Weekly summary 25/05

Weekly summary 25/05

Hanging by an Nvidia

Disclaimer

LWS Financial Research is NOT a financial advisory service, nor is its author qualified to offer such services.

All content on this website and publications, as well as all communications from the author, are for educational and entertainment purposes only and under no circumstances, express or implied, should be considered financial, legal, or any other type of advice. Each individual should carry out their own analysis and make their own investment decisions.

Weekly macro summary

There have also been quite a few interesting events to analyze, and below I list the most noteworthy news. Let's get started:

The success of GLP-1 in weight loss products (initially with another function) from Novo Nordisk, Ozempic, and Wegovy, is transforming other adjacent industries, and competitors in their category are already starting to appear.

$HIMS, a competitor, has already launched a generic product, much cheaper than Novo's, which could capture a large share of the market reached by these drugs.

Other brands, such as Nestlé, have decided to play a second derivative, launching a new line of high-protein foods, designed to compensate for the loss of muscle mass and specific needs resulting from regular GLP-1 consumption.

The European Union has agreed to use the accrued interest generated by the Russian funds deposited in the ECB, which have been frozen for the past two years, to support Ukraine. It is estimated that the annual amount generated will be around €2.5B-€3B, adding to the initiative proposed by Yellen to do the same with the capital held in the USA.

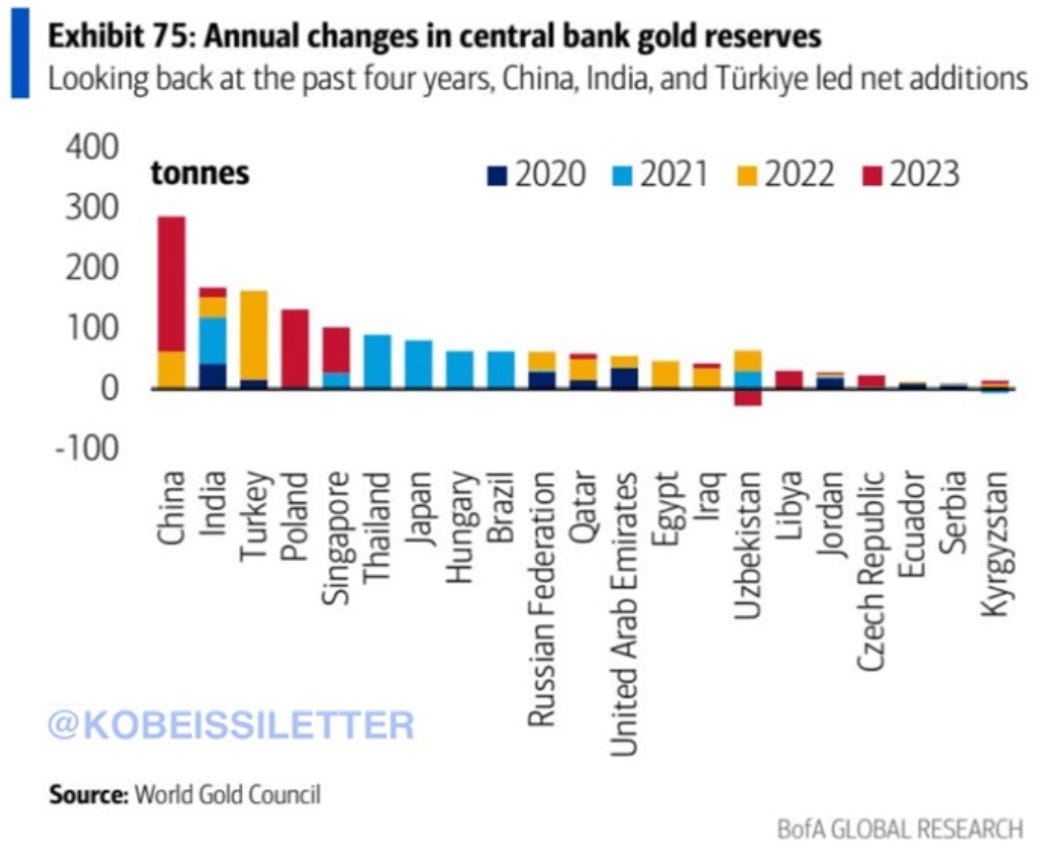

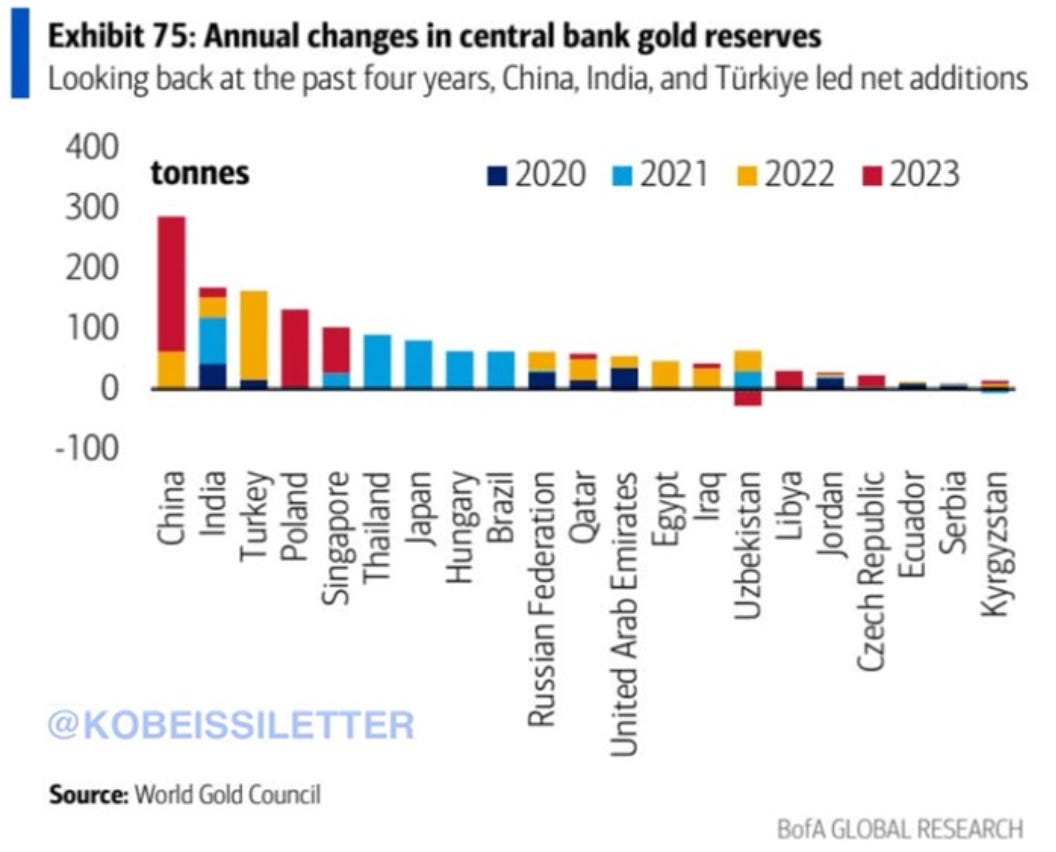

This move, which may seem morally correct to many and even politically reasonable, is actually another nail in the coffin for the dollar (and the Euro, of course). It serves as a warning to other countries not part of the OECD: not your keys, not your coins. It is no surprise, therefore, that countries like China are accelerating their gold purchases to boost their reserves at the highest rates in decades, opening a new dimension to the nascent gold bull market.

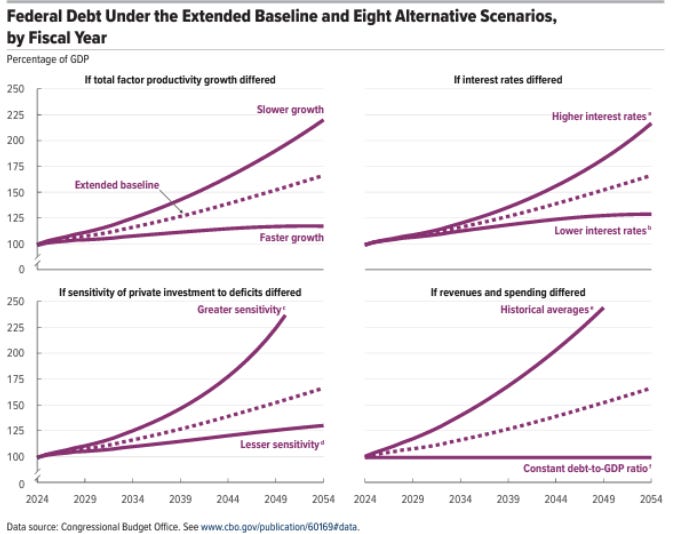

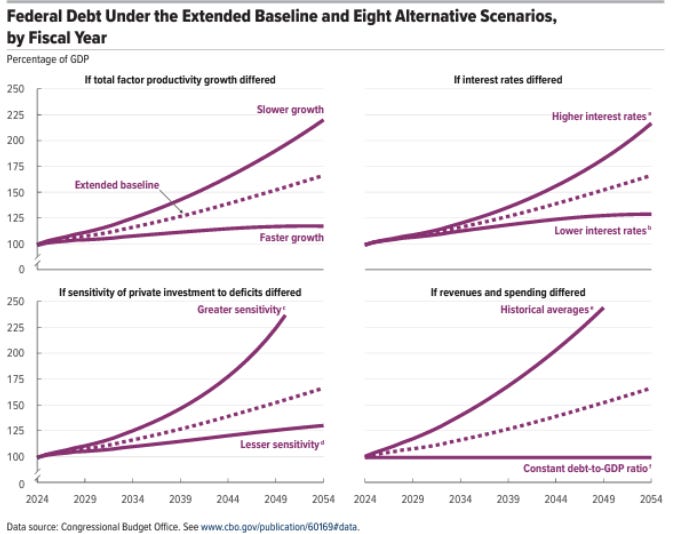

The Congressional Budget Office (CBO) of the USA has conducted a sensitivity analysis of the country's debt relative to its GDP. The conclusions are devastating, as the trend is certainly worrisome and highly sensitive to negative surprises. The following points are highlighted:

Productivity: If labor and capital productivity in the non-agricultural business sector grows 0.5 percentage points faster or slower than projected, public debt in 2054 would be 124% or 211% of GDP, respectively.

Interest rate: If the average interest rate on federal debt is 5 basis points higher or lower than projected, debt in 2054 would be 217% or 129% of GDP, respectively.

Private investment: If government borrowing reduces private investment twice as much as projected or has no effect, debt in 2054 would exceed 250% of GDP or be 130%, respectively.

Discretionary spending and revenues: If between 2024 and 2054 discretionary spending and revenues match their historical averages of 30%, debt in 2054 would exceed 250% of GDP.

Fiscal policy: If fiscal policy is adjusted to maintain public debt at 99% of GDP (2024 level), primary deficits would average 0.4% of GDP, reduced through either a decrease in non-interest spending or an increase in revenues.

The two main political parties in the United States are rapidly changing their stance on cryptocurrencies in general and Bitcoin in particular.

I like the dollar, but many people are doing it [using Bitcoin], and frankly, it’s taken a life of its own. You probably have to do some regulation, as you know, but many people are embracing it. And more and more, I’m seeing people wanting to pay Bitcoin, and you’re seeing something that’s interesting. So I can live with it one way or the other.

— Donald Trump

Seeing that the pro-crypto voter base is large and growing, the Democratic Party, which has been highly critical of the space until now, has changed its stance overnight. This is evidenced by their statement expressing a willingness to work on developing an appropriate regulatory framework for digital assets and their shift in position on Ethereum ETFs, which went from being ruled out last week to being confirmed this week. There is no choice but to adapt, as Trump's lead is large and growing in all key election states.

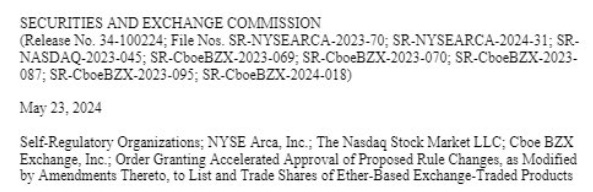

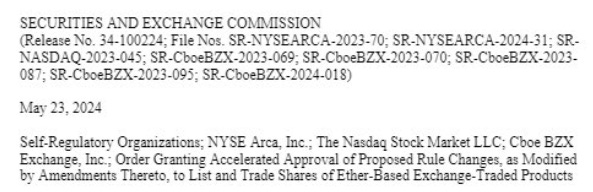

On Thursday, after the market closed, the SEC gave the green light for the launch of these vehicles, making a 180º turn from their stance less than a week ago. Unlike with Bitcoin ETFs, where everything was already prepared, the speed of this process means they won’t start trading for about two weeks, once the final S-1 documents are approved. Patience.

The United States Congress has also reclaimed its mandate and passed the CBDC Anti-Surveillance Act, in favor of individual freedom and privacy. This act prevents the FED from creating a CBDC that involves control and surveillance over American citizens, thus avoiding the dystopia we seem to be heading towards.

After a two-week pause, and seeing how the world's largest hedge funds announced their participation in these vehicles in the 13F filings, ETFs have once again accelerated their net capital inflows.

As Kuppy noted in his article "The Blowoff", this bet now becomes a game theory experiment: the incentives in the capital management industry are perverse and do not allow for relative underperformance among funds. Thus, if the idea works, those without exposure are forced to incorporate it to avoid experiencing an outflow of funds under management, creating a virtuous circle.

Cleared for launch.

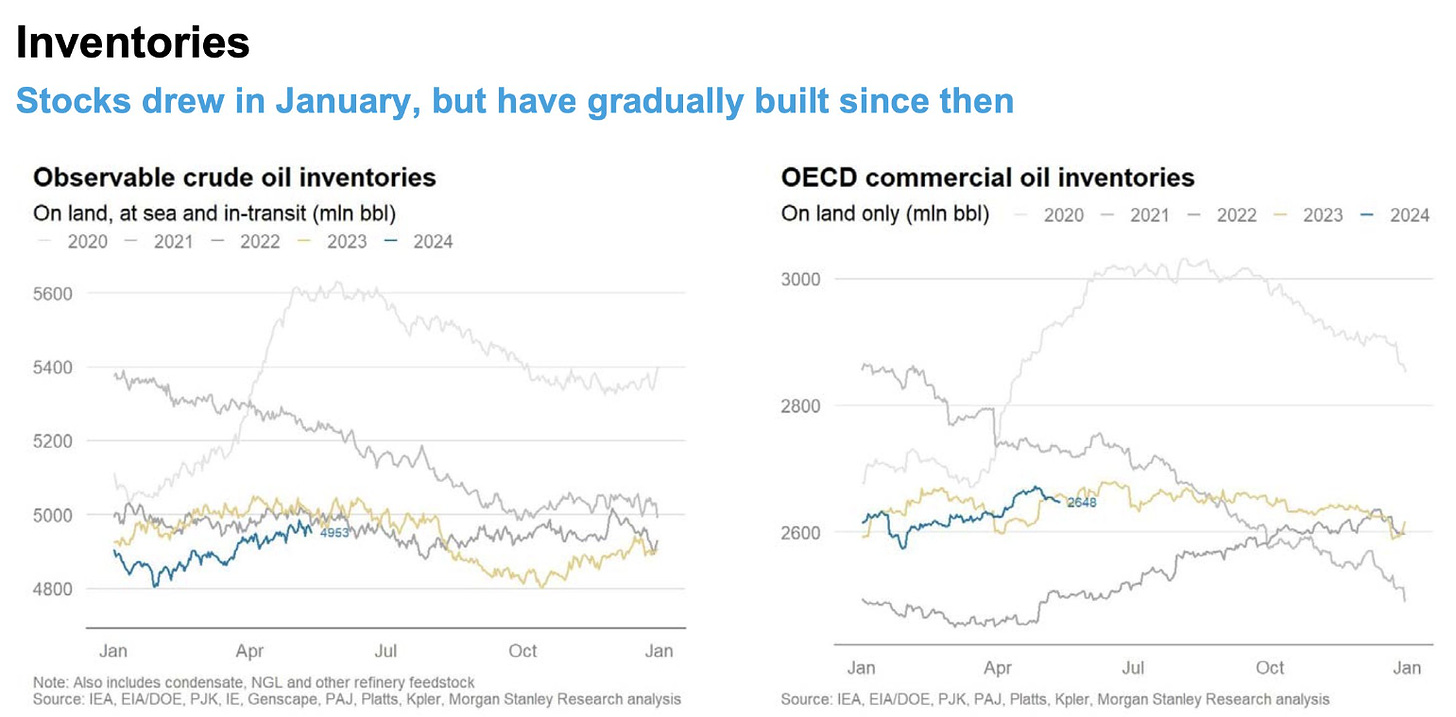

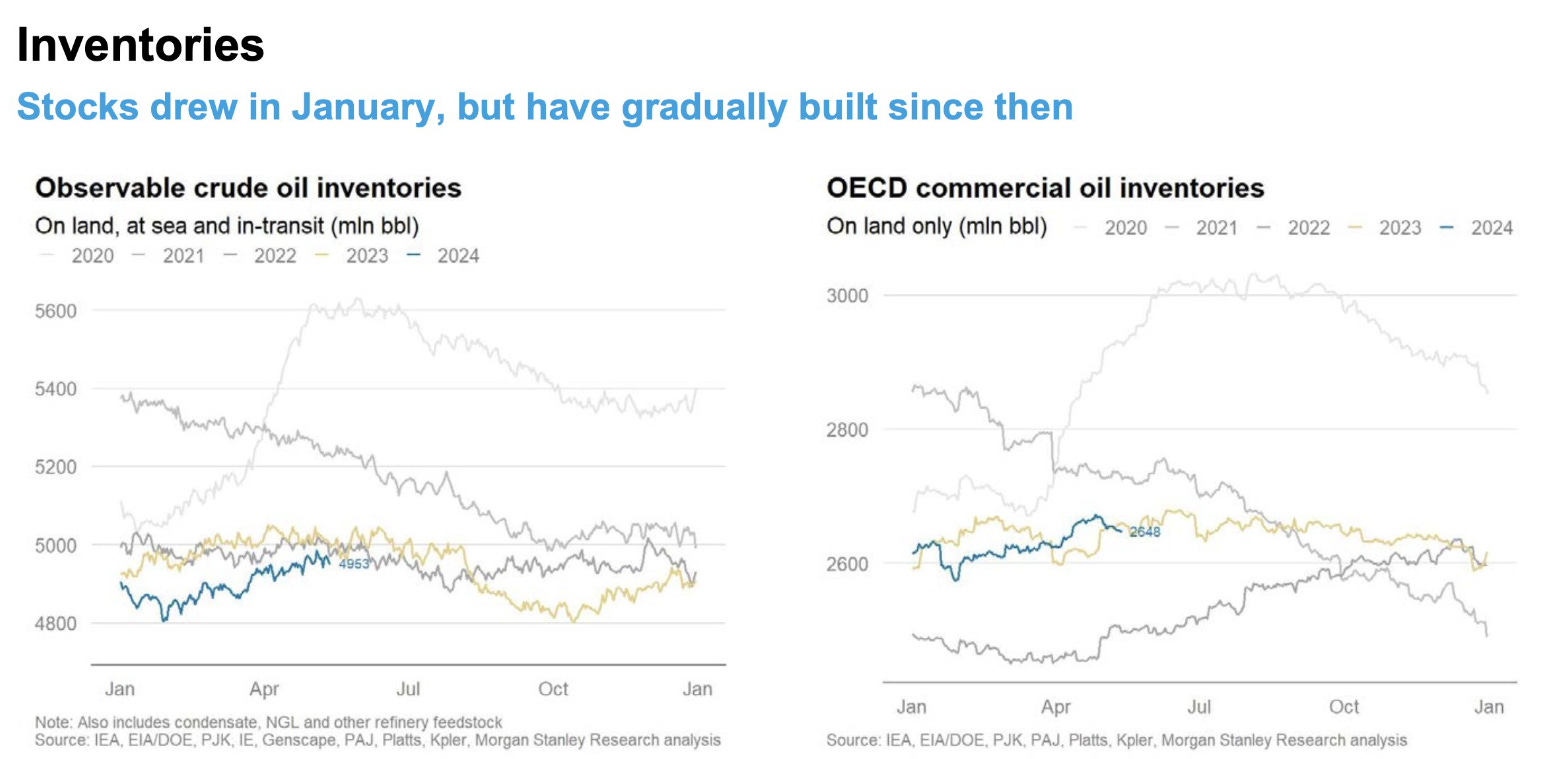

This week's EIA oil inventories were surprisingly negative, especially ahead of several key dates with strong demand: +1.825Mb of crude oil, +1.32Mb in Cushing, -0.945Mb of gasoline, and +0.379Mb of distillates. The good figures from January had suggested a 2024 marked by large deficits, in which OPEC would be forced to reverse the voluntary cuts of 2023. However, with five months elapsed, we see that global inventories have not only not fallen but have increased significantly. The internal disarray within the cartel and pressure from other members have led Iraq, which had been significantly increasing its production, to cut its output by 100Kboe/d, which will hardly be enough to reverse the trend.

Analyzing demand trends by country (actually, imports, which do not exactly equate to consumption), we see mixed figures. Countries like China, India, and the United States are registering strong increases, while others like Italy, France, Germany (it's unusual to see Europe on the podium for decline), and Thailand are showing decreases.

The Biden administration is no longer hiding in the final sprint before the elections and has decided to release 1 million barrels from the Northeast gasoline reserve to lower fuel prices before Memorial Day and the 4th of July. It is inevitable that the consumption of gas and coal will continue to increase at high rates, as the improvement in living standards for a vast demographic depends on it. In India, recurring blackouts (affecting 38% of households) are occurring due to increased consumption from the heatwave they are experiencing, which has increased the demand for coal and LNG. Such situations, more common than we might think, are a top priority for the countries experiencing them, where energy security takes precedence over climate impact.

Model Portfolio

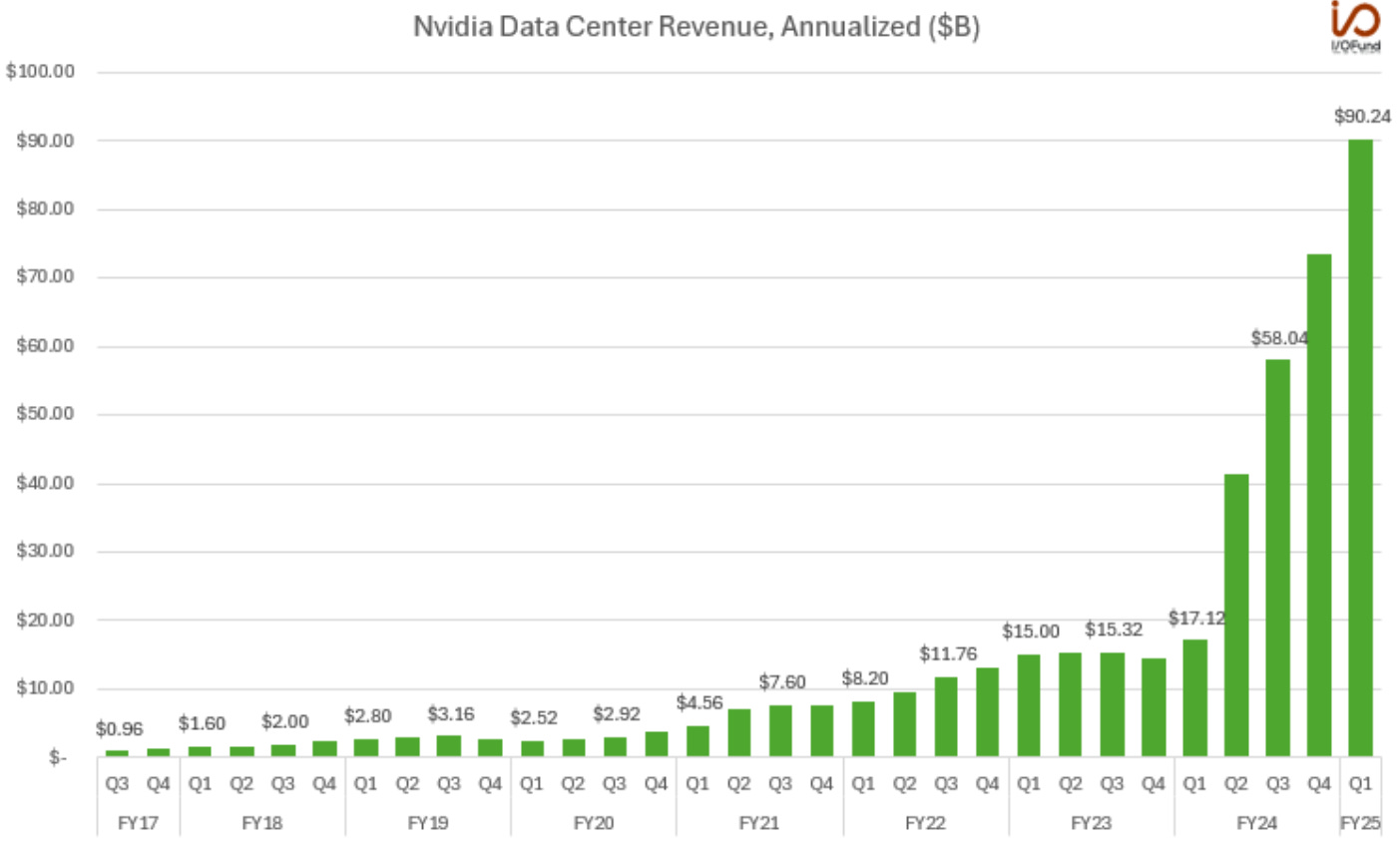

All eyes were on Nvidia's results, which, like Apple's previously, seem to be the reflection and support of the market: if Nvidia did not meet (in fact, if it did not beat) the estimates, the market was at risk of collapsing. Fortunately (for those involved), the company exceeded expectations, beating even the most optimistic forecasts.

In addition to the extraordinary figures, the guidance for Q2 was equally surprising ($28B, $2B above expectations), and they combined the announcement with a 10-1 stock split, so each share will be worth 10% of its current price, making it more accessible to retail investors. The market rewarded the report with a 10% price increase, pushing the price above $1000 per share.

With this new milestone, Nvidia has surpassed in size (though not comparable) the GDP of all countries in the world except seven, the combined GDP of Spain and Saudi Arabia, the market capitalization of Walmart and Amazon combined, and the value of the entire German stock market. It is only 15% away from becoming the second most valuable company in the world.

Nvidia stood alone in this upward momentum, with almost all other companies falling on Thursday. This is not the image we would expect from a healthy market with sustainable valuations. Such narrow breadth, even with the good news from the clear market leader, is a signal to watch closely.

The model portfolio's return is +20.98% YTD compared to +10.89% for the S&P500, and +57.85% versus +32.27% for the S&P500 since inception (September 2022).

Keep reading with a 7-day free trial

Subscribe to LWS Financial Research to keep reading this post and get 7 days of free access to the full post archives.