Petrobras: my vision

Petrobras: my vision

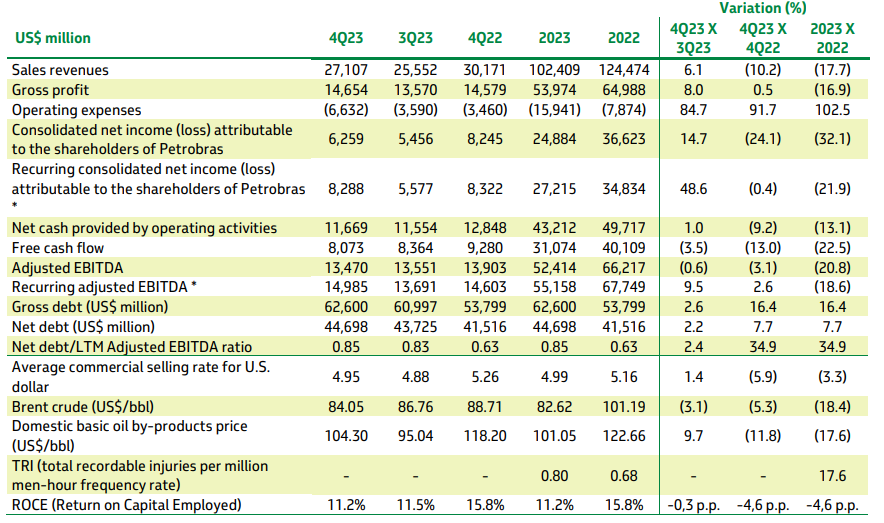

Q4 results commentary

Disclaimer

LWS Financial Research is NOT a financial advisory service, nor is its author qualified to offer such services.

All content on this website and publications, as well as all communications from the author, are for educational and entertainment purposes only and under no circumstances, express or implied, should be considered financial, legal, or any other type of advice. Each individual should carry out their own analysis and make their own investment decisions.

Political risk: fears and expectations

Petrobras presented its fourth-quarter 2023 results on Thursday after the market close, and it was immediately evident that something was amiss: in after-hours trading, the shares plummeted by 15%, making the market's opinion on the report clear.

Given the severity of the movement, the immediate reaction is to think that the numbers are a disaster. However, taking a look at the report, the reality is quite the opposite: they generated $8 billion in FCF (8.4% quarterly yield) in the quarter and $31 billion in the year (33%), marking the second-best year in their history after 2022. The negative comparison to 2022 is explained by the 18% drop in crude oil prices, partially offset by higher production volumes. Debt has remained controlled within the company's target range despite the significant 2023 CAPEX campaign (+$8.7 billion in new leasings), and returning $20.4 billion to shareholders through buybacks and dividends.

If it's not the results themselves, surely they must have had some operational issue, a massive impairment, or canceled shareholder remuneration, finally proving that investment banks and analysts were right: the political risk was too great. Not at all. Production increased by 3.7% in the year, reaching 2.78Mb/d, truly remarkable, and production costs decreased from $40/b to $35/b, with many of the new fields even showing figures below $25/b. The reserves replacement ratio was 168%, meaning the company replaced the 900 million barrels produced and added an extra 400 million to its reserves.

Petrobras's results are even more impressive, if possible, when compared to other majors, where it stands on the podium in all financial and operational metrics despite having a much smaller size (in market capitalization) than its peers.

And, of course, it remains by far the cheapest (in the current price environment, moreover, the actual FCF multiple is closer to 3.5x-4x than 5.2x).

But then, what has happened?

Mi vision

Next, we are going to see why the market reacted so negatively to these results, which at first glance seemed correct, and what my perspective on them is.

Keep reading with a 7-day free trial

Subscribe to LWS Financial Research to keep reading this post and get 7 days of free access to the full post archives.