Disclaimer

LWS Financial Research is NOT a financial advisory service, nor is its author qualified to offer such services.

All content on this website and publications, as well as all communications from the author, are for educational and entertainment purposes only and under no circumstances, express or implied, should be considered financial, legal, or any other type of advice. Each individual should carry out their own analysis and make their own investment decisions.

Introduction and business model

Duratec Limited is an Australian contractor whose business involves providing assessment, maintenance, and repair services for both public and private infrastructure across various sectors. In line with this, their corporate mission is to become the largest civil contractor in the country. The main industries they serve include energy, mining, defense, facades and building, and maritime infrastructure.

Companies like Duratec, classified in the Engineering & Construction (E&C) sector, usually do not generate good long-term returns because they suffer from some structural and business model problems:

They operate in highly cyclical industries, with construction dominating the business over maintenance and rehabilitation, closely tied to the boom-and-bust economic cycle.

There is a risk of project concentration. E&C companies, especially in their early stages, often depend on one (or a few) major clients or projects, posing a significant risk to business viability if they lose the contract or if their client faces difficulties in their own business.

Execution risk. Contractors typically lack significant moats, and much of their competitive advantage is based on reputation and track record. Poor execution, especially due to negligence, malpractice, or incompetence, can cause irreparable damage leading to business collapse.

At first glance, this company may not seem to fit the profile of companies we typically follow in the LWS Financial Research universe. However, what has piqued my interest in this industry, leading me to the idea of $DUR, are the significant tailwinds in the sector and the particularities of the company that mitigate many of the risks described above.

The majority of the human population (80%) resides in developing countries striving to achieve Western living standards, which necessitates quality infrastructure. Consequently, we are witnessing a construction and development boom in these regions. Once developed, similar to OECD countries, these infrastructures require maintenance to ensure longevity and service, estimated at 5%-6% of their cost annually, guaranteeing a tailwind and recurring business for contractors performing these tasks. In Australia, this case is even more pronounced due to having aging infrastructure, with maintenance and renovation needs that are even greater.

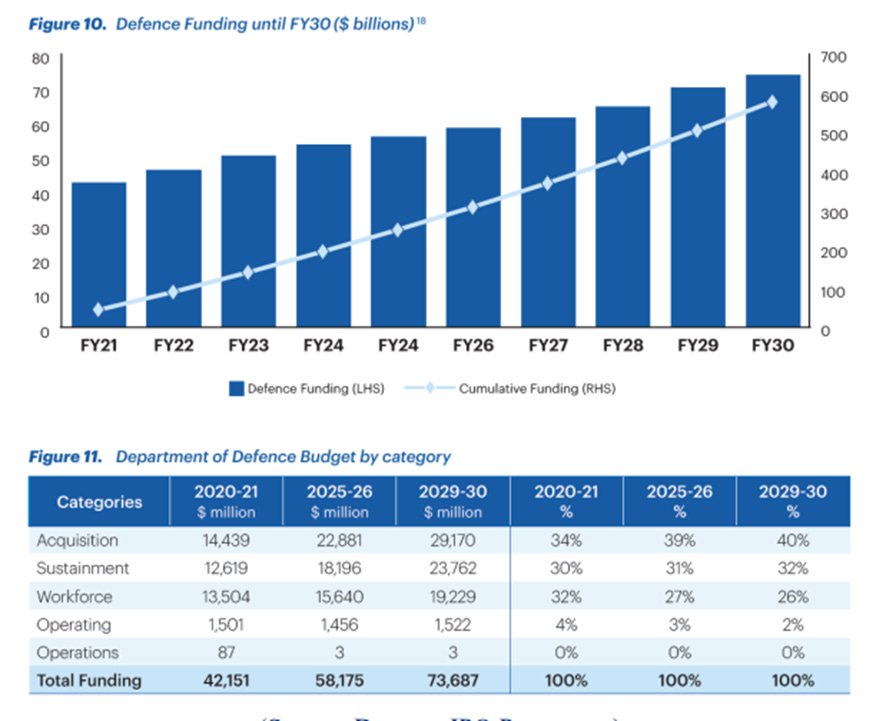

In addition to this structural trend, due to the current geopolitical situation, nations' defense spending is continuously and significantly increasing, with maintenance being a key component of this expenditure. In the specific case of Australia (lower image), the energy and mining sectors also hold significant economic relevance and require similar care and supervision.

Investment thesis

Once the structural tailwinds are understood, let's focus on the specific idea of Duratec, which has particularly interesting fundamentals, characteristics, and valuation. Specifically, we will analyze the following sections: