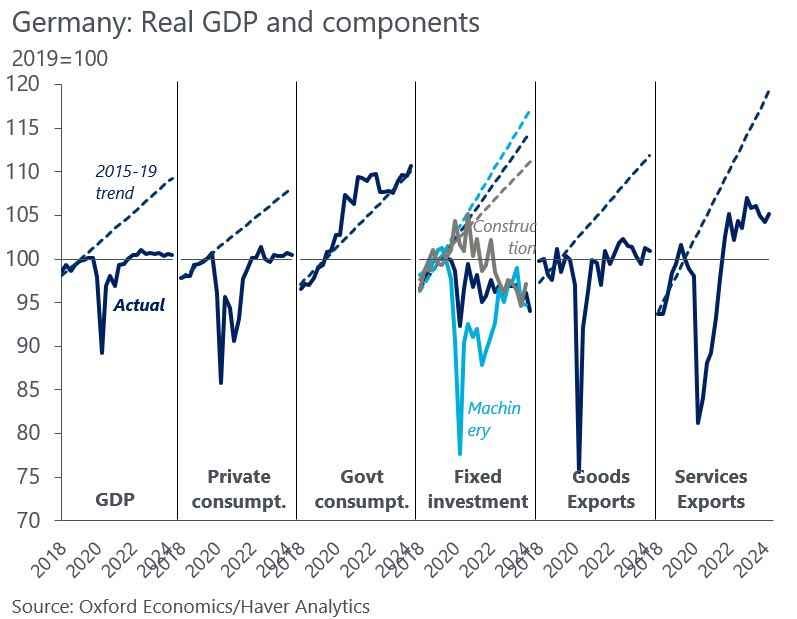

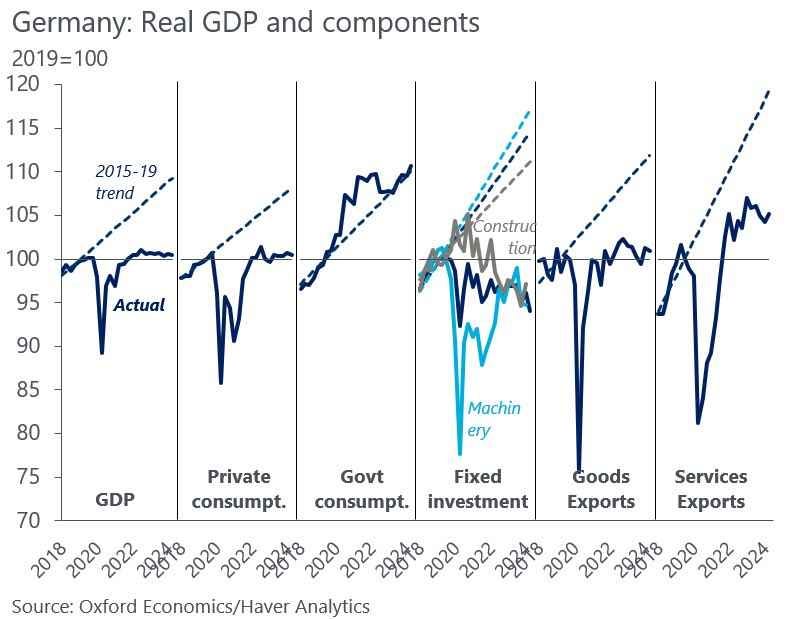

Germany, once an industrial powerhouse and the great engine of Europe, has been in economic stagnation for 6 years, where the only thing that has grown is public spending.

And what could be the reason? All signs point to the Energiewende. The cost of energy, the driving force of industry, has skyrocketed over the past 5 years, and has been on an upward trajectory for decades, as denser energy sources have been replaced by lower quality ones (intermittency, price, etc.). In the following chart, we can see the gross energy production by year and source in Germany between 1990 and 2023.

After the permanent exit of BASF last year, Germany's flagship company, Volkswagen, is now also considering closing factories and laying off workers in the country, highlighting the total loss of competitiveness in recent years. Probably nothing.

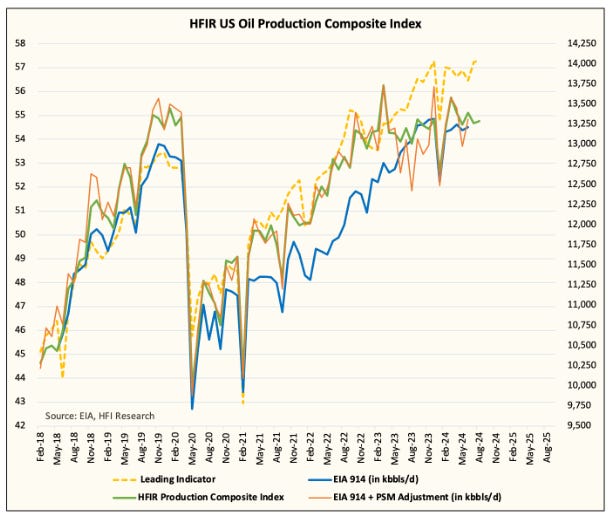

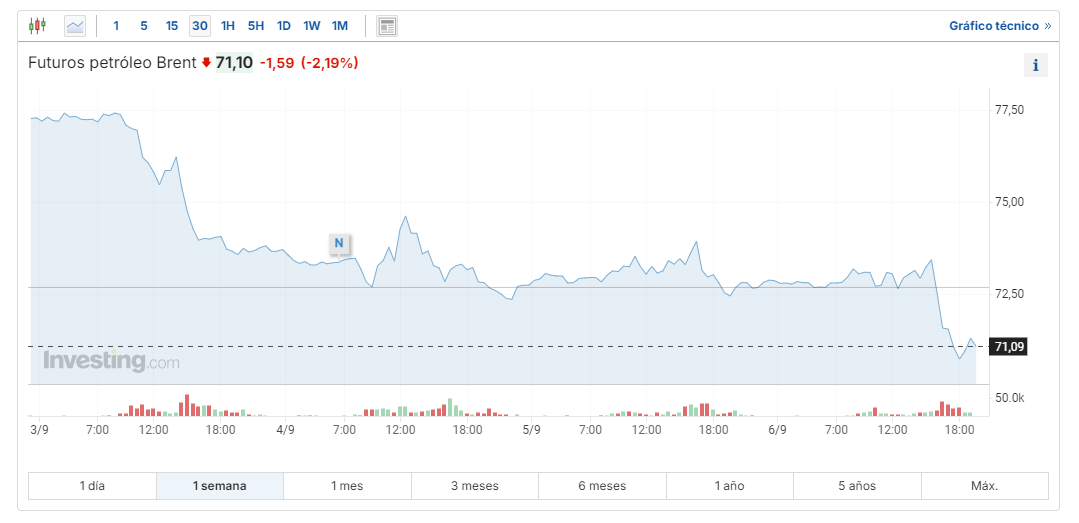

Another week, another massive drop in U.S. oil inventories: -6.9Mb of crude, -1.1Mb at Cushing, +0.8Mb of gasoline. If we only knew three facts: U.S. commercial inventories are at five-year lows, production has barely grown since Q4 2022, and global demand, even with China’s weakness, shows year-over-year growth, and we couldn't look at the crude price, we might be surprised to know that it is at lows and that the sentiment surrounding this commodity points more toward a collapse than a recovery in the short and medium term.

In addition to recession fears and the improvement in the geopolitical situation in Libya, last week the OPEC floated a trial balloon proposing to return some of the withheld volumes to the market starting in October; after seeing the market’s reaction, they decided to extend their cuts for two more months, until December, when they will reassess the situation.

Even if they reversed their cuts as announced, either now in October or in December, the net increase to the market would be minimal: since Iraq, Kazakhstan, and Russia have been overproducing during these months, they have agreed to compensate for this over the next year, so if they keep their promise (which is already a big assumption...), the net effect would be zero.

The narrative surrounding oil prices and their cycles is always extreme, especially when we transition from one price regime to another. Today, we are in an environment where even the most efficient producers in the best shale basin, the Permian, are struggling to generate returns. Can prices fall further? Of course, but in the long term, it’s unsustainable and only sets the stage for the next bullish phase.

The issue of refining margins is particularly paradigmatic: their weakness is used as a clear indicator of demand weakness when, in this case, it is more influenced by the large refining capacity (Nigeria, the Middle East, China...) added in recent years, which creates a new reality of prices and margins that they can exploit with their better technology.

In the current environment, even the most efficient producers in the shale basins are unable to generate positive returns, and since Q4 is the quarter where next year's CAPEX campaigns are shaped, it is likely we will see a downward adjustment in these, which will ultimately positively impact next year’s balance.

There is a narrative, gaining traction every time oil experiences a temporary weakness, that emphasizes how, driven by widespread adoption of electric vehicles, oil demand is going to collapse; in fact, even though my opinion is contrary, the bullish case doesn’t even consider the resilience of internal combustion vehicles: it assumes that almost all growth (75%+) will come from the petrochemical sector. How is that going to be replaced?

Model Portfolio

Recession drums are now beating loudly, heavily influencing market positioning, although there are already some signs of improvement, both in Europe (PMIs on the rise) and in Asia itself. Today I want to share a reflection on the current pessimism surrounding commodities and offer a key nuance. In cyclical companies, as we have analyzed on various occasions, there are actually two underlying cycles: the capital cycle and the economic cycle.

The capital cycle is, without a doubt, the most dangerous for our investments. When prices are high, this tends to incentivize an increase in supply, which eventually reduces prices and leads to a bearish period in the industry. Here, the problem lies in the supply, and this is where a lot of capital is destroyed. This is the great risk we must avoid in this type of investment.

On the other hand, the economic cycle, while also impactful, affects in a different way, mainly influencing demand. This is the problem we are currently facing. However, unlike the capital cycle, economic cycles tend to be shorter, except in cases like the 2008 housing crisis. In today’s highly stimulated economic environment, these crises are usually resolved relatively quickly. Although these cycles can be painful —just look at the last month for us— they are not a long-term structural problem in most sectors.

In summary, we are facing an economic cycle that is affecting demand across the board, but not a fundamental imbalance in the commodities sector. The challenge remains avoiding the capital cycle, which is the true destroyer of long-term value.

You can’t fight the tide. In the short term, fundamentals don’t matter, and sentiment is so negative that it kills any momentum. The following chart shows the YTD performance of the major coal companies, both thermal and metallurgical, and despite having healthy balance sheets, very positive results, and good shareholder return programs, we can see how their performance has been truly poor... Does it make sense to value assets with 20+ year lifespans in many cases due to a temporary weakness of 1 or 2 quarters? In my opinion, no, and I believe the returns if we navigate this period of weakness will be extraordinary.

Right now, it’s estimated that there is $6.3T in money market funds, with 2.5T of that in the hands of retail investors; when inflation is around ~3%, and these vehicles yield 5% risk-free, the option is attractive, but what will happen when in 12 days Jerome Powell cuts rates and, by the end of the year, they are, according to consensus, 100bps below the current value? A wave of liquidity is coming, and this is another reason why I think this market weakness is not here to stay.

The model portfolio's return is +7.97% YTD compared to +13.19% for the S&P500, and +45.67% versus +34.54% for the S&P500 since inception (September 2022). The model portfolio, as of Friday's close, is as follows:

Keep reading with a 7-day free trial

Subscribe to LWS Financial Research to keep reading this post and get 7 days of free access to the full post archives.