Georgia Capital

A compounder on the shores of the Black Sea

Disclaimer

kairoscap is NOT a financial advisory service, nor is its author qualified to offer such services.

All content on this website and publications, as well as all communications from the author, are for educational and entertainment purposes only and under no circumstances, express or implied, should be considered financial, legal, or any other type of advice. Each individual should carry out their own analysis and make their own investment decisions.

Introduction and business model

Georgia Capital (CGEO) is a business holding company with operations in the country of Georgia. Its main activity is to develop or acquire businesses without a specific time frame or mandate, but with the goal of monetizing them by selling its stake as these businesses mature. Their target investment universe includes large companies (with the potential to reach a valuation of at least $100 million within the next 5 years from their investment) and ideally with an asset-light business model.

They classify their businesses by size (large and in the investment phase) and also separate those that are publicly traded (Bank of Georgia and the water utility business) from the rest. In the previous matrix, we can see how they classify each of their business lines (which we will see in detail later) according to their main investment criteria.

In 2022, the Group introduced a new metric (Net Capital Commitment, NCC) to measure leverage and guide their future capital allocation decisions. Specifically, this metric is calculated as:

NCC = Net Cash (debt) - planned and committed investments

And the ratio of this leverage measure to the total asset value is used to address capital allocation through the following formula:

If NCC < 15%, they will aggressively pursue stock buybacks and new investments.

If NCC is between 15% and 40%, they will carry out tactical investments/buybacks while continuing to deleverage the balance sheet.

If NCC > 40%, they will prioritize balance sheet strengthening and will not commit more capital to shareholder returns or new investments.

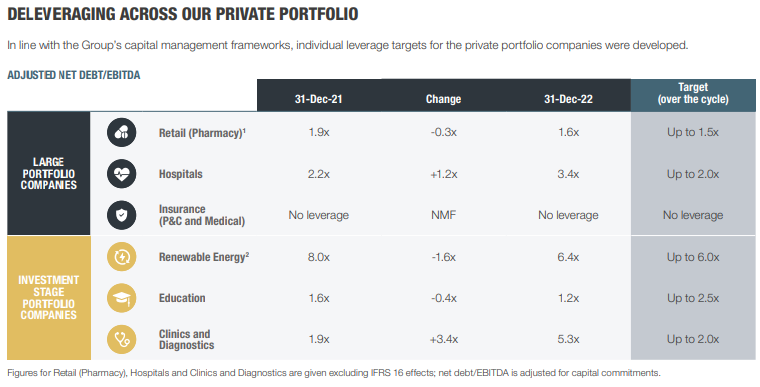

In addition to managing debt and leverage at the holding level, each of the companies has its own target debt ratios, with the goal of maximizing returns. In the following table, they show the evolution of net debt/EBITDA for the main business lines as well as the long-term target (in some cases, for expanding businesses, there is a short-term deviation that they expect to correct later).

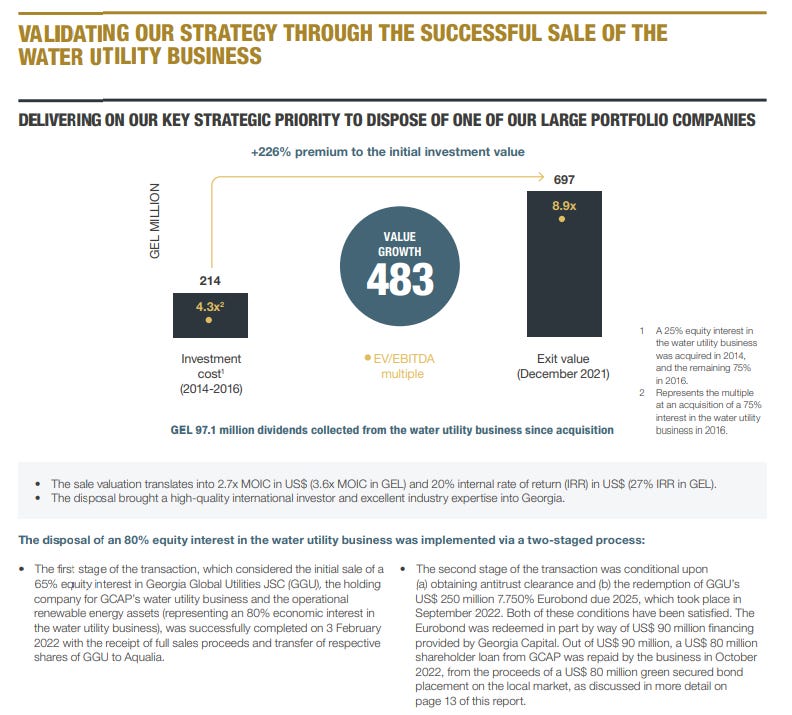

Their strategy of selecting businesses, developing them, and subsequently exiting them has been validated through two methods: the increasing dividends they receive from their investments and the sale, last year, of the Water Utility business (they retain options for 20% of it), in which they multiplied the initial capital invested by 2.7x in 6 years, with an associated IRR of 27% in local currency (20% in USD). CGEO still holds a 20% stake in this business, which they can exercise through options in 2025-2026; specifically, CGEO has a put option at 8.25x EV/EBITDA for 2026, and Aqualia (the buying company) has a call option at 8.9x, based on the normalized EBITDA of the company at that time.

For this thesis, it is also very relevant to understand the geographic, economic, and political environment in which the company operates, as opportunities for buying, growing, and selling largely depend on it. Georgia has a population of 3.7 million, a fairly balanced demographic pyramid, and a clear pro-European policy. The influence and relationship with Russia remain significant (it is a former Soviet republic) and not always friendly: in 2008, Russia invaded part of Georgia under the pretext of defending one of its regions, South Ossetia, which they ultimately annexed.

The country's economy grew at a double-digit rate for the second consecutive year in 2022 (+10.1%), ending the year as one of the top 10 fastest-growing countries globally, according to the IMF. Additionally, one of its main economic drivers, tourism, recorded a 108% increase in revenue compared to 2019, completing the post-pandemic recovery. The unemployment rate dropped to 17.3%, the lowest level since 2010, although there is still room for improvement: more than 66,000 jobs were created in 2022.

The budget deficit for the year is estimated at 3.1% of GDP, and the local currency (the Georgian Lari, GEL) has continued to appreciate against the dollar (+19.6% in 2022), driven by strong foreign inflows and the recovery of tourism in the country. Inflation seems to be under control, having decreased to 0.3%, although in developing countries, price movements (both up and down) are much faster and more aggressive, and monetary policy is already restrictive. Public debt is very low relative to GDP (39.7%), especially considering the strong economic growth, and with inflation under control, the expected interest rate reduction should contribute to this trend.

Therefore, we can see that this is a region in the midst of development with many tailwinds to offer for a private equity company like Georgia Capital.

Investment thesis

We are going to review, one by one, all of Georgia Capital's businesses, as well as discuss their valuation and prospects. Additionally, we will also review the holding structure: balance sheet, capital allocation, to form a complete picture of the company.

Keep reading with a 7-day free trial

Subscribe to LWS Financial Research to keep reading this post and get 7 days of free access to the full post archives.