Q125 Earnings review, part III

New year, part III

Disclaimer

LWS Financial Reserach is NOT a financial advisory service, nor is its author qualified to offer such services.

All content on this website and publications, as well as all communications from the author, are for educational and entertainment purposes only and under no circumstances, express or implied, should be considered financial, legal, or any other type of advice. Each individual should carry out their own analysis and make their own investment decisions.

Q125 Earnings review, part III

This delivery is the third (and final) installment of the first-quarter earnings commentary for 2025 for the companies under our watch or model portfolio. These presentations tend to be highly positive events for our portfolio, as they showcase to the market the strong cash-generating capacity of our holdings and are often accompanied by generous shareholder returns. Specifically, in this publication, we will discuss the results of the following companies::

Coinbase

Warner Bros Discovery

Cresud S.A

Braskem

Let’s get at it.

Coinbase

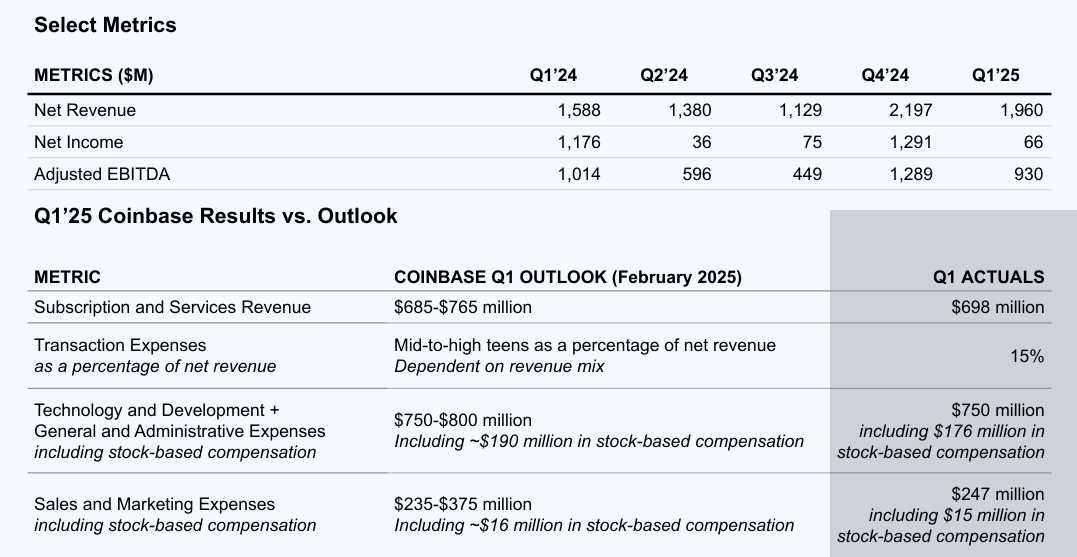

Coinbase has started 2025 with strong financial results, although this is not the core pillar of our investment thesis. Revenues reached $2 billion and adjusted EBITDA came in at $930 million in the first quarter (continuing a consistent positive trend), confirming that the business not only withstands the macro environment but is also expanding while others are retreating. Market share continues to grow in both spot and derivatives trading, with over $800 billion in global derivatives volume during the quarter—driven primarily by its international exchange, where its share in perpetual contracts surged by more than 60%. Overall, the company tends to provide accurate and honest guidance, which it has delivered on consistently.

But the truly significant development has been the announcement of the acquisition of Deribit, the world’s leading crypto options platform, with over $30 billion in open interest and $1 trillion traded outside the U.S. in the past year. With this move, Coinbase steps directly into the front line of the global crypto derivatives market, becoming a genuine one-stop shop for clients seeking to trade crypto assets, greatly easing adoption and use.

Coinbase is also advancing its offensive with USDC (stablecoins being the other pillar of adoption), which has reached a new all-time high market capitalization of $60 billion. Meanwhile, the average balance held in Coinbase products rose 49% quarter-over-quarter, reaching $12 billion. This growth is no accident: it's the result of a bold international licensing strategy. In recent months, Coinbase secured mass registration in Argentina and filed with India’s Financial Intelligence Unit. In Europe, for example, the approval of MiCA has cleared the path, effectively sidelining Tether from the playing field.

At the same time, especially since Trump’s return to the White House, the political landscape has become much more favorable. The U.S. has even taken a step that could mark a turning point: a recent executive order has established the creation of a strategic Bitcoin reserve and a national stockpile of digital assets. For the first time, the country formally recognizes Bitcoin as a strategic asset, opening the door for other governments to follow suit—though it remains to be seen how and to what extent this will be implemented.

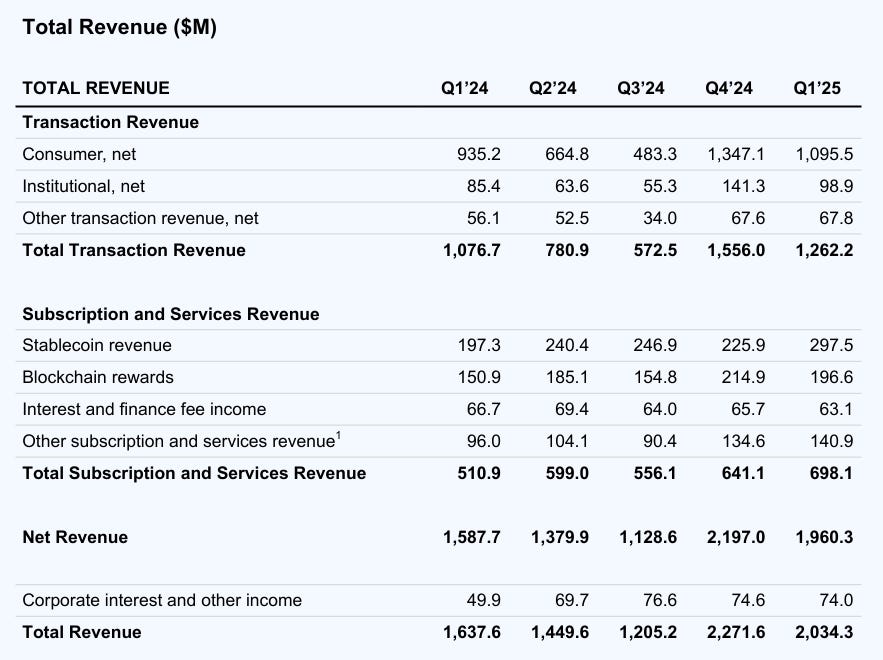

Financially, as mentioned, the company reported $930 million in adjusted EBITDA, $66 million in net income, and a new metric designed to isolate the impact of crypto asset volatility: adjusted net income, which came in at $527 million. One chart I always find useful to share and analyze is the one that shows the growing weight and upward trend of service revenues, which reduces the cyclicality of the income statement and makes it less dependent on volatility.

Looking ahead to Q2, the company anticipates a more challenging environment due to the sharp drop in crypto prices (excluding Bitcoin), such as Ethereum (-36%) and Solana (-25%), which directly impact staking and rewards income, as well as transaction volumes. The May recovery may offset a weak April, especially if BTC breaks new highs—a scenario I see as likely, if not in Q2, then almost certainly in Q3. However, macro uncertainty and trade tensions are not helping. In April alone, spot volume fell by 12% month-over-month—mirroring the global decline of 13%—and transaction revenues reached $240 million. Subscription and service revenues are expected to ease to between $600 million and $680 million, dragged down by asset price corrections.

Coinbase has not only strengthened its balance sheet but is deploying capital with surgical precision to position itself for the coming years. The $1 billion share repurchase authorization with no expiration remains active, but capital allocation is being handled opportunistically: money goes where value is greatest. The $2.9 billion Deribit acquisition, partially financed with $700 million in cash from the balance sheet, follows this logic exactly. Not issuing new shares in this context is equivalent to an implicit buyback, as it avoids dilution and secures a dominant asset in a strategic segment.

From a structural perspective, the company does not hide its ambition: to become the world’s leading financial services app over the next decade. Trading and payments are just the starting point. Coinbase already operates across retail clients, SMEs, institutions, and developers, but the broader goal is to ride the wave of disruption crypto is bringing to the traditional financial system. With more and more banks preparing to integrate crypto, Coinbase holds a clear lead: it already dominates in product, has the infrastructure, regulation is starting to clear its path, and it has the liquidity to make bold bets. Holding onto cash is not a sign of caution but a lever for executing acquisitions and expanding its reach when opportunities are truly worth it. The current environment—with corrected valuations, inefficient structures, and increasing regulatory clarity—might be one of those moments when smart capital makes all the difference. And Coinbase knows it.

Warner Bros Discovery

Keep reading with a 7-day free trial

Subscribe to LWS Financial Research to keep reading this post and get 7 days of free access to the full post archives.