Peabody Energy Corporation

Peabody Energy Corporation

Beautiful clean coal

Disclaimer

LWS Financial Research is NOT a financial advisory service, nor is its author qualified to offer such services.

All content on this website and publications, as well as all communications from the author, are for educational and entertainment purposes only and under no circumstances, express or implied, should be considered financial, legal, or any other type of advice. Each individual should carry out their own analysis and make their own investment decisions.

Introduction and business model

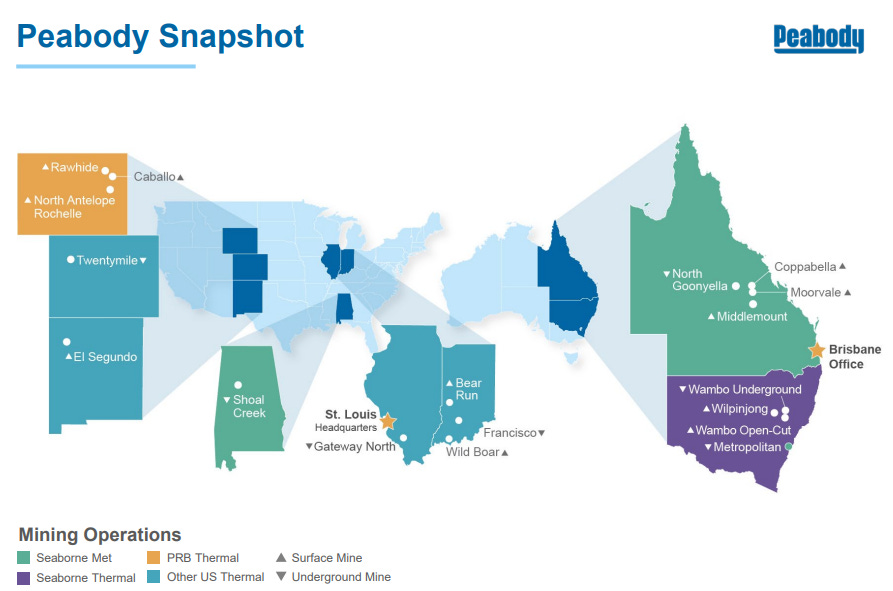

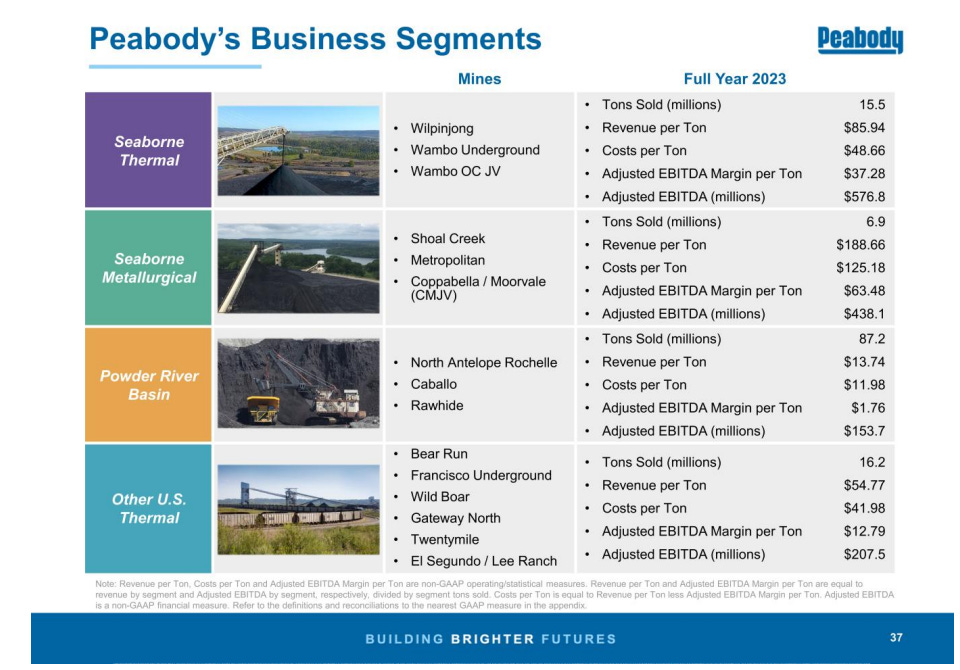

Peabody Energy is a producer of thermal and metallurgical coal in the United States and Australia, although nearly 70% of its revenue comes from the thermal segment. They operate mines in the following geographies, with the production distribution contained in the legend:

Coal is the first fossil fuel widely used in history, enabling the industrial revolution and thus being the energy source that has contributed most to human progress. However, its public image has recently changed: it has been demonized for its high relative emissions (although modern plants have a very small impact), and its disappearance is forecasted in the near future. Despite these exaggerated proclamations, we need coal: we need it for electricity generation, the operation of industrial complexes, and steel manufacturing. These uses are key to welfare and economic progress, and demand will continue to rise, especially in the metallurgical segment and/or in developing countries, until technological innovation finds a greener, cheaper, and more efficient solution to these processes. In 2022, following the rise in gas prices exacerbated by the conflict between Russia and Ukraine, coal regained much of the lost competitiveness for electricity generation against gas. For reference, price equivalences for thermal coal were:

USA: $6/mmbtu of gas = $114/Mt of coal (vs $150/Mt price in 2022)

Europe and Asia: $35/mmbtu of gas = $665/Mt of coal (vs $350/Mt at the peak of 2022).

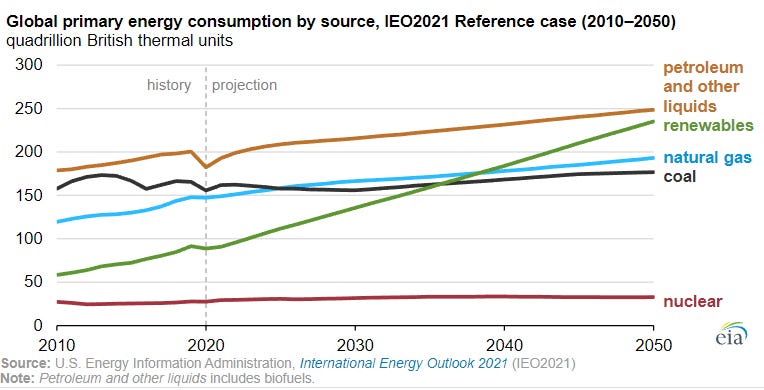

This dynamic led to gas-coal substitution for some processes, providing greater support to demand. In the most pessimistic forecasts (those of the IEA), contrary to the general opinion of imminent ruin, coal demand remains stable for the next 30 years:

Other consulting firms, such as Wood Mackenzie, confirm this view: they expect demand to remain flat until 2030 and then begin to decline slowly. However, it is better not to view demand as an aggregate, as there are significant geographic divergences: in developed economies, demand is already in a phase of slow decline, while in developing economies (many of which still use less energy-dense sources than coal, such as biomass), demand continues to increase, and at a very high rate; moreover, these areas also experience the highest population growth, making them more relevant. By 2030, it is expected that 85% of electricity generation capacity through coal will be in emerging economies. However, in 2023, due to the significant increase in shale productivity and the normalization of inventories in Europe and Asia thanks to the mild winter of 2022, the price of natural gas fell sharply, to the detriment of the competitiveness of thermal coal, leading to the closure of 14 GW of capacity in the USA (-41% accumulated since 2010).

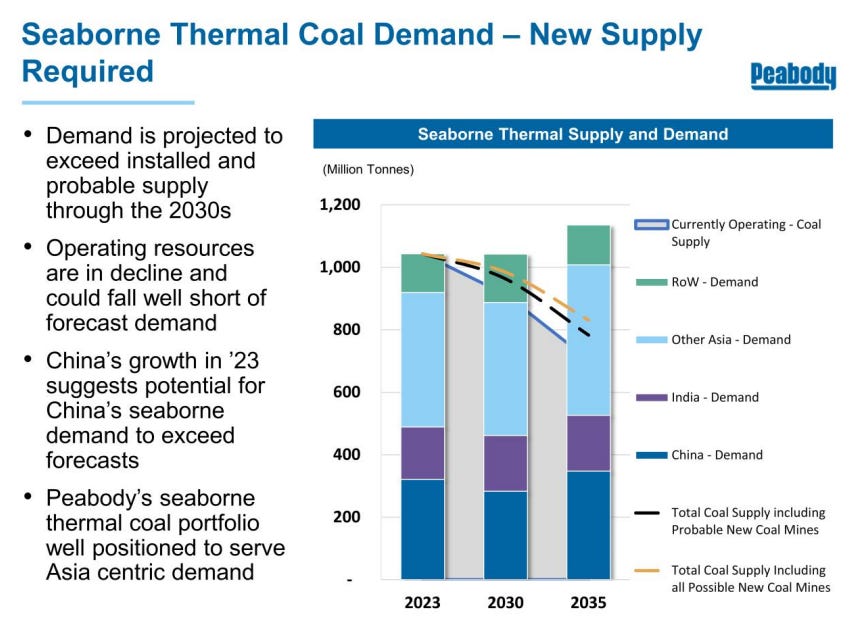

The current supply is unable to meet these demand forecasts, and there are significant obstacles to the exploration and construction of new mines, especially in Western jurisdictions (in the USA, for example, coal production remains historically low, greatly damaged by shale competition in recent years). Meanwhile, China acknowledges that coal is its most important energy source and is increasing production capacity.

Commodity companies tend to be poor investments because when the supply-demand balance is in deficit and prices rise, high returns attract new investment, which eventually offsets the balance in the other direction, causing a price decline and losses to the sector. Coal could be the exception to this cycle, as new supply faces strong entry barriers due to the difficulty of obtaining permits and financing, preventing the typical trajectory of the capital cycle, especially in the metallurgical segment.

Investment thesis

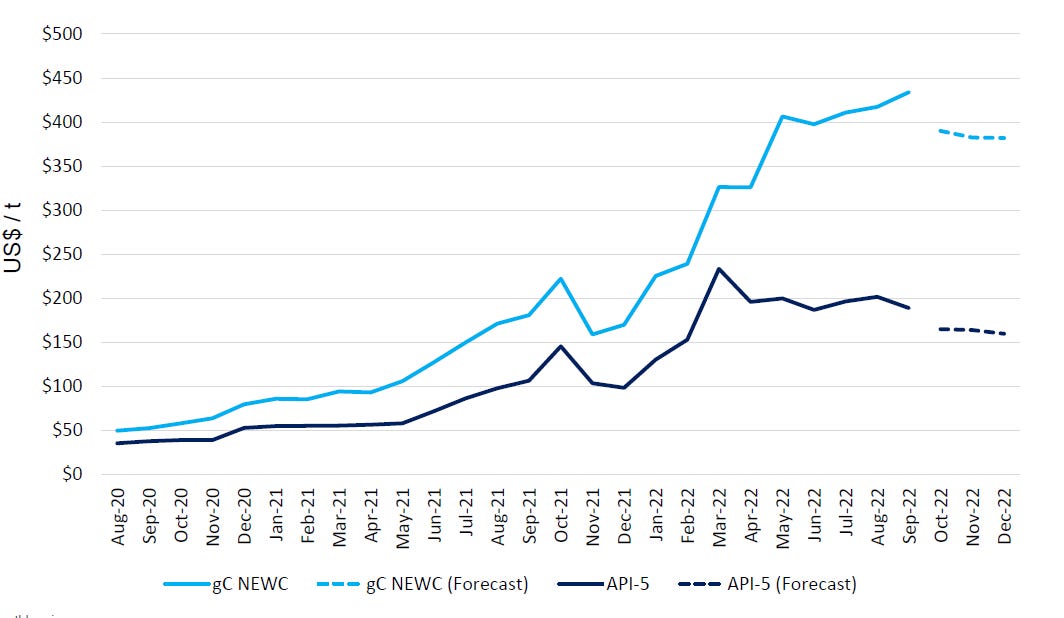

When we first published this idea at the end of 2022, thermal coal prices were at extraordinarily high levels (both historically and in relation to other energy alternatives such as gas and oil), and since then, they have fallen by nearly 60%, to around $140/ton, which raises the question of whether this investment idea still makes sense or not.

As we highlighted, prices have fallen significantly, especially in the thermal segment, so the financial projections we made have become obsolete, although the anticipated catalysts (start of the shareholder return program, margin reversal from derivatives...) have materialized.

Let's now look at the pillars of this investment idea and the expected valuation and return. The main points for this thesis are:

Keep reading with a 7-day free trial

Subscribe to LWS Financial Research to keep reading this post and get 7 days of free access to the full post archives.