Q424 Earnings review, part II

Part II

Disclaimer

LWS Financial Reserach is NOT a financial advisory service, nor is its author qualified to offer such services.

All content on this website and publications, as well as all communications from the author, are for educational and entertainment purposes only and under no circumstances, express or implied, should be considered financial, legal, or any other type of advice. Each individual should carry out their own analysis and make their own investment decisions.

Q424 Earnings review, part II

This delivery is the second installment of the fourth-quarter earnings commentary for 2024 for the companies under our watch or model portfolio. These presentations tend to be highly positive events for our portfolio, as they showcase to the market the strong cash-generating capacity of our holdings and are often accompanied by generous shareholder returns. Specifically, in this publication, we will discuss the results of the following companies::

CVR Partners

Valaris

Whitehaven Coal

Amerigo Resources

Let’s get at it.

CVR Partners

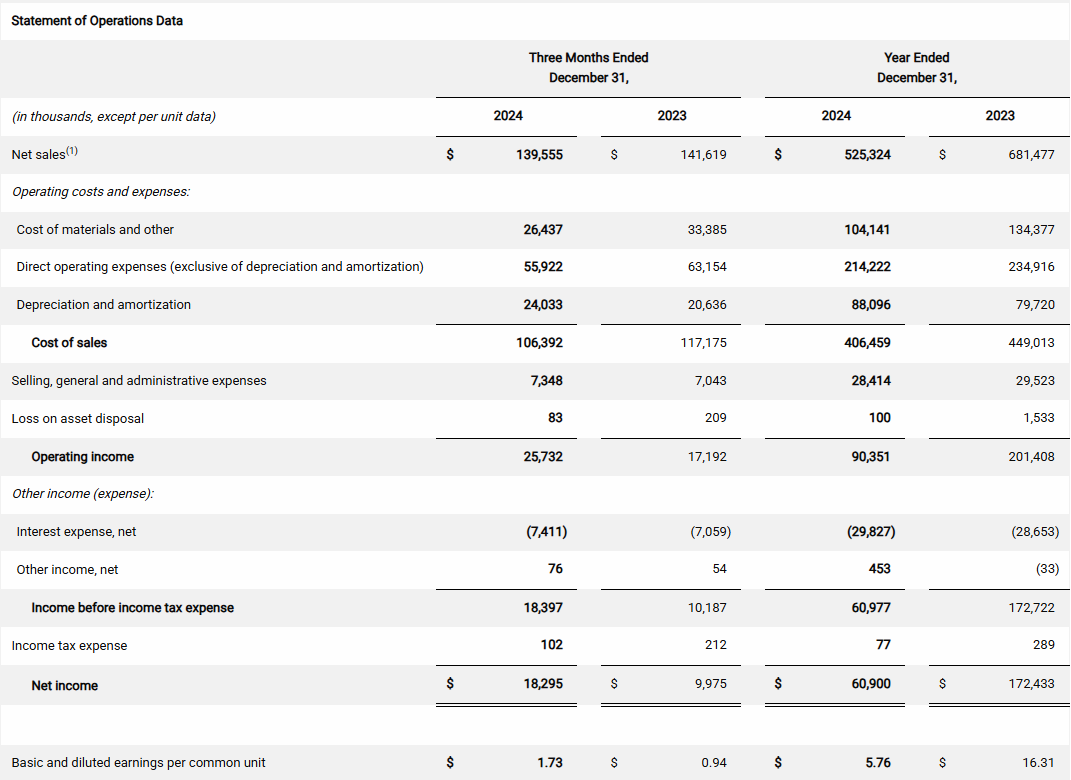

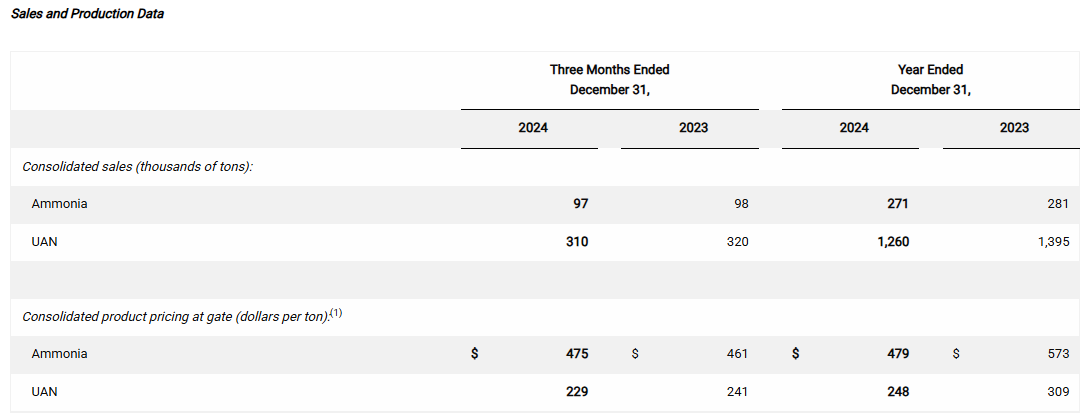

The results were very much in line with those of the previous quarter, and we won’t see a substantial change until 2026. The company closed Q4 2024 with net sales of $140M, a net profit of $18M, and an EBITDA of $50M (depreciation is a significant component of its financial statements). Plant utilization, following last year’s turnaround, has remained very high, above 96%, and, as we will see later, it should improve even further in the coming years. Compared to Q4 2023, ammonia sales volumes remained stable, while UAN volumes decreased by 3%, impacted by adverse weather conditions during the fall application season. They have decided to approve a $1.75/s distribution, bringing the total for the year to $6.76/s (8.45% yield), while reserving cash for the high CAPEX planned for 2025.

Regarding market conditions, ammonia prices increased by approximately 3%, while UAN prices fell by 5% compared to the same period last year. However, it seems we have clearly moved past the cycle’s low point. Despite adverse weather conditions, demand for nitrogen fertilizers remains strong, pushing prices higher compared to Q3.

2025 will be a year of significant investment, with maintenance CapEx of $35M-$45M and growth CapEx of $20M-$25M, which will be financed with the cash reserves accumulated over the last two years (at the end of the quarter, liquidity stood at $130M, of which $91M was pure cash). At the Coffeyville plant, engineering studies on the feasibility of using natural gas as an alternative to third-party petroleum coke as a raw material have already been completed. They are now developing construction plans and awaiting Board approval to begin execution.

Although the imbalances caused by the start of the Ukraine war and the associated disruption fears are now long forgotten, rising grain prices support increased demand for nitrogen fertilizers for spring application.

And customers are looking for more than what is available, which has driven the market higher over the past six weeks. Customers want to buy more. What I heard on the call is that it is very difficult to find available cargo for March. At this point, the market is more focused on April across all producers. This indicates that the market is tight and firm, and we will work hard to meet customer needs in April and May.

— Mark Pytosh

Not a bad starting point for the new year.

Valaris

Looking solely at the numbers, which have been solid and known for the past three months, it’s hard to understand the price trajectory Valaris has followed. Adjusted EBITDA for the fourth quarter came in at $142 million, a slight decrease from $150 million in the third quarter. Revenue was at the upper end of guidance, but EBITDA was slightly below expectations due to higher drilling contract expenses, mainly driven by a non-cash provision related to a legal matter.

Keep reading with a 7-day free trial

Subscribe to LWS Financial Research to keep reading this post and get 7 days of free access to the full post archives.