Disclaimer

LWS Financial Research is NOT a financial advisory service, nor is its author qualified to offer such services.

All content on this website and publications, as well as all communications from the author, are for educational and entertainment purposes only and under no circumstances, express or implied, should be considered financial, legal, or any other type of advice. Each individual should carry out their own analysis and make their own investment decisions.

New content

This week has been packed with updates at LWS Financial Research:

Weekly macro summary

There have been quite a few interesting events to analyze this week, and below I list the most noteworthy news. Let's get started:

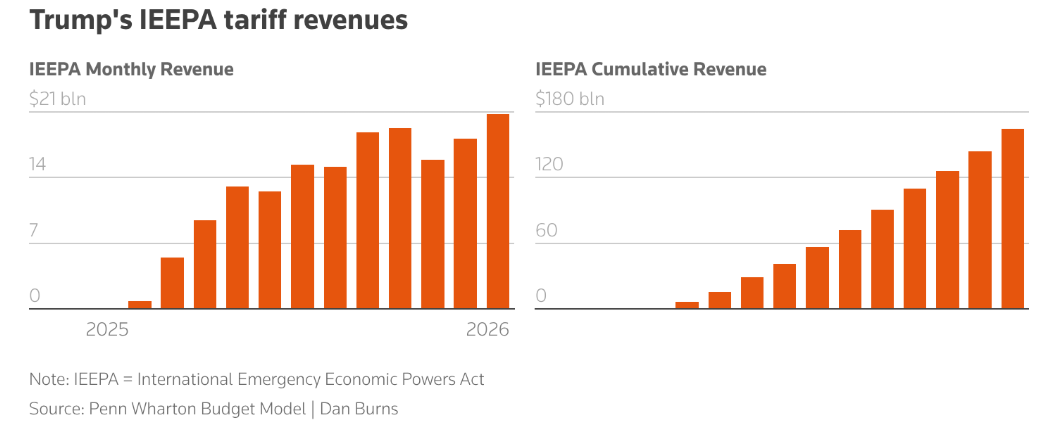

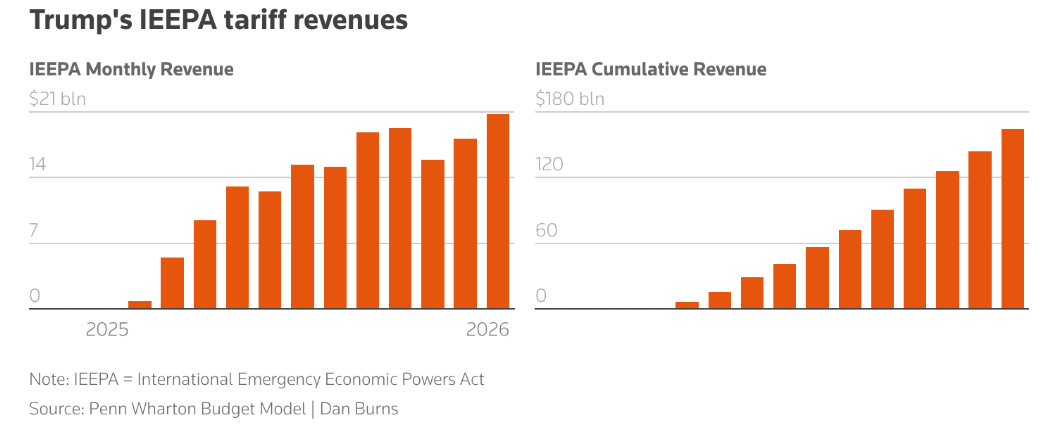

Wall Street closed higher last Friday, driven by the Supreme Court’s decision on tariffs, not so much because the outlook is good, but because it is less bad than the market had feared. The Court struck down Trump’s global tariffs by a 6–3 vote (they had been approved last year under a “national emergencies” law), and that immediately removed one layer of legal uncertainty that had been weighing on risk pricing for weeks. Trump, as if he were the leader of a banana republic, called the ruling a “disgrace” and announced a replacement: a 10% global tariff for 150 days under Section 122 of the Trade Act of 1974. But the calm did not last long: the very next day there was talk of raising it to 15%, which confirms the pattern of this Administration. Tariffs are no longer just trade policy; they are a tactical lever, a form of political communication, and above all a flexible tool for reintroducing pressure whenever convenient.

At the same time, a potentially explosive front is opening up: refunds. With thousands of lawsuits underway against the tariffs, some economists estimate that more than $175 billion in collected revenue may have to be returned. That is not a minor accounting detail; it is a fiscal and operational risk, and also a sign of how far the institutional framework has been stretched by “creative” measures that are now being put through judicial scrutiny.

The problems for the administration are piling up, and its chances of winning the midterms are already very remote. Macro data pointed to a slowdown in growth in the fourth quarter and a rebound in inflation in December. That mix is uncomfortable because it leaves the Fed in a grey zone, debating whether to cut rates to support activity while inflation is reminding everyone that it is not yet domesticated. The market is now almost at a coin toss on a June rate cut, just above the 50% mark. Europe, for its part, reacted more harshly than usual. The European Commission reiterated something basic in international trade: a deal is a deal. The problem is that it is not clear whether the new tariff scheme overrides the EU-US agreement reached last year, which set a 15% rate for most European goods and included zero-tariff exemptions for some products. If the framework changes, the exemptions disappear, predictability breaks down, and Europe’s relative advantage also vanishes if 15% ends up becoming the rate for everyone.

What is interesting about the episode is not Citrini’s post about artificial intelligence (and its impact) itself, but what it reveals about the market. When a blog post, amplified by social media, becomes a sufficient catalyst to move a broad set of sectors, and is even cited by Fed governors, the underlying reading is uncomfortable: we are in an expensive market, with sensitive positioning, looking for excuses to correct. Sometimes the market falls for reasons that are hard to isolate, and the narrative is built afterward. It also tells us something about the paradigm shift brought by the democratization of publishing platforms, where Substack now carries more weight than traditional journalism.

The argument that goes viral is an extreme, and very recognizable, version of the classic fear of automation. In that script, AI destroys jobs and income without generating substitutes, demand collapses, unemployment surges, and the economy enters a negative spiral. Meanwhile, AI infrastructure keeps shining, with Nvidia, TSM, and the hyperscalers maintaining capex and results as if the broader environment did not matter. It is an attractive narrative because it connects with an almost literary intuition: technology devouring its own market. And it offers a simple framework to justify selling in software, asset management, or banking, sectors that live on intermediation and trust. There are already quite a few examples of sectors collapsing in recent weeks in response to a new Claude plug-in.

But when one tries to reconcile it with basic macroeconomics, it starts to creak. The idea of “Ghost GDP,” output that shows up in the national accounts but does not circulate through the real economy, sounds more like metaphor than accounting. If GDP rises, then by accounting identity something has to rise on the other side: consumption, investment, government spending, or net exports. In Citrini’s scenario, consumption falls sharply. Government spending cannot be the release valve without a tax base or credible borrowing capacity in a deteriorating social and political environment. Exports do not close the gap either if the shock is global or if trade partners are facing similar problems. That leaves investment, but investment is only sustainable if there is future consumption to make it profitable. Investing massively in AI to produce more in a world where demand is collapsing is, at the very least, an internal contradiction.

For the picture to make sense, one has to introduce what the narrative only half-addresses: distribution. A world of rising productivity with stagnant consumption for the majority can exist if income becomes more concentrated, if the surplus is channeled outside the domestic consumption circuit, or if the beneficiary is another economic bloc. In that case, the problem is not that GDP is ghostly, but that the distribution of it makes the system politically unstable. And that is where another weak point in pure doomerism appears: if the consumer base becomes poorer, the extraordinary returns that justify the AI investment cycle eventually run into their own ceiling. Concentration can hold for a while, but it is hard to see how it can be sustained indefinitely without a political, fiscal, or regulatory response, or without some reallocation of income toward effective demand.

In the end, the virality of the post says more about the emotional state of the market than about the coherence of the scenario. In an expensive stock market, with the AI narrative already embedded in prices and with growing doubts about who monetizes what and when, any story that turns a diffuse concern into a complete narrative gains traction. Not because it is the best explanation of the present, but because it puts words to an old fear.

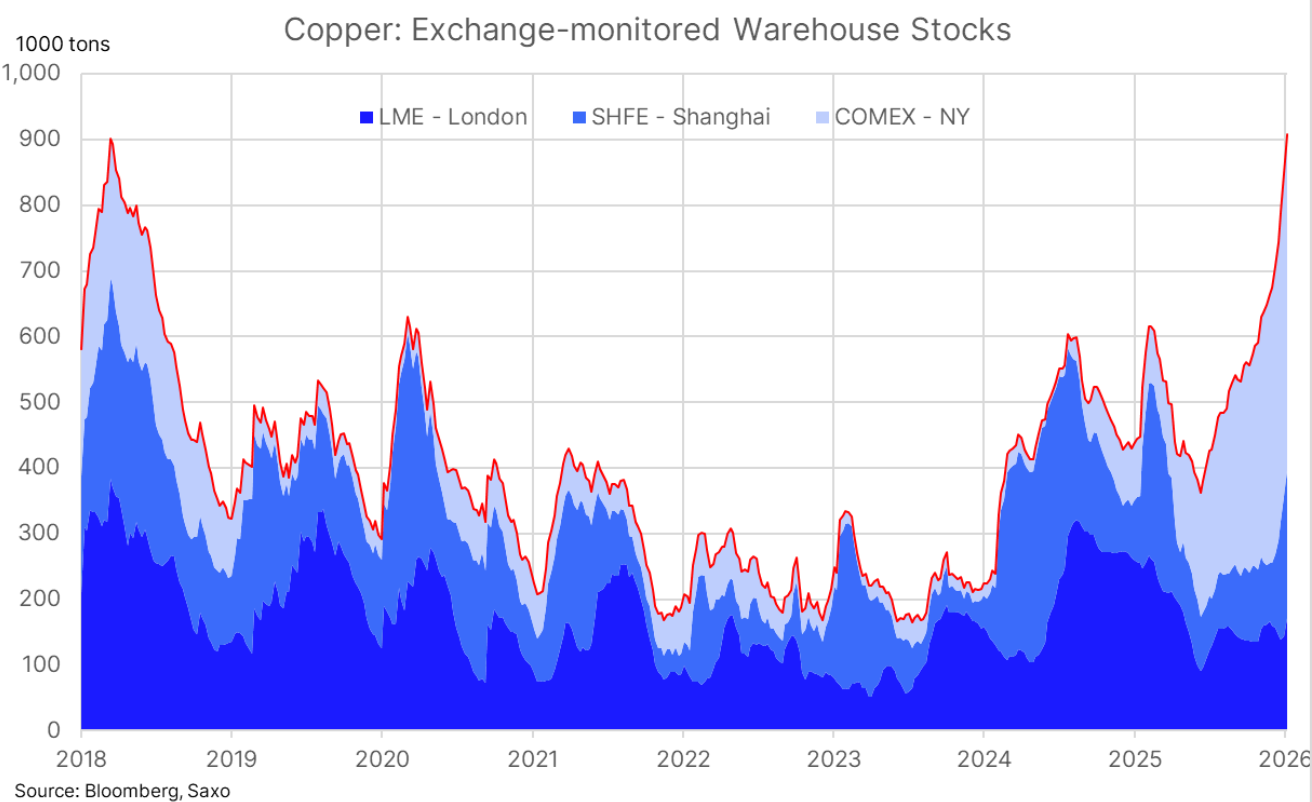

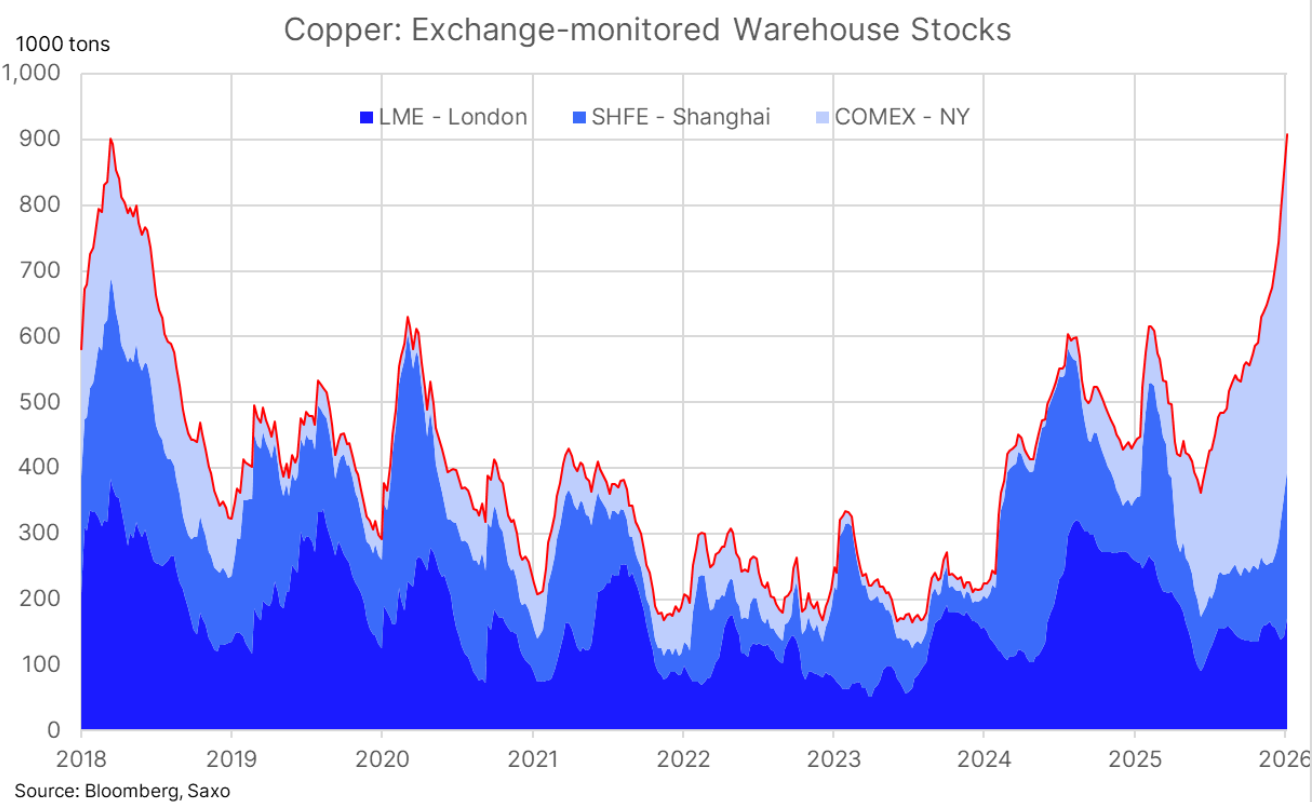

For months now, there has been a consistent emphasis on the alarming rise in copper inventories, especially in the United States. This seems to suggest that the sharp price increases being seen are not so much the result of a true market imbalance, but rather of strategic stockpiling in a world shaped by political fragmentation and tariffs. Robert Friedland, the GOAT, however, has a different view, though of course he is hardly a disinterested party.

According to him, the debate around global inventories is conflating inventory with availability, because the market still treats stocks as if they were one single liquid pool, when in reality there are two distinct worlds. On the one hand, there is commercial inventory, which responds to price, spreads, and arbitrage. On the other, there is political inventory, which responds to national security concerns. From an accounting standpoint, both are copper. Economically, they are nothing alike. The United States is a good example. Moving from roughly 85,000 tonnes to around 520,000 in a year is a regime signal. In a world of tariffs, technological rivalry, and militarized supply chains, assuming that copper is exportable “if the price is right” is equivalent to assuming the state will simply stand by and watch. There may be no explicit ban, but none is needed. Licenses, inspections, regulatory pressure, and operational friction are enough to make that metal, in practice, domestic only. In terms of the global balance, that copper is there, but it is the market.

China is the same phenomenon under a different label. A strategic stockpile of less than 500,000 tonnes, even if that figure were exact, would not cover even a month of consumption. More importantly, it is not a static deposit. Part of it is pre-allocated or consumed in sensitive uses that do not show up in the “clean” reporting. The key point is that price is not set by total stock, but by marginal stock, the portion that can actually be released when the market tightens. If marginal inventory is in the hands of governments or inside jurisdictions that prioritize strategic autonomy, elasticity disappears. In theory, China should hold roughly three months of consumption in reserves, according to its recent policy stance, and the hardening of that stance as expectations build around what may happen in Taiwan, which means there is still room for further stockpiling, especially now that the Chinese New Year pause has ended.

It should no longer surprise anyone that investment bank analysts have zero independent judgment and simply adapt the narrative to whatever the price action is doing. We have seen it many times in their target prices for stocks that fall (or rise), and now once again with oil. After publishing a report just a few months ago calling for oil at $50/bbl during 2026, and now seeing that none of their arguments about massive surpluses still hold up, Goldman Sachs is suddenly saying it expects a price range 10% higher in 2026 and 2027, clinging to whatever argument allows them to save face.

On the other hand, on March 1, the eight OPEC+ producers are meeting again to discuss the next phase of the production cut “unwinding.” The number currently circulating as a rumor is a modest increase of around 137k b/d, and the market is already extrapolating that as if it were the start of a steady drip of supply throughout the rest of 2026. From a fundamental standpoint, that kind of increase changes the physical market balance by virtually nothing, and OPEC+ is also operating close to its operational limit and, more importantly, close to its export limit. Saudi Arabia, the UAE, and Iran are already exporting at or near full capacity. In Saudi Arabia’s case, there may be some room left, perhaps around 500k b/d more to average roughly 7.5Mb/d, but that is where the story ends. In the UAE and Iran, spare capacity is essentially zero. In short, what is being discussed on March 1 matters more for sentiment than for actual flows.

Model Portfolio

Year to date, the model portfolio is up +18.54%, versus +0.15% for the S&P 500 (S&P in euros), and +205.6% since inception (September 2022), compared with +50.5% for the S&P 500. The model portfolio, as of Friday's close, is as follows:

⚠️Past performance does not guarantee future results. The historical performance of the model portfolio is shown for informational and educational purposes only and does not constitute investment advice or an offer to buy or sell securities. The returns shown may not include fees, taxes, or other associated costs.