Weekly summary 23/03

Weekly summary 23/03

The everchanging world order

Disclaimer

LWS Financial Research is NOT a financial advisory service, nor is its author qualified to offer such services.

All content on this website and publications, as well as all communications from the author, are for educational and entertainment purposes only and under no circumstances, express or implied, should be considered financial, legal, or any other type of advice. Each individual should carry out their own analysis and make their own investment decisions.

Weekly macro summary

There have also been quite a few interesting events to analyze, and below I list the most noteworthy news. Let's get started:

The Fed showed its most dovish stance at the March FOMC meeting. Although the interest rate decision was already known and remained unchanged, what truly mattered, as almost always, were the details, and in this case, Powell's subsequent message is what propelled the markets to new highs. The press conference, with a very accommodative tone, has revived animal spirits and inflation expectations, and the Fed has (re)demonstrated that it has not just two mandates but three, with this third one being the most relevant: the stability of the American Treasury.

The dot plot, which represents the graphical depiction of members' expectations for interest rate cuts, saw minimal changes, and the majority consensus remains at three cuts, although the number of participants expecting 4 or more cuts has been reduced (to just 1). Powell took care to confirm afterward that their restrictive monetary policy has already peaked and that they view the slight uptick in inflation in this first quarter as a mere bump in the road.

As highlighted at the outset, the real problem is that the government, despite the good employment situation, incurs a budget deficit of 6% of GDP, which is unsustainable in the long term, and whose only solution is to cut spending or raise taxes; since both paths seem unlikely, the only lever available is to lower interest rates to at least not add the burden of interest to the deficit.

I loved the book "Principles for Understanding the New World Order" by Ray Dalio, which analyzes the cycles of rise and fall of empires, their causes, and their consequences. In the following graph, we can see a classic archetype of these cycles, and if we are honest, the United States is at point number 15.

The Bank of Japan raised its benchmark interest rates for the first time in 17 years, to a range of 0.0-0.1%, thereby ending the longest streak of negative rates in a developed country. Additionally, on the liquidity front, they have decided to terminate their Yield Curve Control (YCC) program, which involved purchasing bonds to prevent an increase in interest rates. Pressures in wages (the largest negotiated increase by unions in the last 30 years, with a rise of 5.8%) hastened the central bank's decision, fearing excessive inflationary pressure if no action was taken.

The following graph is very illustrative, depicting debt as a percentage of GDP (x-axis) against interest rates (y-axis), reflecting a relationship contrary to economics textbooks: the higher the debt, the more pressure there is to keep interest rates low to avoid entering a debt spiral, such as the one Japan would suffer if it did not curb its leverage situation.

The crypto landscape never stops, and we've had another week of intense emotions. The SEC announced that it is investigating the Ethereum Foundation, considering this crypto asset to be a security, which would have severe regulatory implications and, at first glance, pushes back the expected approval of an ETH ETF in May. In the Bitcoin ecosystem, after weeks of massive capital inflows, we've had capital outflows every day due to the significant volumes exiting the Grayscale ETF, which has the highest fees. My opinion is that we will see a return to the bullish path in the coming weeks as RIAs (registered investment advisors) may begin to include and trade these vehicles on their trading platforms.

As a counterpoint, the mysterious buyer who has been acquiring packages of 100 BTC for over a year has resumed activity with renewed enthusiasm, taking advantage of the weakness in price these days.

The bullish gold market we are currently experiencing seems to still have room to grow. Global demand for the metal in 2023 was the highest ever recorded, driven by strong purchases from central banks, along with jewelry consumption, which offset net capital outflows from ETFs, particularly concentrated in the West.

Central banks, which had been net sellers until 2009, are accumulating gold at an unprecedented and increasing rate, which at first glance may seem counterintuitive in a fiat monetary system.

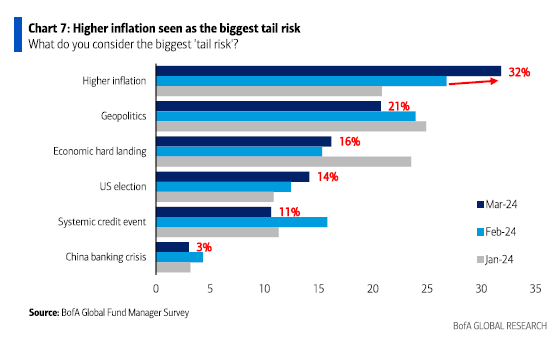

If we consider what the biggest concerns or tail events for the general public are right now, these movements make a lot of sense: the two perceived tail risk focuses are a new wave of inflation and the outbreak of a major geopolitical conflict, both scenarios where gold would play a key protective role.

In line with the first paragraph of this post, economic conditions in the United States, a proxy for the global market, seem to have stabilized, and most investors are already expecting a no-landing scenario, meaning completely avoiding an economic recession.

Nevertheless, the data continues to be mixed, and although there are reasons for optimism, one of the most worrying and attention-grabbing is the huge rise in interest payments, which now exceed hourly wage income, an indicator that has proved to be prescient in the last two crises.

Nvidia has held its annual artificial intelligence developers' conference, where they showcase their new products and discuss the latest trends and advancements in the sector, with room for other companies to also share their ideas. The standout announcement was the unveiling of their new product, Blackwell, a chip that is 30 times faster than its predecessor for tasks such as generative AI, and with 25 times lower energy consumption, demonstrating the speed and scale of innovation in the current era. The new chips are expected to hit the market by late 2024 and will cost between $30,000 and $40,000 per unit; to celebrate the launch, Nvidia has announced a new collaboration with Oracle and Chinese automotive companies, such as BYD, to further define the new phase of AI.

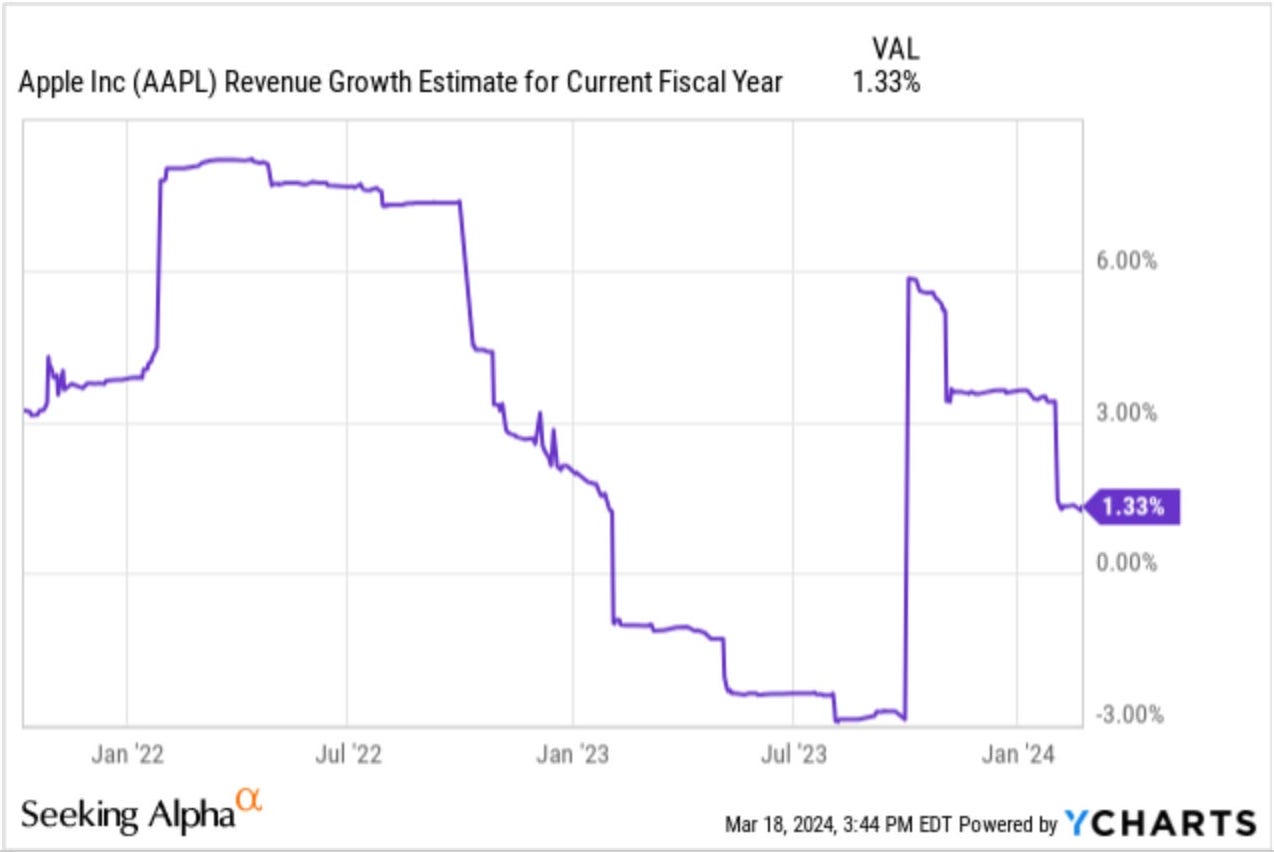

Apple has clearly fallen behind in the race for AI and will entrust GOOG 0.00%↑(it's the worst technology, but it can't be associated with $MSFT) with the implementation of these services on its devices. The Cupertino company has gone years without innovating significantly (if we overlook removing the headphone jack) and has transitioned into a mature services and aspirational fashion company, which is how, in my opinion, the market will ultimately value it.

Its finances reflect this, and after the tailwinds from COVID, its revenue growth has slowed significantly, even marking negative comparables last year (and, in any case, real negative growth since 2022).

As is often the case, when it rains, it pours, and the Department of Justice has sued Apple for monopolistic practices in the marketing of its flagship product, the iPhone. It's not the first time they've faced accusations, which tend to be good buying opportunities, as they are usually temporary problems; this time, however, it adds to the long list of issues plaguing the Californian company.

We continue with the streak of positive oil inventory reports: -1.952Mb of crude, -0.018Mb in Cushing, -3.31Mb of gasoline, and +0.624Mb of distillates, meaning a simultaneous drop in crude and products, which brings the total for the year to levels clearly lower than those of 2023.

Oil, buoyed by this positive fundamental development, has risen nearly $10/b since the beginning of the year, with refining margins and physical timespreads supporting such movement (sustainable and healthy), while investor positioning remains at lows, which could add significant upside potential to an upward movement if sentiment were to reverse.

We highlighted last week that the IEA had been forced to revise its estimates of oil demand upwards, given the stubbornness of reality, and now it expects an increase in oil consumption of 1.5Mb/d for 2024 (still far from the 2.2Mb/d forecasted by OPEC); to deepen the credibility crisis of the agency, a group of US politicians issued a statement this week accusing them of having a political bias, which is especially relevant considering that their reports often shape market consensus.

In the context of the armed conflict in Ukraine, Kiev has launched attacks on Russian refineries, reducing the country's refining capacity to its lowest level in the last 10 months. As always, everything is political, and despite the success achieved (or precisely because of it), the United States has asked them not to continue with these attacks, as there is a risk of significantly affecting oil production in Russia and destabilizing crude oil prices, which would be very negative in an election year.

Model Portfolio

In a deja vu of 2021, the fever of IPOs at ridiculous valuations has returned with force. Reddit, one of the largest and most active forums, went public on Thursday and had a 60% appreciation in its first hours on the market. The company has an interesting value proposition, with 73.1 million daily active users and over 100k active communities, making the value of data and network effects clear, but its valuation doesn't quite add up:

After the 60% increase, Reddit's market capitalization is $9.5 billion, and in 2023 its net result was -$90.8 million, with a revenue growth of 21%, up to $804 million. Thus, the valuation by multiples places it at 11x P/S (it has no earnings), with a business model with a certain risk of terminal value and growth that, while not insignificant, does not justify these excesses.

Regarding the model portfolio, this week has been spectacular, with very positive returns on several of our ideas that position us very well to meet the objectives of each year:

Positive and double-digit profitability.

Outperforming benchmark indices.

Focus and accuracy.

The model portfolio return is +7.65% YTD vs +9.44% for the S&P500 and +43.83% vs +30.96% for the S&P500 since inception (September 2022).

Keep reading with a 7-day free trial

Subscribe to LWS Financial Research to keep reading this post and get 7 days of free access to the full post archives.