Weekly summary 21/09

Weekly summary 21/09

Behind the curve

Disclaimer

LWS Financial Research is NOT a financial advisory service, nor is its author qualified to offer such services.

All content on this website and publications, as well as all communications from the author, are for educational and entertainment purposes only and under no circumstances, express or implied, should be considered financial, legal, or any other type of advice. Each individual should carry out their own analysis and make their own investment decisions.

Weekly macro summary

There have also been quite a few interesting events to analyze, and below I list the most noteworthy news. Let's get started:

The U.S. Federal Reserve has begun its rate-cutting cycle, joining other major central banks such as the ECB and BoE. The market had already priced in this cut but was awaiting the magnitude of it, where opinions were divided. They have decided to start with a 50bps cut, that is, in the most aggressive manner possible. Much has been written about whether this choice is positive or negative, suggesting that the underlying economic reality is more concerning than it appears. In my opinion, it is clearly positive: the underlying economic reality, whether good or bad, is independent of the Fed's decision, but the 50bps cut stimulates the economy more and accelerates recovery faster than a 25bps cut would. Additionally, the mistake of not cutting rates in July has now forced them to make both cuts at once.

Powell’s subsequent press conference was the most interesting part, and the Fed chairman managed to calm concerns and convey confidence in the work done:

We do not believe we are behind the curve… but you can take this cut as a commitment to not falling behind.

Projections show that we expect GDP growth to remain solid.

Inflation has decreased significantly but remains above target; long-term inflation expectations seem to be well anchored.

The reality is that they are indeed very much behind the curve, and that the current economy, coupled with the massive fiscal deficits the country is running, can only function in an artificially low interest rate environment, meaning there is a long path ahead for rates to fall.

Growth estimates, such as the Fed’s Atlanta GDPNow, show a higher forecast for expansion (3%). My opinion is that in the coming months, we will see negative employment data, and after an initial 50bps move, the Fed will be forced to repeat the size of the cuts in subsequent meetings.

The market, as expected, reacted as it always does: after the initial move, which is the real one, it reverses the path, then resumes with Powell’s speech, only to reverse again.

h/t Incomesharks The last few times when the rate-cutting cycle started with a move of 50bps or more, overall stock market performance has been positive, even in the face of a recession. However, it is true that in more recent examples, the behavior has been the opposite. More than $6T is now sitting in money market funds, which is attractive at 5%, but what will happen when rates drop to 3%? Until (a significant) part of this liquidity returns to the market, I don't think it makes much sense to expect a crash.

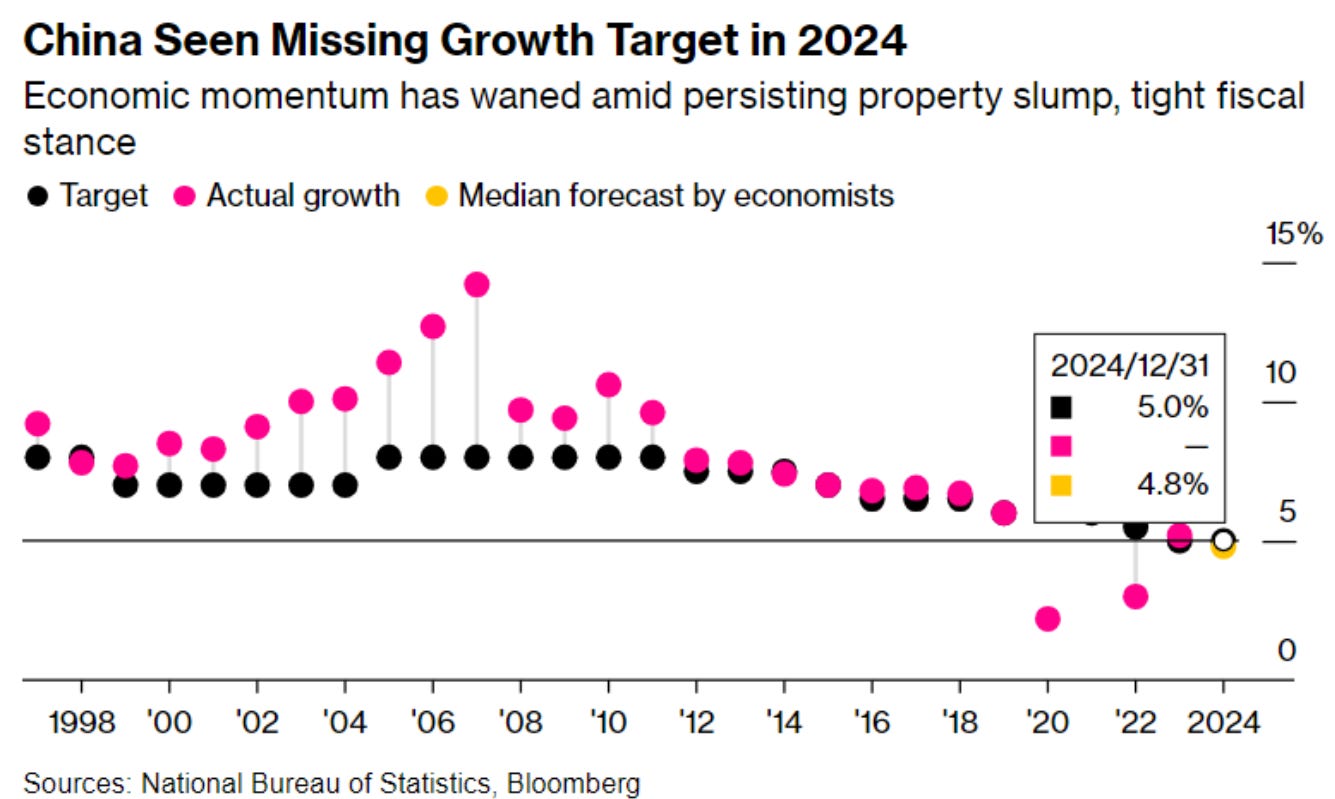

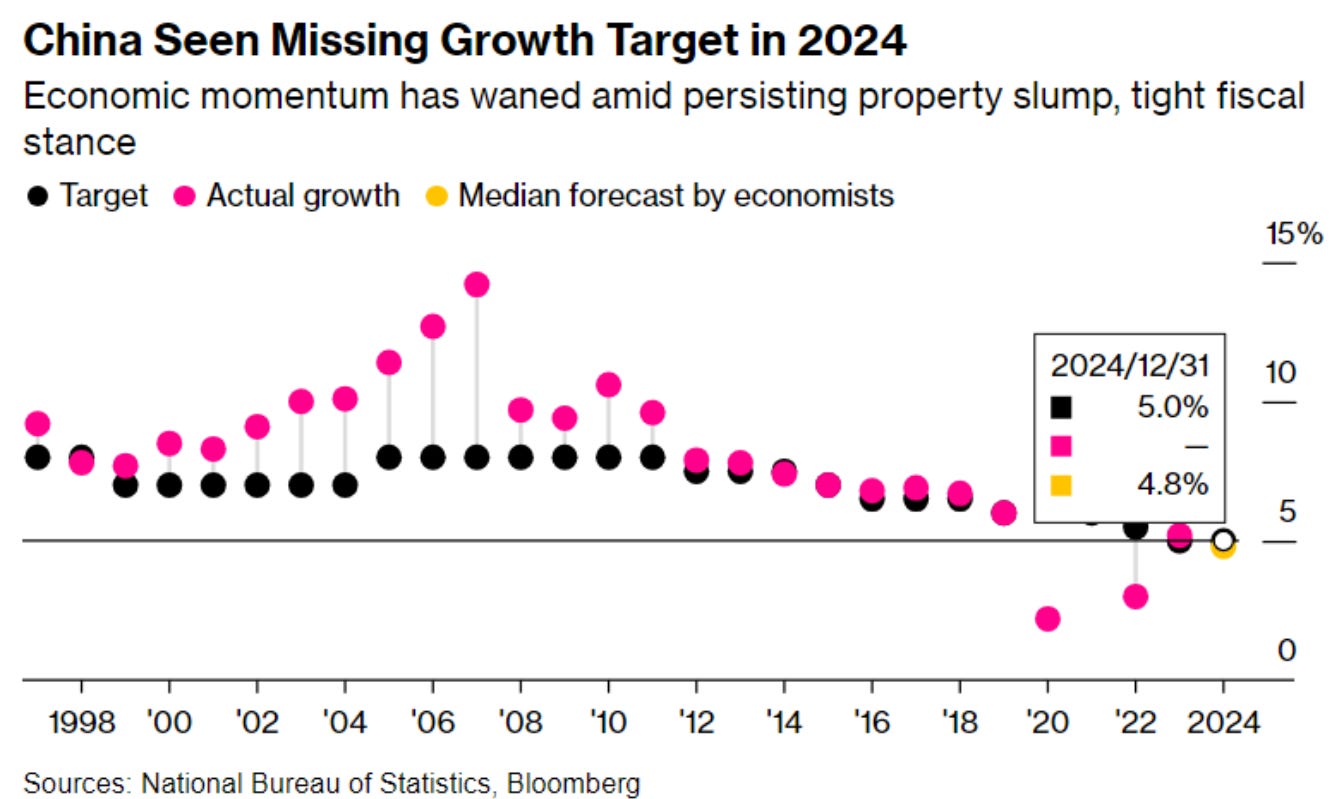

The commodities market has been waiting for some sign of China's recovery to restore optimism, and it seems this development may arrive soon. Xi Jinping has urged Chinese officials to meet the annual growth target, emphasizing the importance of implementing the Central Committee's major economic initiatives to ensure development goals are achieved in the remainder of the year.

Despite government efforts, including interest rate cuts, the economy continues to rely on manufacturing and exports to maintain its pace. Recent data shows a slowdown in industrial production for the fourth consecutive month, the largest in nearly three years.

The central concern is that, despite the measures taken, the Chinese economy continues to show signs of weakness, which reinforces the urgency for additional policies to meet the government's ambitious growth targets. As a first step, a further rate cut (50 basis points) is being considered to ease pressure on mortgages and encourage consumption.

Growth in China | Bloomberg Japanese automakers in Indonesia are facing increasing challenges in retaining their key employees as Asian rivals, such as BYD, aggressively enter the market. BYD, the Chinese electric vehicle manufacturer, is building a $1 billion plant in West Java province with the capacity to produce 150,000 vehicles annually, and is using its market entry to lure talent from Japanese companies already operating there, like Toyota, which has dominated 90% of the market since its arrival in the 1970s.

BYD's case is not unique. Hyundai also entered Indonesia in 2022 with a plant of similar capacity, using similar talent attraction strategies. The South Korean automaker offered generous salary packages, up to three times what employees earned at Japanese companies, to attract experienced executives.

The competition for talent in Indonesia highlights a bigger issue: the declining appeal of Japanese companies as employers in the region. Key reasons include the lack of upward mobility for local staff and lower wages compared to other multinationals.

This problem is not limited to Indonesia. The wage gap between Japan and other markets, such as India, has drastically narrowed. Information technology engineers who used to earn 50% to 100% more in Japan now find similar salaries in their home countries.

Mario Draghi presented his report on Europe's competitiveness last week, and the conclusions are bleak. Below, we highlight the most relevant messages.

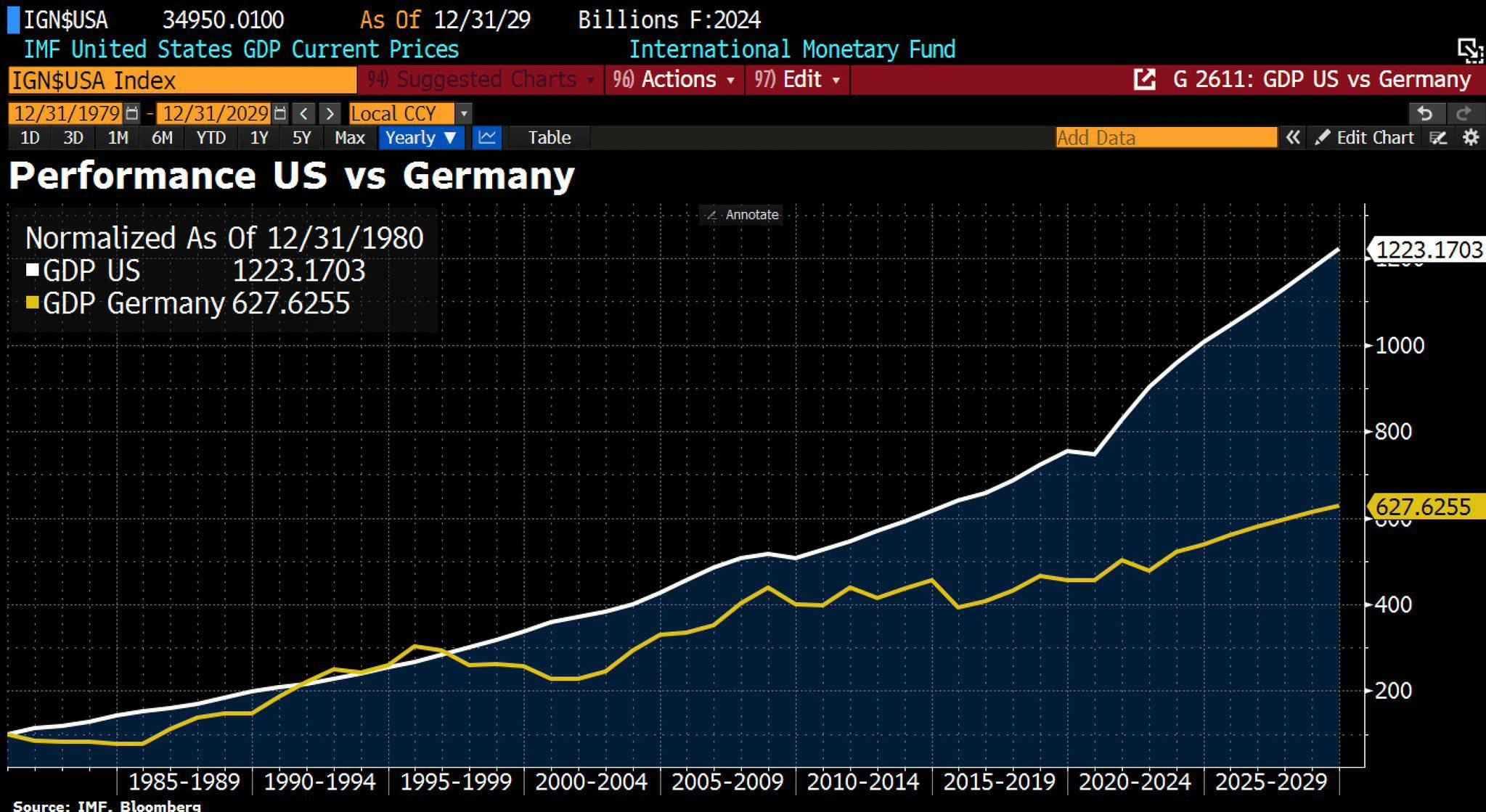

Growth in Europe has been declining for decades, and the GDP gap between the European Union and the United States has widened significantly. This has had a direct impact on European households, whose disposable income has grown at nearly half the rate of Americans since 2000. While this slowdown was, for a long time, more of an inconvenience than a crisis, the landscape has now changed dramatically. With a declining population, the EU is increasingly dependent on productivity to drive its growth. If European productivity continues to grow at the current rate, it will only be enough to maintain a stable GDP until 2050.

As the need for growth rises, the EU faces monumental challenges: digitalizing, decarbonizing the economy, improving its defense capabilities, and maintaining its social model in an aging society. The necessary investments are colossal; it is estimated that investment will need to increase by five percentage points of GDP, a level not seen since the 1960s and 1970s. This is much larger than the contributions of the Marshall Plan, which represented 1-2% of annual GDP between 1948 and 1951. Three key areas stand out where efforts must focus to revitalize competitiveness:

The first is closing the innovation gap with the United States. Europe has lagged behind in the digital revolution, and its weakness in emerging technologies is concerning. Although Europe has innovative ideas, these do not translate into commercial products. European companies face restrictive regulations and a lack of financing, leading many entrepreneurs to seek capital in the U.S.

The second focus area is combining decarbonization with competitiveness. Europe leads in clean technology innovation but faces higher energy costs compared to the U.S., which could slow growth if the benefits of renewable energy are not managed properly.

Lastly, the report highlights the need to improve security and reduce dependencies. Europe is vulnerable due to its reliance on a few suppliers for critical raw materials and digital technology. To address this challenge, the report urges the EU to develop a strong external economic policy, foster industrial partnerships, and increase its defense capacity.

Financing these investments will be crucial, and while Europe has a high level of private savings, greater public intervention is required. Draghi emphasizes that without structural reforms, the EU will face difficult trade-offs between welfare, the environment, and freedom.

The drama between Nippon Steel and U.S. Steel has intensified following national security concerns raised by the U.S. government regarding the planned acquisition of U.S. Steel by the Japanese company. In a meeting with Treasury Department officials, Nippon Steel, represented by its Vice President Takahiro Mori, sought to clarify its position amid growing opposition to the purchase.

The Committee on Foreign Investment in the U.S. (CFIUS) expressed concerns about two key points: the possibility that Nippon Steel could transfer U.S. steel production capacity to India, and the company's resistance to U.S. trade policies, such as increasing tariffs on products imported from China. Nippon Steel has attempted to counter these claims, assuring that its commitment to the U.S. market remains firm and proposing the creation of a trade committee composed of U.S. citizens to oversee trade matters at U.S. Steel.

The situation is further complicated by differing opinions within CFIUS itself. While some departments, like State and Defense, view the U.S.-Japan relationship as a strategic priority, bipartisan opposition in Congress represents a significant hurdle to the acquisition's approval.

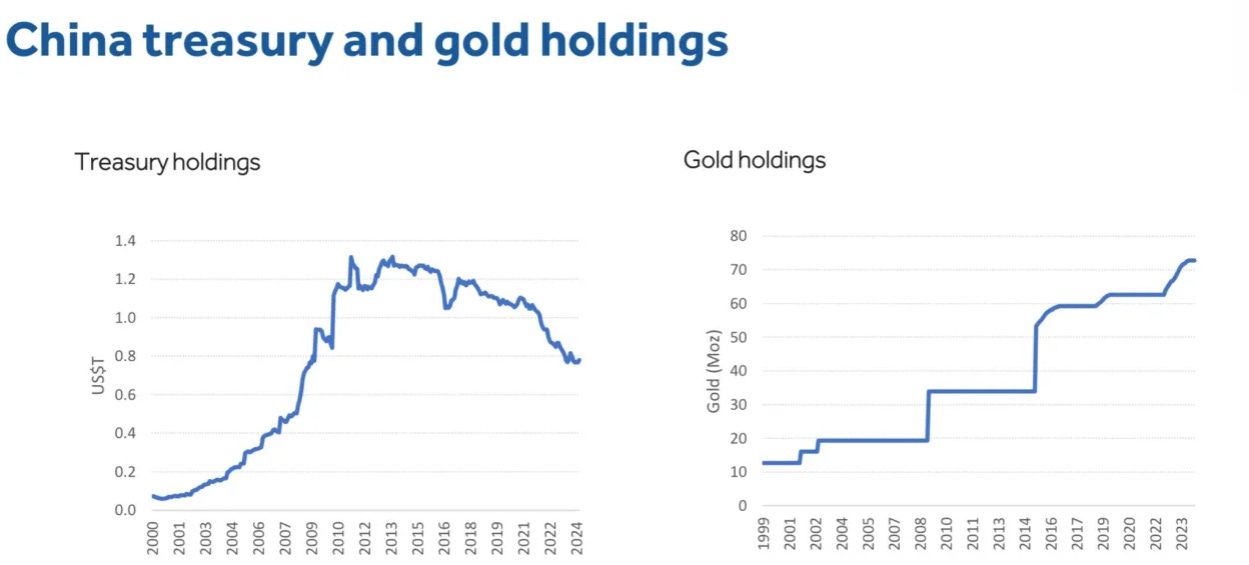

Gold has once again reached record highs, accumulating an appreciation of more than 25% so far this year. Central banks have been the main drivers so far, but with the start of the rate cut cycle, it's likely that individual investors will join the trend. In any case, the transition to a harder currency (and the move away from the dollar) by non-Western countries will likely continue as an unstoppable trend.

In the digital counterpart, it seems that the cycle is speeding up again. MicroStrategy, Michael Saylor's company, has announced the issuance of debt worth $1.01B (initially $700M) at an interest rate of 0.625% (!!) to buy more Bitcoin.

Some countries (remember, slowly at first, then all at once) are starting to adopt (and report) this asset as part of their monetary reserves, with Bhutan being the most recent example. The Asian country has accumulated 13,011 BTC, which places it 5th in the global race for Bitcoin adoption (not bad for a country ranked 153rd in global wealth).

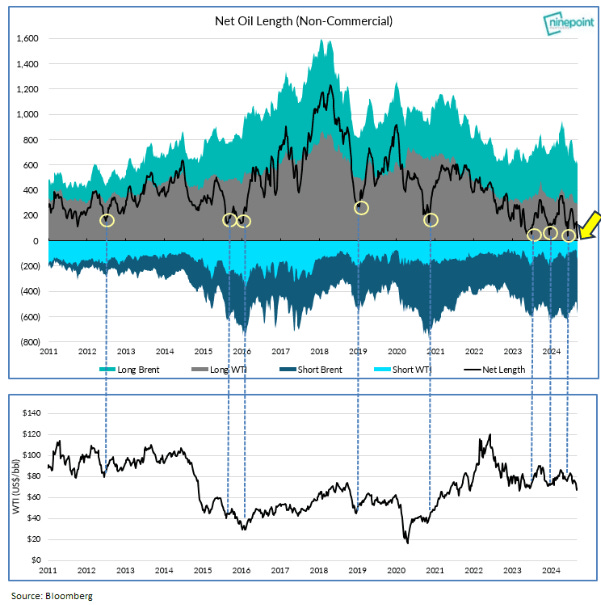

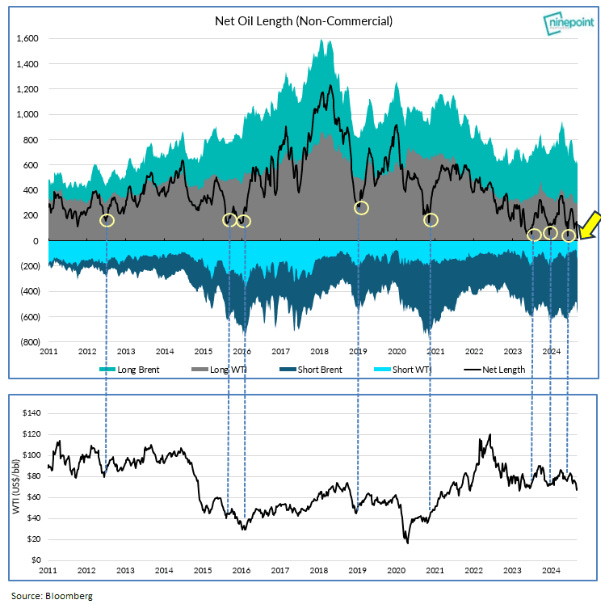

Another week, another drop in oil inventories: -1.63Mb of crude, -1.979Mb in Cushing (!!), +0.07Mb of gasoline, and +0.125Mb of distillates. Global inventories fell by 47.1Mb in July, which implies a deficit of 1.6Mb/d. Despite all the talk about weak demand in China, crude imports have risen significantly this month and inventories haven’t increased, suggesting that consumption has rebounded.

A lot has been written this week about oil’s financial positioning, which has turned negative for the first time—meaning sentiment has never been as negative as it is now, a view that doesn't quite align with the underlying reality. In the following chart (h/t Eric Nutall), we can see how much of this year’s volatility has been caused by this very positioning. What has been a headwind and obstacle until now could quickly turn into a catalyst, as we saw in 2022. These extreme positions, especially when largely based on sentiment, tend to behave like a pendulum.

Model Portfolio

The model portfolio's return is +13.55% YTD compared to +18.67% for the S&P500, and +51.25% versus +40.02% for the S&P500 since inception (September 2022). The model portfolio, as of Friday's close, is as follows:

Keep reading with a 7-day free trial

Subscribe to LWS Financial Research to keep reading this post and get 7 days of free access to the full post archives.