Weekly summary 06/04

Disclaimer

LWS Financial Research is NOT a financial advisory service, nor is its author qualified to offer such services.

All content on this website and publications, as well as all communications from the author, are for educational and entertainment purposes only and under no circumstances, express or implied, should be considered financial, legal, or any other type of advice. Each individual should carry out their own analysis and make their own investment decisions.

The publication has grown significantly over these months, fueled by a community that has become a reference point, organized around Discord (for which we will continue to work on improving quality and reducing noise), and the good results obtained. The annualized return (CAGR) has been 38.64% in my personal account, and +48% since inception (September 2022) in the model portfolio, with the same philosophy, which only differ in the allocation of weights and the use of options.

We are now around the top 100 globally, which exceeds the expectations, due to the speed at which the goal was achieved, which I had when I started this journey at the end of 2022.

As always when something grows quickly (a clear example with M&A operations in the market), this development is, in part, chaotic until the new dimension of the project is assimilated, and then I share with you the new roadmap of the publication to ensure that this transition does not alter the essence of the community:

Implementation of new sector reports, M&A monitoring, special situations, etc., and a weekly report with the main news, progress, and topics discussed on Discord for those who have less time to devote to it on a daily basis.

Incorporation of new top-level collaborators to allow us to delve into sectoral and industry dynamics.

Slight changes in the Discord channel structure to allow conversation and interaction while avoiding excessive noise and information overload.

Price increase for NEW subscribers, which will change from €132/year to €240/year (20€/month) in the annual format, and from €16.5/month to €24/month in the monthly format. The idea behind this measure is precisely to be able to support the data, information, and collaborators structure that we are implementing.

For current subscribers, as I already mentioned in February, NOTHING changes, meaning this price increase does NOT affect you, and you will ALWAYS have a price advantage over new members (a cheaper tier until the eventual perpetual freezing of fees). The price increases will take effect on Monday, so this is the LAST chance to subscribe at this price.

Weekly macro summary

There have also been quite a few interesting events to analyze, and below I list the most noteworthy news. Let's get started:

The reacceleration of commodity prices is very bad news for the Fed and its crusade against inflation, as they are a basic input in any industrial activity and also play a key role in anchoring inflation expectations, which often ends up becoming a self-fulfilling prophecy.

This fact has not gone unnoticed by the market, which is already beginning to question whether the American central bank will consider rate cuts in June. I still believe that other factors, despite the discomfort of the situation, will weigh more on the balance, and that, if nothing is done, interest expenses at the end of the year would be at a run rate of $1.6 trillion/year vs the current $1.1 trillion/year, which would only increase by $100 billion if they reduce the reference rates by 150 bps.

Gold is the commodity that best reflects the unsustainable path of the dollar as a hegemon, and it no longer trades, as it historically has, in relation to real interest rates, but rather its price is determined by non-Western central banks, which are the marginal buyer, in their efforts to escape the American yoke. On the other hand, if inflationary fears materialize, purchases derived from traditional drivers of the gold price will add to this trend, so it seems that the bullish market still has (much) room to run.

Furthermore, although concerning, increases in commodity prices should not be able to trigger a new inflation peak if they are not accompanied by inflation in services and shelter, of which, for the moment, there are no indications. Thus, we could have a scenario similar to that of 2011-2014, where inflation would not reach the Fed's 2% target but would remain in the range of 3%-4%, which, while not optimal, allows for normal economic activity.

Israel has escalated tensions in the Middle East by bombing the Iranian embassy in Syria, resulting in the deaths of several Iranian Revolutionary Guard commanders and sparking outrage from Iran, which has been in a constant state of uneasy calm with the Jewish state. Additionally, the attacks have inadvertently targeted some aid convoys, such as those belonging to the NGO of Spanish chef José Andrés, further diminishing the already scant sympathies they garner in the international sphere.

In line with retaliatory threats announced by Tehran, the CIA has warned Israel to prepare for an attack within the next 48 hours. However, it is most likely that the attack will not occur directly to avoid total confrontation: it may be carried out through proxies or target Israeli infrastructure outside Jewish territory. Naturally, the market received this news with concern, leading to significant drops in major indices while oil prices surged to exceed $91 per barrel.

As the halving approaches, price volatility is increasing, as many mining companies sell their inventories to finance their operations during the transition period to reduced rewards. My idea, for which I do not expect as significant an impact on the price as in previous cycles, is that we have yet to see much in terms of ETF demand, as Registered Independent Advisors (RIA) have not had access to the vehicle. It is expected that major banks such as Morgan Stanley, UBS, Goldman Sachs, etc., will begin marketing them as early as next week, as some ETF prospectuses, such as BlackRock's, have already been amended to include them as intermediaries.

Meanwhile, the United States government has begun the process of selling 30,170 BTC seized during the Silk Road shutdown operation, which totaled 195,000 BTC. Although they had initially announced that they would hold them as a strategic asset, short-term vision has led them in other directions. In my opinion, this is a serious error in vision (the money is of negligible magnitude in the context of the US budget), stemming from the original sin of the Western democratic system, where legislation is framed in terms of elections rather than the country's long-term prosperity.

This week, although crude oil inventories themselves have not been spectacular: +3.21 million barrels of crude, -0.377 at Cushing, -4.256 million barrels of gasoline, and -1.268 million barrels of distillates, the figures for implied demand have experienced a strong upward surge, reaching the highest level in the past 5 years, which is very positive for the bullish thesis of oil.

Of course, the significant surge in crude oil prices (> $90/bbl) is mainly due to geopolitical risks in the Middle East, which threaten to cause a real disruption in supply. However, what is necessary for these levels to be sustainable is an improvement in fundamentals in the physical market. With this price increase, it seems that the US Department of Energy (DoE) is now abandoning the idea of filling the strategic reserve, and they must regret not having taken advantage of Donald Trump's proposal to do so when crude oil was trading at $20/bbl.

As is customary, investment bank analysts are always lagging behind, and just as with target prices, they chase the narrative, with Bank of America completely changing its forecasts and message on the market balance with just three months' difference. That's why it's so important, in addition to being flexible, to have our own independent thinking, allowing us to position ourselves optimally in each market environment.

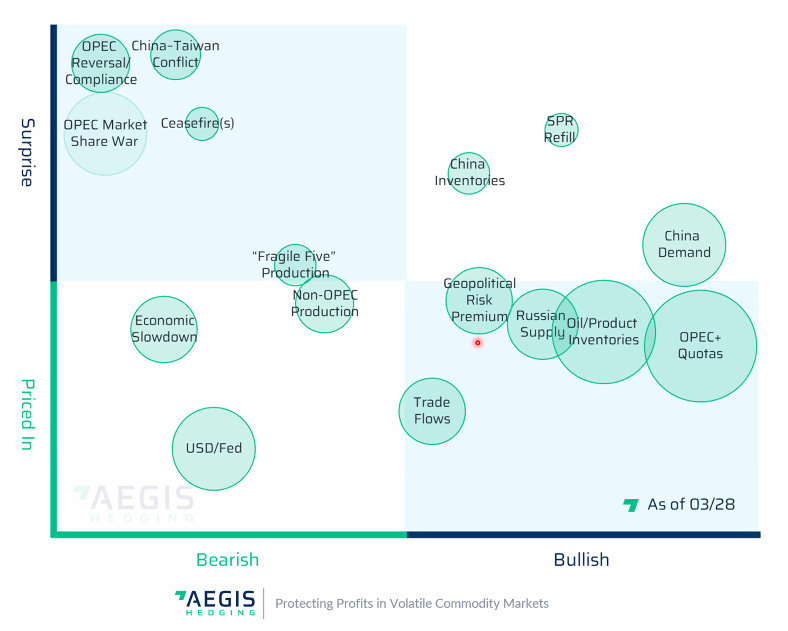

I also want to share with you a very interesting chart by Christine Guerrero where various factors impacting the oil market are classified in a matrix (positive/negative, surprise/discounted), allowing for a fairly accurate classification of day-to-day macro news or events.

Model Portfolio

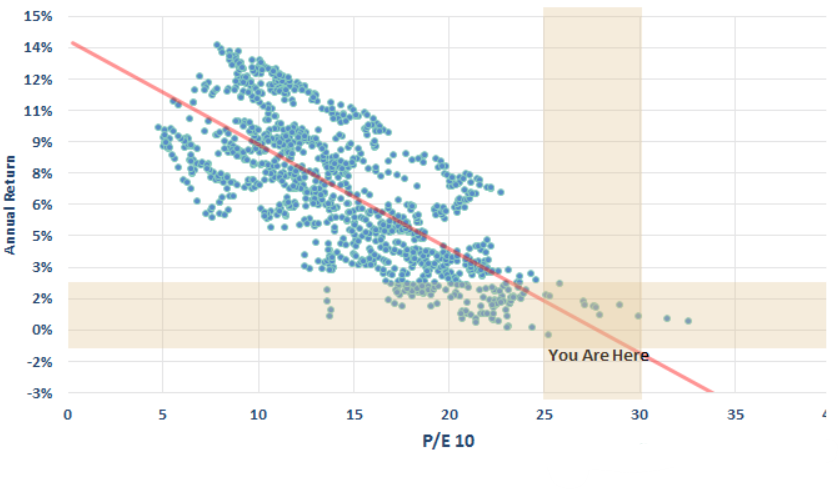

The valuation aberrations in the market, though frequent, usually don't last long. As the famous motto goes:

You can fool some of the people all the time, and all of the people some of the time, but you cannot fool all of the people all the time.

In 2021, we witnessed a collective euphoria episode towards certain narratives, such as renewable energies or electric vehicles, which seemed to be on an unstoppable path towards market dominance; in this context, Tesla's valuation reached $1.2 trillion, surpassing that of all its major competitors combined, despite its profit generation being 95% lower.

At that time, of course, there were arguments and justifications for the valuation dissonance: Tesla is not really a car manufacturer, and the real business is software, the potential of autonomous driving and robotaxis, the energy sector, and a long list of projects championed by the genius Musk. Fast forward to today, we see how the market has purged the previous excesses and, despite recognizing that several of these mentioned initiatives make sense and can end up creating a lot of value, valuation matters, and the company's vehicle deliveries, far from registering the much-predicted growth, reflect a very significant drop and a clear deceleration in demand.

Except in very exceptional cases, the return obtained shows a strong correlation with the price paid, and a very high valuation multiple incorporates many expectations that, if not met, completely ruin the IRR of our investments. The underlying logic is clear: a lower valuation, ceteris paribus (of course, this reflection is a huge conceptual simplification), leaves room for many more errors in our models and projections. That's why value investing will never go out of style since buying cheap will never be a bad strategy.

The model portfolio's return is +11.79% YTD compared to +8.89% for the S&P500, and +48.01% versus +30.27% for the S&P500 since inception (September 2022).

Keep reading with a 7-day free trial

Subscribe to LWS Financial Research to keep reading this post and get 7 days of free access to the full post archives.