Disclaimer

LWS Financial Research is NOT a financial advisory service, nor is its author qualified to offer such services.

All content on this website and publications, as well as all communications from the author, are for educational and entertainment purposes only and under no circumstances, express or implied, should be considered financial, legal, or any other type of advice. Each individual should carry out their own analysis and make their own investment decisions.

Introduction and business model

Golar LNG is the leading independent player in the FLNG market, a highly specialized segment within the global natural gas midstream. The company operates a fully integrated industrial model that spans the engineering, conversion, operation, and maintenance of floating liquefaction units (FLNG), capable of processing natural gas at the point of extraction and exporting it as LNG without the need for onshore infrastructure. This approach creates an operating profile with predictable cash flows, high technical availability, and exceptional resilience to geopolitical risk. Golar’s differentiated positioning relative to other competitors in the segment (both FLNG and onshore infrastructure) is based on three key elements:

A superior operating track record, demonstrated by the flawless performance of Hilli, its first asset, since 2018;

A contract portfolio with durations exceeding two decades and highly creditworthy counterparties;

A model that allows the replication of new FLNG units without incurring the complexity and cost overruns that typically affect onshore projects.

The company is at a strategic inflection point. With Hilli in operation (one of its assets, which will be discussed in more detail in the next section), Gimi starting production, and Fuji under construction, Golar is consolidating a platform whose EBITDA is expected to grow from approximately USD 250 million to nearly USD 1 billion by 2030.

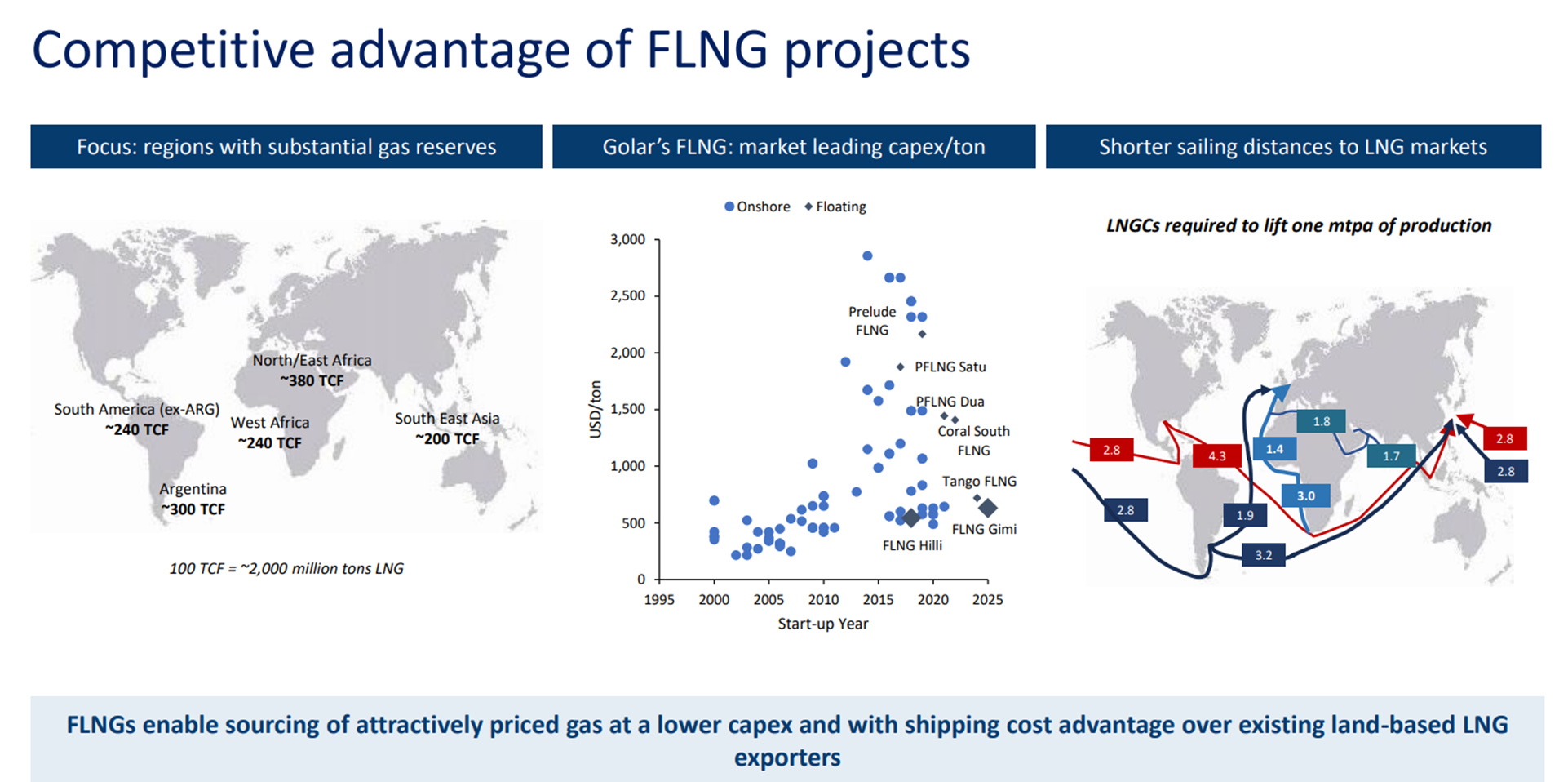

At the macro level, natural gas is one of the commodities with the strongest demand outlook for the coming decades. It serves as a bridging energy source in the energy transition and provides flexibility to meet short-term demand peaks driven by structural factors such as global economic growth, as well as cyclical factors like the rise of AI. Supply and demand centers are geographically separated, making the export of large volumes of natural gas necessary, with LNG being the most efficient form. An FLNG unit costs roughly one-third of an onshore plant, enters operation 3–4 years earlier, and allows the capture of arbitrage opportunities without a fixed location. Golar is the leader in this modular architecture.

Over the past decade, Golar has executed a structural transformation that has fundamentally altered its business model, risk profile, cash generation capacity, and valuation as a listed asset. The company divested its LNG carrier fleet—sold to CoolCo in 2022—its FSRUs, and its downstream business, which was transferred to New Fortress Energy. This sequential divestment process has enabled debt reduction, corporate simplification, and the reallocation of resources toward the highest-return and most scalable business: FLNG.

The result is a pure-play FLNG company with a clear growth strategy supported by multi-decade contracts, high-quality clients—BP, Perenco, Pampa, Harbour Energy—and projects aligned with globally relevant gas hubs such as GTA (West Africa) and Vaca Muerta (Argentina). This transformation has dramatically reduced operational complexity and increased financial visibility. The market, however, continues to value Golar as a cyclical asset dependent on Argentina and commodity prices, rather than recognizing that it operates a global, diversified contract portfolio with returns comparable to—or higher than—those of premium energy utilities. Compared with its main competitors (ENI, Petronas, Shell, Cedar LNG), Golar is the clear leader in FLNG capacity (8.6 mtpa across its three assets versus 6.4 mtpa for ENI, the second-largest operator), in an industry expected to grow significantly over the next five years, expanding from 17 mtpa of supply to an expected 30 mtpa. Each FLNG unit is typically contracted for 20 years, effectively turning the assets into quasi-utility instruments, with exceptionally stable margins and an unusual level of cash flow visibility even within the energy infrastructure sector.

Investment idea

To answer the question of whether Golar LNG could be a good investment opportunity, we will analyze the following sections:

Assets and business lines

Operations and financials

Balance sheet and shareholder return

Valuation

Let’s get started.