Disclaimer

LWS Financial Research is NOT a financial advisory service, nor is its author qualified to offer such services.

All content on this website and publications, as well as all communications from the author, are for educational and entertainment purposes only and under no circumstances, express or implied, should be considered financial, legal, or any other type of advice. Each individual should carry out their own analysis and make their own investment decisions.

Weekly macro summary

There have been quite a few interesting events to analyze this week, and below I list the most noteworthy news. Let’s get started:

The Fed kept rates unchanged at 3.5%–3.75%, but the key point was not the decision itself, which was fully priced in, but the internal fracture within the committee. The vote was the most divided since 1992, with eight members supporting the decision to hold rates, three rejecting the dovish bias in the statement, and one, Stephen Miran, voting directly for a 25-basis-point cut. In other words, Powell is leaving behind a Fed split into three camps: those who want to wait, those who believe the next move should still be a cut, and those who no longer even want to hint at easing.

The change in language also offered quite a few clues. Inflation is no longer described as “somewhat elevated” but simply as “elevated.” It may seem like a minor nuance, but it is not. The Fed is acknowledging that the energy shock stemming from the war with Iran, with oil back above $100, makes the normalization narrative much more complicated. Until now, the market was still clinging to the idea that cuts were only a matter of time. After the meeting, futures no longer priced in any cuts in 2026 and even briefly assigned a non-negligible probability to a rate hike over the next year. The market is beginning to accept that the Fed may not have as much room to cut as previously thought, despite Warsh’s arrival, especially if the economy continues to grow at a solid pace and energy inflation threatens to filter through into expectations, wages, or core inflation.

Kevin Warsh will inherit a much less compliant Fed than he probably expected. If his intention was to arrive with a clear mandate to cut rates, the committee has just sent him a preventive message: there will be no blank check. The three hawkish dissenters did not vote against holding rates, but against maintaining the easing bias. If the oil shock fades over the coming months, the Fed will be able to refocus on the weaker side of its mandate: employment, growth, and the risk of a slowdown. But if crude remains high, the narrative changes completely. Central banking history is full of mistakes made by treating energy shocks as transitory when they ultimately contaminate the rest of the economy.

SpaceX has approved a new compensation package for Elon Musk that, even by Musk’s own usual standards, borders on science fiction. The company’s board has reportedly designed a pay plan tied to extraordinarily ambitious milestones: reaching a $7.5T valuation, establishing a permanent colony on Mars with at least one million people, and operating data centers in space with 100 terawatts of computing capacity.

The figure is difficult to put into context because there is simply no comparable precedent. We are not talking about improving margins, growing revenue, or expanding EBITDA, but about objectives that belong more to SpaceX’s founding mission than to the traditional corporate governance playbook. The package includes up to 200 million restricted super-voting shares if the milestones linked to Mars and valuation are achieved, plus another 60.4 million shares tied to additional valuation targets and the construction of orbital computing infrastructure. All of this would be in Class B shares, carrying 10 votes for every Class A share, further reinforcing Musk’s control over the company.

The obvious reading is that SpaceX wants to ensure Musk remains mentally anchored to the project ahead of a potential IPO. The company is reportedly targeting an IPO around June 28, Musk’s birthday, at a potential valuation close to $1.75T. If that figure already seems extraordinary, the plan approved by the board implies multiplying that value several times over and turning SpaceX not only into the dominant space company, but into critical infrastructure for a multiplanetary civilization and, potentially, for the future of computing.

The uncomfortable point is that SpaceX and Tesla are, in practice, competing for the attention of the same person. Tesla already justified its own massive compensation package by arguing that it needed to keep Musk focused on the company, especially at a time when the electric vehicle business faces greater competition, margin pressure, and a narrative increasingly dependent on autonomy, robotics, and artificial intelligence. Now SpaceX is using a similar logic, but with even more extreme objectives. The result is an incentive conflict that is difficult to ignore: two enormous companies, with different shareholder bases, trying to buy time and focus from the same founder.

If Musk does not achieve the targets, he does not receive the shares. But if he does, the reward could be enormous and come with even greater voting power. In theory, this aligns incentives with value creation. In practice, it also consolidates a structure in which the founder increasingly concentrates control, and where minority shareholders must accept that the investment thesis depends extremely heavily on a single individual. The risk, meanwhile, is just as obvious: extreme valuation, founder dependence, technological complexity, and objectives with no historical precedent. But so is the reason why the market may be willing to pay multiples that would look absurd in almost any other sector.

OpenAI is once again facing the same question hanging over the entire artificial intelligence industry: not whether demand exists, but whether it is arriving fast enough to justify the level of investment already committed. According to the WSJ, the company has reportedly missed several internal user and revenue targets in recent months, raising concerns within management itself about its ability to absorb the huge computing and data center contracts already signed or under negotiation.

The company continues to grow, and ChatGPT remains the benchmark consumer AI product, but the economics of generative AI require near-perfect scale. Every additional user consumes infrastructure, inference capacity, chips, energy, and data center resources. Unlike traditional software, where incremental margins tend to be extremely high, here the cost of serving demand remains material.

For months, the market has been funding the expansion of AI on the assumption that future demand will absorb any excess capacity. The other relevant angle is competition. OpenAI has reportedly lost ground to Anthropic in key markets such as coding and enterprise, precisely where monetization is most attractive and where customers can justify higher spending. This matters because the consumer market can provide scale and brand recognition, but the real profit pool will likely be in enterprises, productivity tools, workflow automation, and vertical software. If Anthropic begins to capture a growing share of that segment, pressure on OpenAI increases, especially given such an aggressive cost structure.

There is also a signal of product maturity. ChatGPT reportedly fell short of its internal goal of reaching 1 billion weekly active users by year-end, while dealing with subscriber cancellations and weaker adoption momentum. This fits with an idea we have been discussing: the phase of explosive growth and novelty-driven adoption is starting to fade. AI is no longer just a viral curiosity; it is becoming a recurring, useful, but more normalized tool. AI can be transformational and, at the same time, overcapitalized in certain parts of the value chain.

As it has done every Friday for weeks, Axios published a new “story” that seemed to bring permanent peace in the conflict between the United States and Iran closer. The objective, clearly, was to try to push crude prices lower, but the effect is becoming smaller each time, both in magnitude and duration, as it increasingly seems obvious that any solution will be complicated. If the Strait of Hormuz remains closed over the coming weeks, the oil market would enter territory that is almost impossible to model. Sell-side analysts will try to assign a price target to crude, as always, but the reality is that there is no comparable historical precedent. The potential supply loss — between 11 and 13 million barrels per day — cannot be absorbed through a simple price increase or marginal demand adjustments. The only useful reference point would be a COVID-style demand destruction shock: mandatory lockdowns and government-directed economic paralysis.

Outside that scenario, the market has never destroyed demand on this scale through purely economic mechanisms. Not even during the Great Financial Crisis of 2008 did we see anything resembling a 12% decline in global demand.

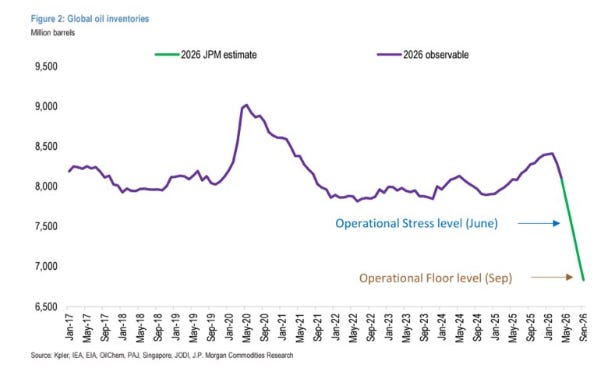

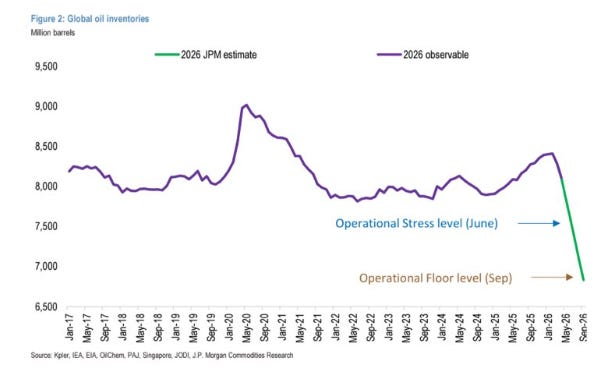

The latest inventory data are already starting to show the scale of the imbalance. The EIA reported a massive 24.1 million-barrel draw in petroleum inventories, even with a 7.1 million-barrel release from the strategic reserve. Commercial crude inventories in the U.S. alone fell by 6.2 million barrels. And this is happening while some VLCCs that were already loaded and heading to the United States are still being discharged, which is keeping imports artificially elevated in the short term.

But this buffer is temporary. Those same cargoes that are supporting imports today will turn into lower available volumes in one or two weeks. In addition, there is a fleet of empty VLCCs heading toward the United States, suggesting that the drawdown in commercial inventories could accelerate sharply. On top of this, refined product inventories are also likely to keep falling, while U.S. exports of petroleum products remain near historical highs. In practice, we could see weekly EIA reports showing crude draws of 10–12 million barrels even alongside 10 million-barrel releases from the SPR. In other words, an effective cumulative reduction of 20–22 million barrels in a single week. If that happens, even generalist investors will realize that the problem has become impossible to ignore.

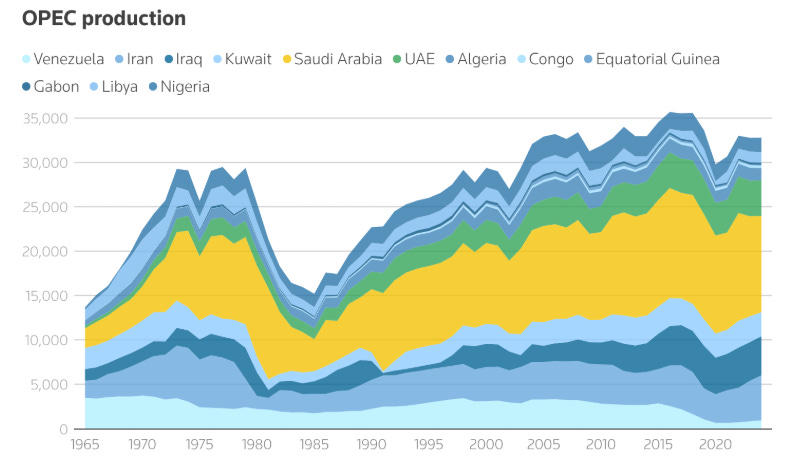

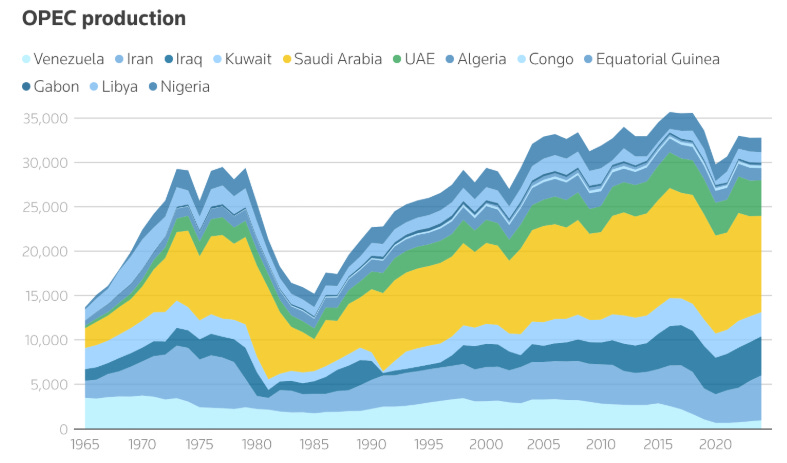

The United Arab Emirates’ exit from OPEC represents a significant blow to the traditional architecture of the oil market, although its immediate impact is partially cushioned by the blockade of the Strait of Hormuz. Under normal conditions, one of the group’s largest producers leaving both OPEC and OPEC+ would be a clearly bearish signal for crude, as it frees Abu Dhabi from production quotas and allows it to increase output once logistical restrictions disappear. But while Gulf crude remains trapped, the ability to produce more does not translate into the ability to export more.

The decision reflects an increasingly visible fracture between the UAE and Saudi Arabia. For years, Riyadh has acted as the market’s central stabilizer, absorbing much of the political and economic cost of production cuts. The UAE, by contrast, has been investing for some time to expand capacity and no longer wants to accept limits designed for a balance that favors Saudi Arabia more than its own ambitions. This weakens OPEC’s coordination power over the medium term and could effectively mark the end of the organization, given the enormous loss of relevance — they now control 40% of global supply. If the UAE, one of the few countries with real spare capacity alongside Saudi Arabia, decides to act outside the cartel, Riyadh’s ability to manage the market is reduced. More importantly, it raises an uncomfortable question: if market adjustment increasingly depends on a single producer, how sustainable is Saudi Arabia’s role as the central bank of oil?

For Trump, the UAE’s exit can be sold politically as a victory. It fits his long-standing rhetoric against OPEC, which he accused of manipulating prices while the United States bore the military cost of defending the Gulf. The war with Iran has exposed a weakness that the market used to treat as a tail risk, but which is now at the center of the system. Around one-fifth of the world’s crude oil and liquefied natural gas passes through the Strait. If that artery is compromised, OPEC+’s weight in global supply falls mechanically, not because producers decide to cut output, but because they cannot place their production on the market. In fact, OPEC+’s share would already have fallen from 48% to 44% in barely a month, and could continue declining if production shutdowns intensify.

Model Portfolio

Year to date, the model portfolio is up +20.33%, versus +5.83% for the S&P 500 (S&P in euros), and +210.2% since inception (September 2022), compared with +59.0% for the S&P 500. The model portfolio, as of Friday's close, is as follows:

⚠️Past performance does not guarantee future results. The historical performance of the model portfolio is shown for informational and educational purposes only and does not constitute investment advice or an offer to buy or sell securities. The returns shown may not include fees, taxes, or other associated costs.