Weekly summary 13/04

Weekly summary 13/04

Between Scylla and Charybdis

Disclaimer

LWS Financial Research is NOT a financial advisory service, nor is its author qualified to offer such services.

All content on this website and publications, as well as all communications from the author, are for educational and entertainment purposes only and under no circumstances, express or implied, should be considered financial, legal, or any other type of advice. Each individual should carry out their own analysis and make their own investment decisions.

We are approaching the Q2 earnings season, which will be particularly interesting for us due to the high prices of the raw materials produced and traded by many of our companies, and we will closely monitor it in this publication. However, before that, we will bring the updated investment article on Whitehaven Coal (as well as its model), and a new analysis next week.

Weekly macro summary

There have also been quite a few interesting events to analyze, and below I list the most noteworthy news. Let's get started:

On Wednesday, consumer price inflation (CPI) data was released in the United States, which once again slightly surprised on the upside (actually, the figure was 0.359% MoM, rounded to 0.4%, vs the expectation of 0.3%, so if it had been 0.009% lower, there wouldn't have been such a discrepancy), causing a sharp market decline as the window for Fed rate cuts continues to narrow.

The stock market's reaction seems certainly exaggerated, although the market now assumes we won't have more than three rate cuts in 2024 (initially, the consensus was for 6), and even several investment banks (and some Fed governors) are already pointing to only one 0.25% cut for the year, in November, after the presidential elections, or even new hikes if inflation accelerates. Luckily, Biden stepped in to calm things down:

I don't know what the Fed will do, but there will be a rate cut before the end of the year.

— Joe Biden

It's highly unlikely, in my opinion, that the Fed will fail its third mandate, the political one, especially in an election year, so my base case hasn't changed despite this setback in the fight against inflation.

My opinion is that we won't see a new big wave of inflation, at least in the short term, since service inflation is not rebounding alongside commodities, and wage growth is also very contained, unlike in 2021.

The German industrial collapse, which we have referenced so many times, seems to have arrived to stay. Due to the higher structural costs associated with importing gas via LNG compared to the cheap Russian supply, the European industrial sector is at a structural disadvantage, which at the moment seems insurmountable. Although valuations may appear attractive through screening, the fact of not being competitive in a globalized market environment is too great a burden, which skews the risk/reward profile downwards for this segment.

The sharp decline in inventories and the serious supply issues (export halts in Indonesia and Myanmar, which ranked in the top 3 producers in 2022), have caused a significant bullish movement in tin, reaching its highest level in the last two years, almost touching $33,100/t. The truth is, all factors pointed to this, and from the model portfolio, we were buying $AFM, one of the world's largest producers, 30% lower (average price 50% lower than current) a few months ago.

Tin has risen 27% YTD, surpassing copper to become the best-performing metal in 2024, which is certainly surprising, considering they are two commodities highly correlated with the economic cycle, where the consensus seems to be of manifest weakness.

In the same vein, major investment banks have revised upward the expected growth for China, hovering around 5% in all cases; beyond the specific figure, which we may believe or not, the trend is very revealing, as corroborated by other data on demand for industrial metals closely linked to the economic cycle, such as copper.

As we anticipated in the previous publication, the escalation of geopolitical tension in the Middle East is evident, and following the attacks by Israel on the Iranian embassy in Damascus, Tehran appears ready to retaliate. On Friday, alarm bells rang throughout the Jewish state as missiles were launched from Lebanon, orchestrated by Iran, targeting various points of its territory, increasing fear in the market and causing a spike in key volatility indicators.

Iran attempted to reassure the United States and other Western actors by specifying that the response would be measured and proportional, aiming to avoid a full escalation of the conflict. However, it warned the United States not to get involved in the conflict, under the risk of having its bases and military infrastructure in the area considered valid targets.

We've had another negative oil inventory report, and it seems that this will be the trend until the summer season, which is typically the most positive: +5.84Mb of crude, -0.17Mb at Cushing, +0.715Mb of gasoline, and +1.66Mb of diesel. Crude inventories have increased by 26Mb YTD while those of the main refined products have fallen by 46Mb.

On the bullish side, OPEC+ seems to have fully regained control of the market, and in its latest communication, it points to a forecast of strong demand in the summer, for which they will have to return part of the volumes withheld from the market if they want to avoid a price shock. In this regard, Joe Biden is not very helpful and continues to hinder local supply with new royalties and taxes for the development of oil and gas fields on federal land.

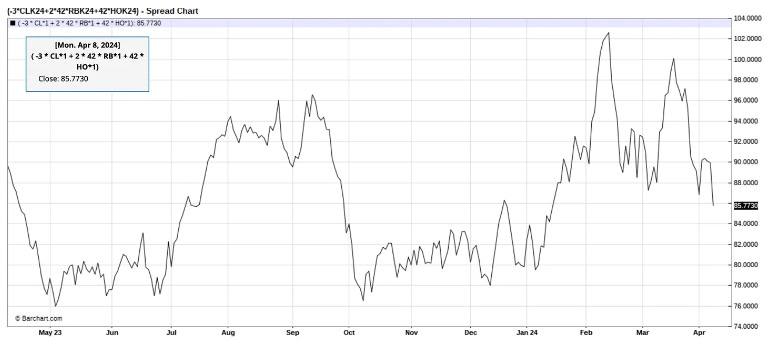

As we mentioned in the opening block, it seems that the trend for the coming months, until the arrival of summer, will be bearish inventory reports, and market fundamentals reflect this, with refining margins trending downward and having corrected from the highs of February and March, which always precedes, in normal market conditions (that is, excluding any geopolitical event), a consolidation or correction in crude oil prices. In case any additional signal is needed that we are near a (local) peak, Barclays has reopened its oil & gas coverage division; we already know that investment banks, due to their limited ability and their sole interest in extracting commissions from lagging investors, always arrive late to any trend. Position accordingly.

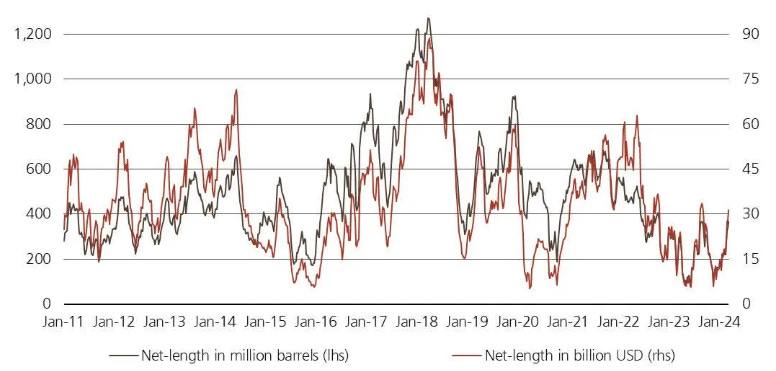

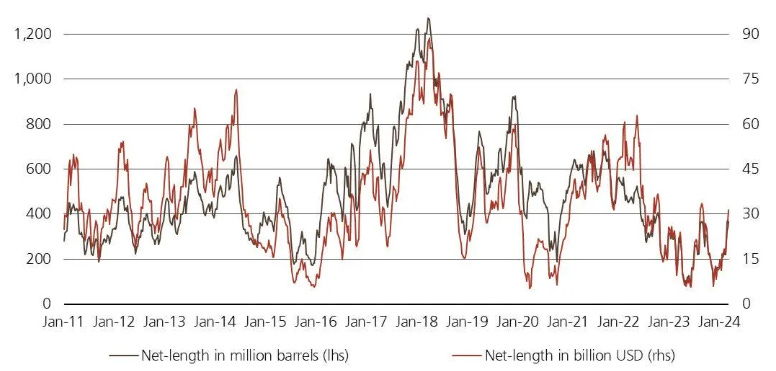

While it is true that geopolitical tensions and risks are providing a tailwind for prices, with fundamentals pointing in the opposite direction, the physical market should prevail, at least in the short term, especially considering the fickleness of political conflicts and how quickly they can change; additionally, speculative positioning has rebounded strongly from the lows earlier this year and, while not yet at bullish levels, it already offers much less optionality.

Model Portfolio

We are on the threshold of a new earnings season which, as always, we will closely monitor for all the companies in the model portfolio and the extended universe of LWS Financial Research in this publication. This week we have already had many operational and guidance updates, which we will now discuss, and which, generally speaking, have been very positive. Due to our investment philosophy, returns tend to arrive in short periods of time and very forcefully, as soon as a catalyst reveals the value we already know, and now we are in a true bullish frenzy, which makes me very positive about achieving our investment objectives:

Positive and double-digit returns: check (another year).

Outperforming any benchmark index: loading.

Navigating such a complex macro and market environment as the current one is not straightforward. It's crucial to remain detached from both euphoria and despair, to be reflective, and to avoid hasty decisions. It seems like we are caught between Scylla and Charybdis, a situation of chaos and volatility, which often also signifies opportunity. The model portfolio's return is +15.94% YTD compared to +7.29% for the S&P500, and +42.16% versus +28.67% for the S&P500 since inception (September 2022).

Keep reading with a 7-day free trial

Subscribe to LWS Financial Research to keep reading this post and get 7 days of free access to the full post archives.