Weekly summary 14/09

Weekly summary 14/09

The first debate

Disclaimer

LWS Financial Research is NOT a financial advisory service, nor is its author qualified to offer such services.

All content on this website and publications, as well as all communications from the author, are for educational and entertainment purposes only and under no circumstances, express or implied, should be considered financial, legal, or any other type of advice. Each individual should carry out their own analysis and make their own investment decisions.

Weekly macro summary

There have also been quite a few interesting events to analyze, and below I list the most noteworthy news. Let's get started:

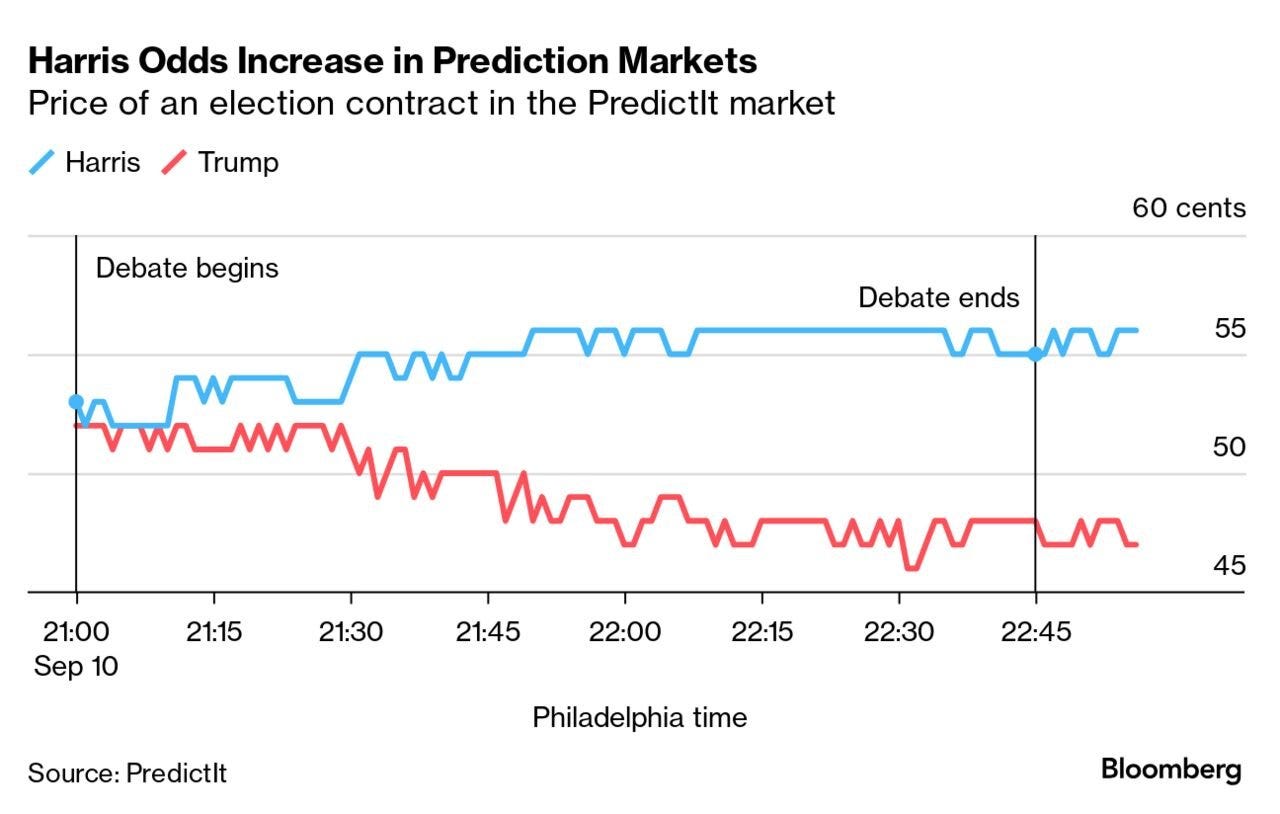

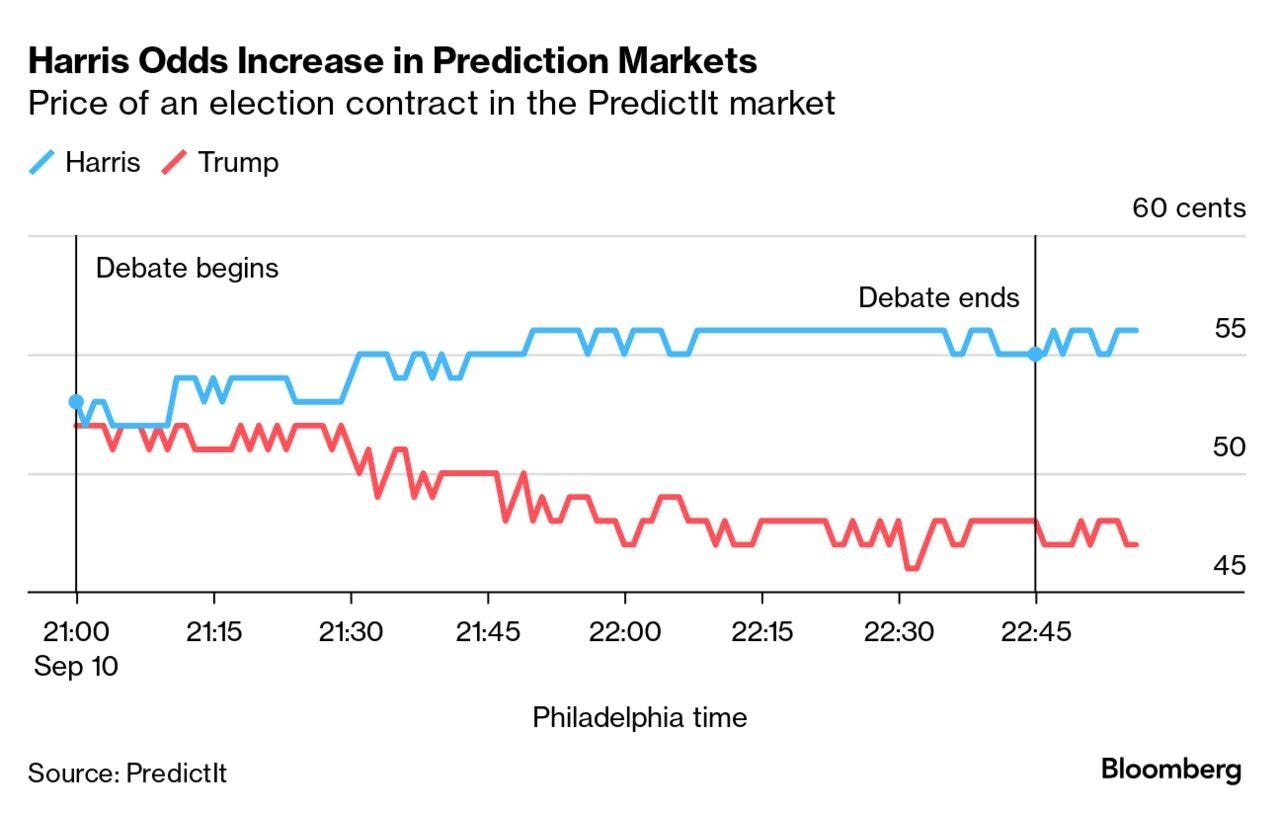

We had the first electoral debate between Kamala Harris and Donald Trump, which we followed with great interest, and Aleix Amorós analyzed on our channel (below is his analysis). The big winner was the Democratic candidate.

Harris was able to establish her own profile, distancing herself from Biden's baggage, and steered the debate in her favor. She leaned on the current administration's legacy only on favorable points, such as job creation, while avoiding thornier issues like the border.

Trump, on the other hand, often appeared cornered and on the defensive, leading to out-of-place and erratic comments in a markedly aggressive and belligerent stance.

Trump came into the debate with a 7-point lead over Harris on Polymarket, his largest lead since early August, and was favored in all the polls. Had he dominated the debate, he likely would have sealed the race for the White House. However, with last night's setback, the gap has narrowed to the smallest margin, and Harris is now regaining momentum after exhausting the initial boost from her nomination. Both campaign teams have already stated that both candidates are open to a second debate before the November 5 election. It remains to be seen on which network this will take place.

As for the debate itself, Trump barely led in the initial economic block, which is his strong point. Still, in my view, he focused too much on inflation, which is clearly in retreat in areas as sensitive to U.S. citizens as gasoline. Moreover, inflation is not directly under the control of the Executive but rather the Federal Reserve. He didn’t offer any solutions beyond his confrontational rhetoric toward the world, emphasizing his tariff stance.

Two of the most contentious social issues, abortion and gun control, were clearly won by Harris. Much more pragmatic and empathetic, she leveraged not only her status as a woman but also as a former prosecutor to win over the audience.

Similarly, climate change and the new economic model were strong points for Harris, who also skillfully navigated some contradictions in her record, such as her initial opposition to fracking. The IRA passed under Biden’s administration ensured, very cleverly, that a significant portion of foreign investment commitments would be directed toward Republican states, making it unlikely that the act would be overturned in the event of a Trump victory, as governors from both parties support the large associated stimulus packages.

There was only a degree of parity in foreign policy. Regarding current conflicts, as expected, Harris prioritized Zelensky and Ukraine, while Trump leaned toward Netanyahu and Israel. It is realistic to think that under a Democratic administration, the Middle East conflict would be more contained, with higher chances of resolution, while the war in Eastern Europe would likely continue. Conversely, under a Republican administration, the situation would reverse 180 degrees.

As things stand, it is still unclear to declare a clear winner, although Harris is clearly stronger and ahead. What can be said with relative certainty is that the popular vote will likely go to the Democrats, and it seems probable that the Senate majority will remain in Republican hands. In other words, even if Harris wins the election on November 5, it won’t be easy for her to pass legislative packages. The market has made its own reading of the results and has started pricing in scenarios.

Bitcoin dropped more than $1,000 after, indicative of Trump's poor performance, as he had forecast favorable policies for cryptocurrencies.

The dollar is weakening, as a Harris presidency is seen as more predictable and less explosive. In recent months, the dollar had acted as a safe haven. On the other hand, this could boost emerging currencies, especially with the upcoming interest rate cuts by the Federal Reserve next week.

Sectors linked to the energy transition are gaining ground, as there is a perception of favorable and consistent policies in support of climate change action.

Companies more exposed to China should benefit, as the chances of a new phase in the trade war are reduced. Look at Tesla or Apple, for example. Goldman Sachs designed two asset baskets, one aligned with the Democrats and another with the Republicans, and the trend of recent days will likely continue.

The release of the CPI data generated anticipation, not so much because of its direct relevance, but because it could clarify the outlook regarding the possible interest rate cut expected next Wednesday. The month-on-month CPI grew by 0.187%, aligning with forecasts, leaving the annual figure at 2.5%, marking a deceleration for the fifth consecutive month, reaching its lowest level since February 2021. On the other hand, core CPI grew by 0.281%, exceeding expectations of 0.2%.

While the annual drop of -4.0% in Energy and -1.9% in Basic Goods kept the CPI in line with the forecasted 2.5%, services continue to show persistently high inflation. Housing prices rose 5.2% annually, and Transportation increased by 0.9% monthly, remaining at a high +7.9% annually. Although the overall inflation in August is 2.5%, price increases in basic necessities are significantly higher:

Auto insurance inflation: 16.5%

Transportation inflation: 7.9%

Hospital services inflation: 5.8%

Homeowners’ inflation: 5.4%

Rent inflation: 5.0%

Car repair: 4.1%

Eating out: 4.0%

Electricity: 3.9%

h/t @ecommerceshares Right now, the market assigns a 40% chance of a 50 basis point rate cut on the upcoming 18th.

Apple unveiled its AI-powered iPhone 16 on Monday, just hours after its Chinese competitor Huawei announced its new three-part foldable phone, the Mate XT, which has already accumulated millions of pre-orders. Tim Cook, Apple's CEO, emphasized that the iPhone 16 'marks the beginning of a new era for Apple's intelligence,' indicating that the company designed this phone from the ground up to fully leverage its new AI software, called Apple Intelligence.

In an environment where major tech companies are fiercely competing to integrate AI into their products, Apple aims for these improvements to motivate consumers to upgrade their devices, despite the slowdown in iPhone sales. The software will be available in English in the U.S. next month and will expand to other languages, including Chinese, French, and Spanish, starting in 2024.

In contrast, Huawei has demonstrated its resilience in the face of U.S. sanctions with over 3 million pre-orders for its Mate XT in China. This highlights the Chinese market’s appetite for advanced AI features, where Apple faces growing domestic competition. Globally, while Western markets are more conservative regarding AI adoption, China shows more immediate interest in these features, which could complicate Apple's plans in the country, especially with the need to get its AI software approved under Chinese regulations.

This week, oil inventories in the United States have increased slightly: +0.83Mb, -1.7Mb in Cushing, +2.3Mb of gasoline, and +2.3Mb of distillates. The figure seems to reverse the trend of recent weeks, but paying a bit more attention to the details, we see that everything remains the same: net imports have increased by 1.5Mb/d, and they are 1Mb/d above the average of the last four weeks, which has generated a surplus of 7Mb this week, a cost paid by another region in the world.

We are now fully entering hurricane season in the Caribbean, and Francine, the most recent storm, is already affecting energy infrastructure in the Gulf of Mexico. The main impact analyses estimate that 24% of the region's oil and gas production (675kb/d and 0.91 bcf/d) has already been affected and is out of the market.

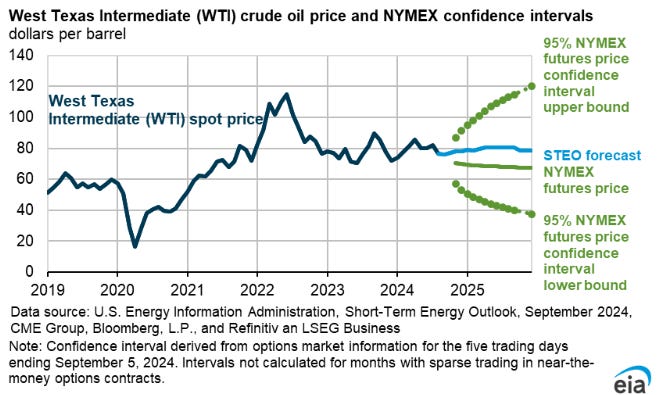

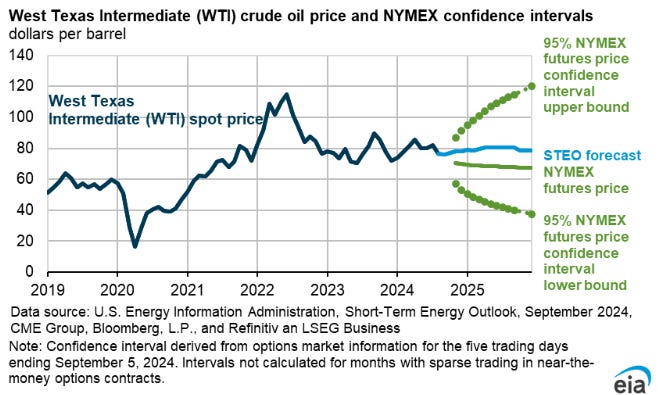

One of the most anticipated events was the release of the EIA’s STEO (Short Term Energy Outlook), where the agency publishes its market balance, trends, and price expectations for the coming year. This time, the message was surprisingly positive:

The agency now expects a deficit of 0.9Mb/d (previously 0.58Mb/d) for 2024 and a balanced market (previously a deficit of 0.1Mb/d) for 2025.

They believe Brent prices will rebound to $80/b this month and will average $82/b in Q4.

They have adjusted global demand for 2023 (as always, revised upward) to 102.1Mb/d compared to the previous 101.8Mb/d.

The consensus seems to be convinced that in 2025 we will see a surplus in the oil market balance, mainly due to two factors: 1) low growth in oil demand and 2) a significant increase in supply outside of OPEC. What is interesting is that, by reflecting these expectations in the price, the market itself alters the most probable future. Low prices tend to incentivize higher demand, while high prices destroy that demand. Similarly, low prices may discourage supply, while high prices encourage it. According to estimates from organizations like the IEA, EIA, and banks such as Morgan Stanley and Goldman Sachs, supply growth outside of OPEC in 2025 would range between 1.5 and 1.8 million barrels per day. However, with oil prices currently at $68 per barrel and projections of $66 for 2025, it is unlikely that supply will see any growth. U.S. shale is unprofitable, except in rare cases, at these levels, and for the first time in the last 15 years, we could even see a reduction in production.

Right now, sentiment is extremely negative, but eventually, the only thing that will matter are the fundamentals.

Model Portfolio

The model portfolio's return is +12.74% YTD compared to +17.08% for the S&P500, and +50.44% versus +38.43% for the S&P500 since inception (September 2022). The model portfolio, as of Friday's close, is as follows:

Keep reading with a 7-day free trial

Subscribe to LWS Financial Research to keep reading this post and get 7 days of free access to the full post archives.