Q423 Earnings review, part I

Q423 Earnings review, part I

Trust the plan

Disclaimer

LWS Financial Reserach is NOT a financial advisory service, nor is its author qualified to offer such services.

All content on this website and publications, as well as all communications from the author, are for educational and entertainment purposes only and under no circumstances, express or implied, should be considered financial, legal, or any other type of advice. Each individual should carry out their own analysis and make their own investment decisions.

Q423 Earnings review, part I

We begin the final round of 2023 results presentations, which combine Q4 and the overall yearly figures. These presentations typically serve as very positive events for our portfolio, showcasing the market the significant cash-generating capacity of our companies, and moreover, they often come with generous returns to the shareholder. Specifically, in this publication, we will discuss the results of the following companies::

International Petroleum Corp

DHT Holdings

British American Tobacco

Peabody Energy

Here we go.

International Petroleum Corp

In November, when OPEC+ lost market control, we sold almost all our oil companies, keeping only those that represent a special situation or whose valuation and operations make them immune to the crisis, such as Petrobras. In this context, one of the companies we sold was International Petroleum, where we practically tripled our capital since 2021. Despite no longer being in our portfolio, it seems to me that, due to the quality of its management and assets, it is one of the few that allows for a long-term approach or buy and hold in a cyclical industry like oil.

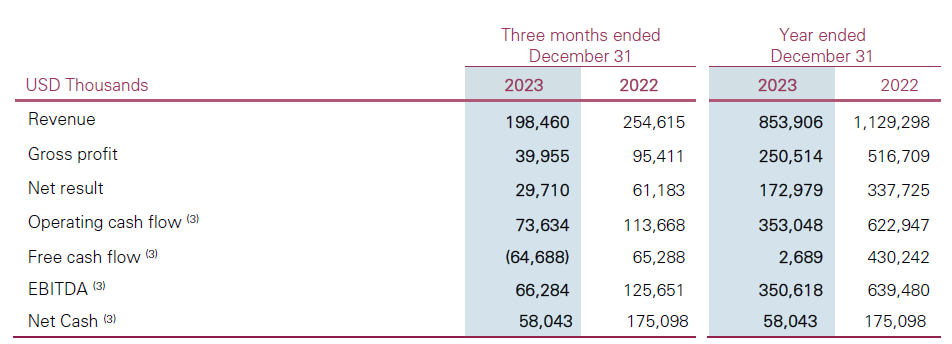

Thanks to excellent operational management and the acquisition of Cor4 in March 2023, they achieved a record production level of 51k boe/d, well above what was expected at the beginning of the year. Despite the significant drop in oil prices compared to 2022, their financial results have been very good:

Operating cash flow of $353M.

Free cash flow, in a year of massive CAPEX, of $3M.

Net cash position, at year-end, of $58M.

The figure for free cash flow is heavily influenced by the record investment of $327M ($240M for the development of Blackrod and $60M for the acquisition of Cor4). However, it is noteworthy that they have managed to keep it positive and finance all their projects organically. In addition to all the funds allocated for growth, they have carried out buybacks totaling $95M (8% of the float), completing the virtuous circle.

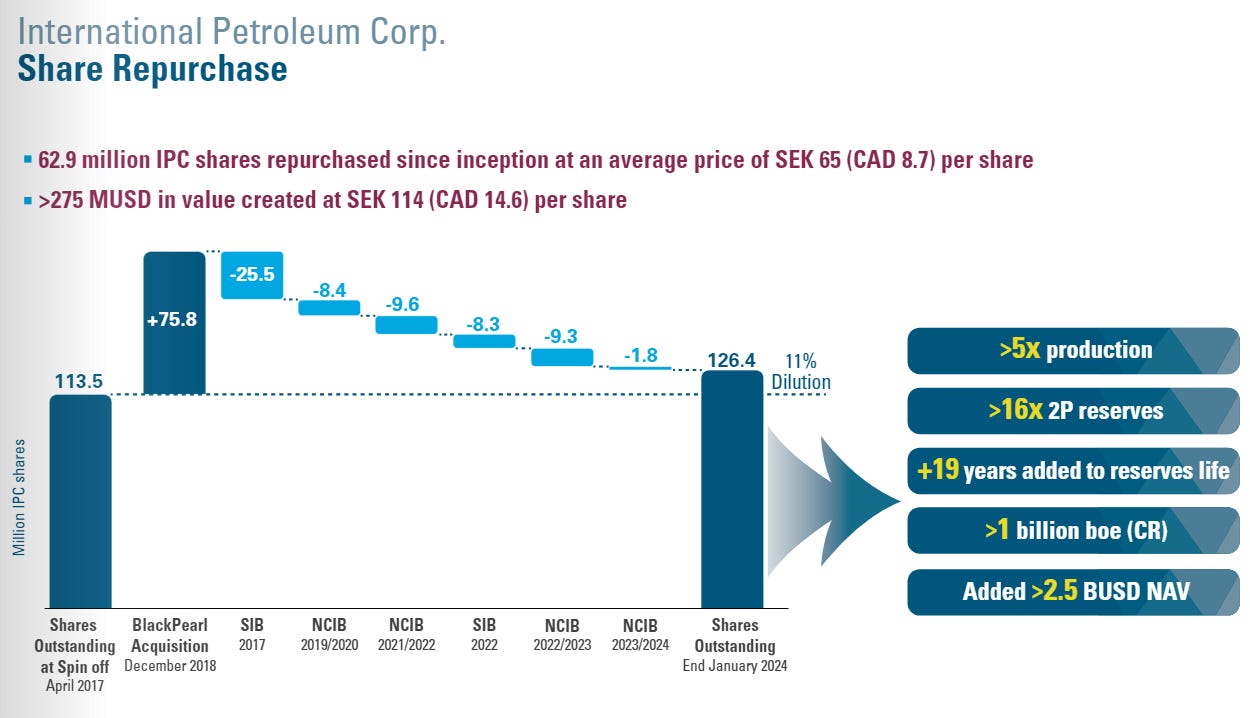

Since 2019, they have repurchased 23% of outstanding shares while expanding production and opportunistically acquiring other assets. One of the reasons why IPCO seems to me one of the few long-term options to consider in the oil & gas sector is the deep understanding and sensible use of capital structure by its management (the Lundins, in fact, have an impressive track record of value creation): since its foundation in 2017, IPCO has diluted shareholders by 11%, achieving a 5x increase in production, 16x in reserves, and adding 20 years of operational life, in what has been an exercise in value creation for the major shareholder.

In addition to NCIBs (normal course issuer bids), which are standard repurchase programs in Canada allowing the withdrawal of up to 10% of the float annually, they are considering conducting an SIB (substantial issuer bid), which are larger tender offers to accelerate the process. They have done this in the past, though not at the moment, as the priority is to finance the development of Phase I of Blackrod.

Another aspect where the management's excellent operational skills stand out is in the hedging they establish: for 2023, they were able to enjoy much higher natural gas sales prices than the spot market (average selling price of $4/mmbtu vs $2/mmbtu at market) thanks to pre-selling volumes established at the beginning of the year. Generally, in order to provide predictability and security to their cash flows to address their projects, they hedge part of their production, forex exposure, and WCS differentials each year. Specifically, for 2024:

25% of their oil production in Canada sold at $81/b WTI.

WTI/WCS differential covered at -$15/b for 70% of their Canadian production.

Currency hedged for Blackrod's CAPEX: $406M in 2024 and $150M in 2025.

This is especially important in a year with such a high forecast for CAPEX, as it allows them to face it with confidence and security while maintaining flexibility.

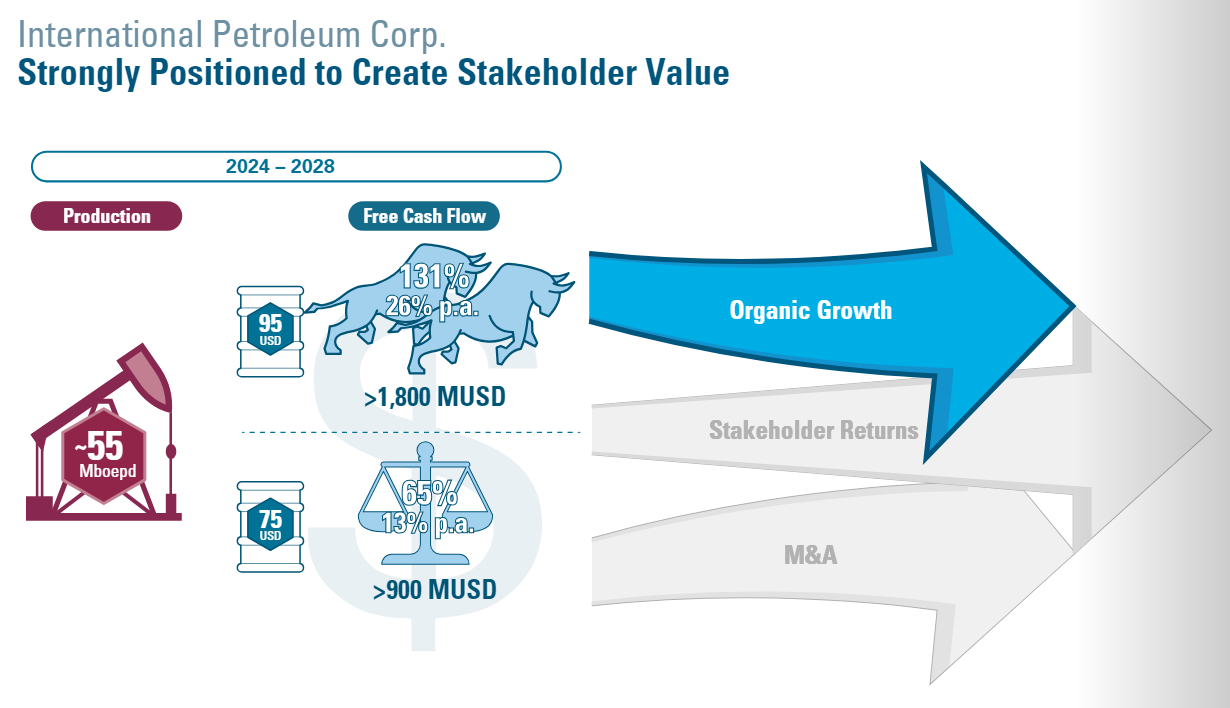

For 2024, they anticipate a production range slightly lower than that of 2023, between 46k boe/d-48k boe/d, and an even higher CAPEX investment: $437M, the bulk of which will go towards the development of Blackrod, with its first production expected in 2026 and enabling an increase in production beyond 65k boe/d. Excluding this concept, for 2024, within the price range of $70/b-$90/b WTI, free cash flow would be $140M-$270M, representing between 10% and 20% FCF yield. We can observe their significant operational leverage to oil prices, as seen last year with $420M of FCF with just an extra $20/b in crude oil prices. If we extend our time horizon a bit, over the next 5 years, including the capital invested in Blackrod, the company would generate (at scenarios of $70/b-$90/b) between $900M and $1.8B in FCF. This, considering the capital allocation priorities they clearly share with us, is poised to generate substantial value for shareholders.

DHT Holdings

DHT Holdings, the focus of our latest analysis, presented figures very much in line with expectations, with few surprises (as it often does) and great clarity and skill in management. Throughout 2023, it generated a net profit of $161.4M ($0.99 per share), which it distributed in the form of dividends (9% yield at current prices), maintaining the lowest debt profile in the sector, with an LTV of 19.7%, equivalent to a debt of $14.7M per vessel.

Keep reading with a 7-day free trial

Subscribe to LWS Financial Research to keep reading this post and get 7 days of free access to the full post archives.