Amerigo Resources

Recycling copper

Disclaimer

LWS Financial Research is NOT a financial advisory service, nor is its author qualified to offer such services.

All content on this website and publications, as well as all communications from the author, are for educational and entertainment purposes only and under no circumstances, express or implied, should be considered financial, legal, or any other type of advice. Each individual should carry out their own analysis and make their own investment decisions.

Note: This article has been updated as of 02/26/2025. The original release was on 02/25/2024, when the stock was trading at C$ 1.32/share.

Introduction and business model

The business model of Amerigo Resources is very interesting and, in a certain way, similar to that of Dynacor Group, a company we have already analyzed and which has had a magnificent performance: Amerigo owns 100% of Minera Valle Central S.A (MVC), located in Chile, which has a long-term contract with the El Teniente Division (DET), the largest underground copper mine in the world. Under this agreement, MVC processes both new and historical tailings (material left over from the initial mineral processing, which does not extract all of the content), and obtains copper and molybdenum, which it sells at market prices. MVC generates revenue from the sale price of copper and incurs processing and refining expenses, royalties paid to DET, and transportation costs.

The Teniente mine, from which the tailings are obtained, began production in 1905, and it is estimated to remain active until 2082, making the supply for Amerigo practically infinite, and the jurisdictional and counterparty risk is negligible or very low as it operates with Codelco, the Chilean state-owned mining company. The agreement is valid until 2037 for the new tailings and until 2033 for the old ones, although it can be extended further; Amerigo estimates that the chances of early termination or non-renewal are very remote. Processing costs (~$2/lb) are high, mainly because most of the copper has already been extracted by Codelco.

The royalties paid to Codelco are proportional to the copper price and follow a predefined scale within the range of $1.95/lb to $4.8/lb; if the metal price remains sustained (for more than a quarter) outside this range, both parties will meet to agree on the specific amount to be paid. As a reference, a $0.20/lb increase in the copper price would entail a $0.1/lb change in royalties for DET.

In the finance and operations section of the investment thesis, we will delve into all the financial figures and projections to see what cash generation capacity the company has with current copper prices and put them into context regarding its valuation.

But... does investing in copper make sense? What are its prospects?

Copper investment thesis

Copper is one of the metals considered key for the development of nearly all current transformative megatrends, being the best electrical conductor in nearly any situation.

Despite efforts to find viable alternatives, copper remains the best-known conductor and will likely continue to be the preferred choice for most applications and uses unless significant deficits occur. A period of very high prices would be beneficial for mining companies, but there is a risk of demand destruction. In fact, during the period from 2000 to 2015, aluminum, much cheaper but with poorer conductivity, began to be used for many transmission lines.

Applications cover many transformative trends, such as electrification or renewable energies, although one of the most prominent is their application in BEV (Battery Electric Vehicle) technology. Electric vehicle designs are evolving to use less copper, which, combined with the slower adoption rate of this technology (compared to consensus), may lead to deviations from analysts' projections, although it is true that almost all simple substitutions have already been made.

Over the past decade, and perhaps generating excessive expectations, China's demand (and its growth), particularly in the construction sector, was truly remarkable. However, with the current real estate crisis the country is facing, along with economic slowdown and weakness in its manufacturing sector, doubts have emerged about the sustainability of this upward trend. Nevertheless, investment in infrastructure and energy transition (both in renewable energy itself and electrification) should offset this weakness, especially as the macroeconomic situation and restrictive monetary policy improve. In fact, it is likely that in March, after the two sessions of the CCP, we will see the announcement of a real stimulus package, as failing to do so would make it nearly impossible for China to reach its 5% growth target. Additionally, taking over from China, other Asian countries are experiencing a demand boom, which could push overall figures even higher.

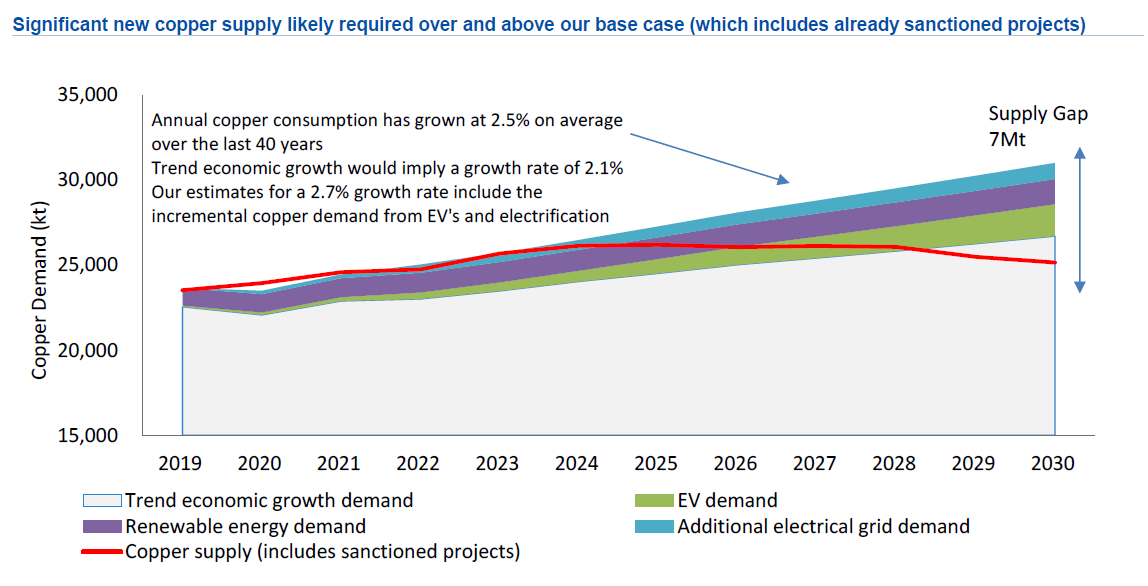

It is estimated that copper consumption, including its relation to electrification and electric vehicles trends, will grow at a 2.7% CAGR, surpassing pure economic development (2.1% annually), and it doesn't seem straightforward for supply to match this pace. During the last cycle of high prices (2017-2018), the industry responded by launching several projects (QB2, Quellaveco, etc.), but these were the more advanced and easier to implement ones. From 2025 onwards, there is little visibility on new mines. At the same time, copper mining is becoming increasingly challenging: cost inflation, worsening ore grades, social discontent, and a lack of quality projects are putting pressure on extraction operations.

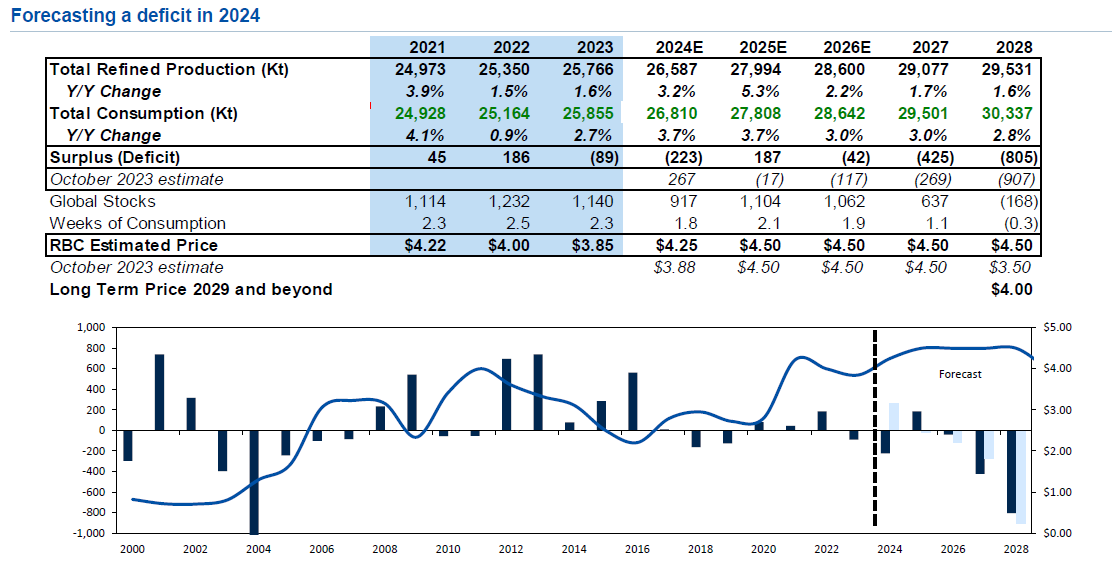

Entering into the current supply and demand balance, expectations for 2024 were pointing to a surplus of 2%. However, due to persistent supply issues (such as the closure of Cobre Panamá, reduction of guidance by several operators, etc.), the consensus now indicates a deficit of 1% for this year.

Current prices, after a sharp increase at the beginning of 2024 that took us above $5/lb, are not sufficient to massively incentivize new exploration and development. Combined with existing macroeconomic uncertainties, this is likely to further delay new project developments, exacerbating the future supply deficit, which is also worsened by the deterioration of current mining operations. Over the next 10 years, the necessary investment to balance the market—currently facing a projected 10Mt deficit—exceeds $200 billion, not accounting for potential cost increases and inflationary pressures.

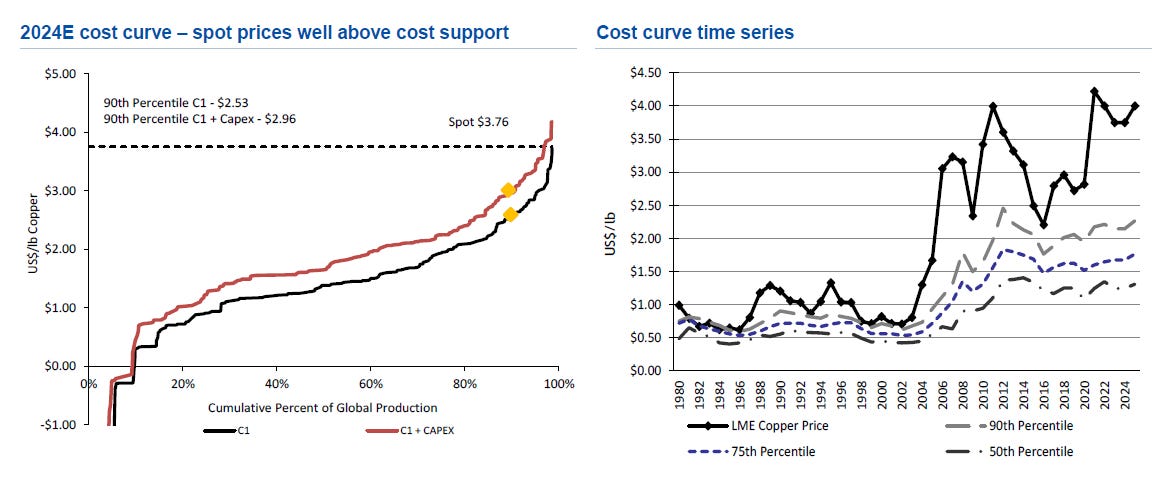

If we analyze the industry's cost curve, a key factor in commodity investment, and its evolution over time, we can see that the 90th percentile was already above $4/lb last year (for 2025, an additional ~$0.1/lb–$0.2/lb should be considered). This suggests that $4/lb is the minimum threshold required to incentivize new developments with a decent return (+20% IRR). Most likely, this figure will continue to rise over time, which is why, in the valuation model for Amerigo, I will use $4.5/lb as a reference price going forward.

Governments continue to maintain a constructive rhetoric regarding the development of new projects, but with increasing emphasis on environmental policies, obtaining permits and social approval for these projects is becoming increasingly difficult.

From a momentum perspective, inventories are at historically high levels. A year ago, they covered less than five days of demand, which has historically led to significant price rallies to incentivize new supply. However, the situation reversed starting in May, particularly in China, and there is now a long way to go to return to price-supportive levels.

Investment thesis

Let's review the operational, financial, and balance sheet aspects of the company in order to make an assessment and draw conclusions about the company. Specifically, we will analyze the following points, on which the investment thesis is based:

Operations

Cash generation

Balance sheet

Capital structure

Shareholder return

Keep reading with a 7-day free trial

Subscribe to LWS Financial Research to keep reading this post and get 7 days of free access to the full post archives.