Disclaimer

LWS Financial Reserach is NOT a financial advisory service, nor is its author qualified to offer such services.

All content on this website and publications, as well as all communications from the author, are for educational and entertainment purposes only and under no circumstances, express or implied, should be considered financial, legal, or any other type of advice. Each individual should carry out their own analysis and make their own investment decisions.

Q224 Earnings review, part II

With this dispatch, we continue with the commentary on the second quarter results for the year 2024 of the companies under our monitoring or model portfolio. These presentations are usually very positive events for our portfolio, as they demonstrate to the market the great cash generation capacity of our holdings and are often accompanied by generous shareholder returns. Specifically, in this publication, we will discuss the results of the following companies:

Vermilion Energy

Peabody Energy

Warrior Met Coal

Valaris

Let’s get at it.

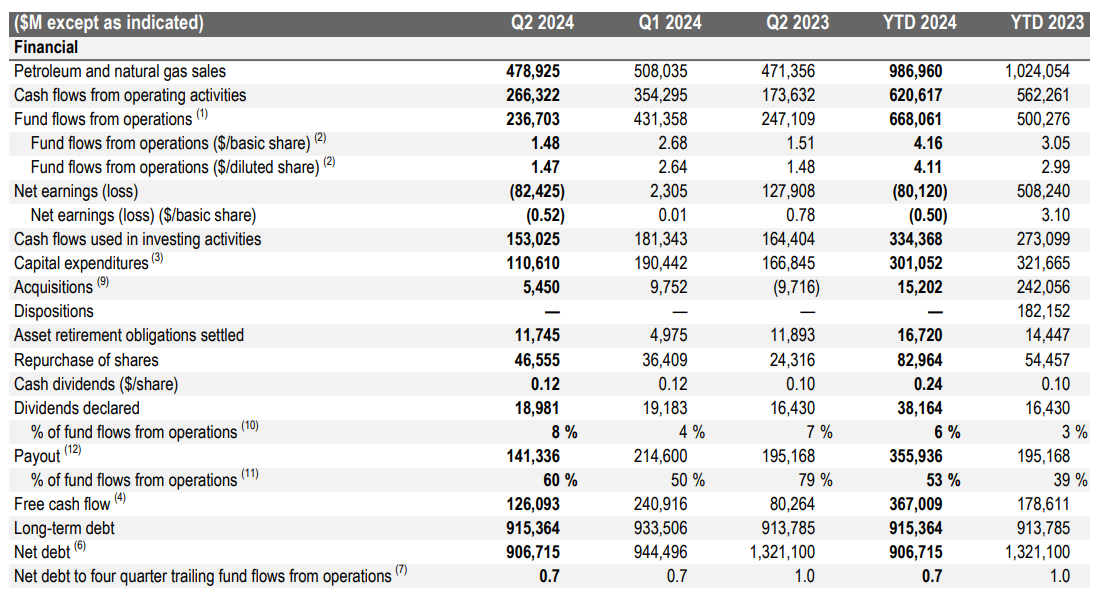

Vermilion Energy

Vermilion Energy closed another operationally excellent quarter, with production at the high end of guidance (85k boe/d), representing a +2% YoY increase (+6% YoY per share due to buybacks). Following these strong numbers, the company has decided to raise its full-year forecast to 83k boe/d - 86k boe/d (+1,000 boe/d at the lower end of the range compared to previous communications).

Cash generation for the quarter was $126M in FCF ($0.78/share), impacted, compared to the previous quarter, by lower gains relative to the hedges they have in place. Leverage continues to decrease, with net debt reduced by 4% during the quarter, while returning $66M to shareholders ($19M in dividends and $47M in buybacks). It’s important to note that, according to their current shareholder remuneration framework, they distribute 50% of their FCF in the form of buybacks and dividends, and this percentage will increase as leverage continues to decrease.

With the recent rebound in natural gas prices in Europe, now around $17/mmbtu, Vermilion has hedged 42% of their 2025 production at this level, ensuring a very attractive cash generation profile. The market is overly pessimistic about this company, which has not been the best in terms of execution in the past, but has managed to transform its balance sheet and finally start a substantial shareholder return program that can move the needle (they are buying back 1M shares per month).

Their assumptions regarding oil and gas prices are very much in line with the current strip, giving them significant optionality if these perform better (as I expect) and a realistic anchor if they do not.

Peabody Energy

Keep reading with a 7-day free trial

Subscribe to LWS Financial Research to keep reading this post and get 7 days of free access to the full post archives.