Disclaimer

LWS Financial Research is NOT a financial advisory service, nor is its author qualified to offer such services.

All content on this website and publications, as well as all communications from the author, are for educational and entertainment purposes only and under no circumstances, express or implied, should be considered financial, legal, or any other type of advice. Each individual should carry out their own analysis and make their own investment decisions.

Weekly macro summary

There have been quite a few interesting events to analyze this week, and below I list the most noteworthy news. Let’s get started:

Nvidia is once again making a move to bring artificial intelligence out of the data center and directly into the PC. The company has unveiled RTX Spark, a new chip developed alongside MediaTek and Microsoft, with which it aims to turn the personal computer into a machine capable of running AI agents locally, without always depending on the cloud. The idea is that if the next computing interface is not an app, but an autonomous agent working in the background, today’s hardware falls short. After the phase of massive training in the cloud, the next battle appears to be shifting toward the edge — that is, toward devices capable of running models and agents locally. Qualcomm is also framing it this way, describing 2026 as “the year of agents.” The logic makes sense: if these systems are going to operate continuously, with low latency, access to private data and a degree of autonomy, not everything can go through remote servers. There will be growing demand for distributed computing.

For Nvidia, this opens up a new growth avenue beyond data centers, where it already dominates overwhelmingly. With RTX Spark and the Vera CPU, the company is moving directly into the traditional territory of Intel, AMD, Qualcomm and Apple. It is not simply trying to sell a more powerful GPU for gaming or design, but to redefine the PC as an AI-native platform. The pre-market declines in AMD, Intel and Qualcomm reflect fears that Nvidia could do in PCs what it has already done in servers: impose its standard before the rest can react. Still, it is important not to confuse narrative with immediate adoption. The PC with local agents still needs clear use cases, reasonable costs and a real improvement over today’s cloud-based experience. The iPhone reorganized the mobile ecosystem; ChatGPT reorganized the software layer; Nvidia is now trying to do the same with PC hardware. Whether RTX Spark will truly become the foundational moment the market is promising remains to be seen, but the strategic direction is clear: AI is no longer just a tool in the cloud; it is beginning to become a permanent layer of the personal computer.

Lisa Cook reinforces an idea that the market still does not seem willing to fully accept: the Fed is not yet in a position to declare victory over inflation. Quite the opposite. Although she supports keeping rates unchanged for now, her message is clearly more hawkish than one might expect in a context where Trump has placed Kevin Warsh at the head of the Fed with the expectation of accelerating rate cuts.

The problem is that the macro picture has become much more uncomfortable. Tariffs are still feeding through into prices, oil has become more expensive because of the war with Iran, and the investment boom in artificial intelligence is creating additional pressure in chips, software and data center construction. In other words, inflation is no longer coming from a one-off shock, but from several simultaneous forces pointing in the same direction. Cook still expects some of these pressures to moderate in the coming months, but she acknowledges that the risk is clearly tilted toward more persistent inflation.

What matters is not so much whether the Fed is going to raise rates tomorrow, but that the bar for cutting them appears higher than part of the market is discounting. After five years of inflation above 2%, the concern is no longer just the monthly data point, but the possibility that companies and workers start embedding structurally higher inflation into their pricing and wage decisions. The other side of the mandate, employment, remains relatively stable. Cook acknowledges that the accelerated adoption of AI could lead to job destruction before generating new productivity gains, but for now she does not see enough deterioration to justify preventive cuts. Even Trump, who has been so vocal about rate cuts, now recognizes that the macro reality has changed and is no longer constantly calling for cuts, giving poor Warsh a bit more room to maneuver.

Anthropic has confidentially filed paperwork to go public in the United States, moving ahead of OpenAI in a race that is starting to look less technological and more financial. The company has not yet disclosed the size or terms of the transaction, but its latest funding round already valued it at close to $965 billion, after more than doubling its valuation since February. If confirmed, this would be one of the largest IPOs in recent history, not only because of its size, but because of what it implies for the narrative underpinning a large part of the US market.

It is worth remembering that SpaceX is also moving toward a mega-IPO at a $1.75 trillion valuation, while OpenAI has been preparing its own process for weeks. In other words, some of the most important private companies in the world are trying to access the public market almost at the same time, competing for an amount of capital that, while enormous, is not infinite. The market window is open, but precisely for that reason everyone wants to get through it before it closes.

Anthropic’s listing will carry a dual interpretation. On the one hand, it will likely be the first major foundation model company to show its audited numbers to the market, setting the framework through which investors will assess revenue, margins, cash burn, computational capex and dependence on cloud providers. On the other hand, it is taking the risk of being the first to face real scrutiny. Until now, the private market has valued these companies based on growth, promise and fear of missing out. The public market will demand something more uncomfortable: unit economics, visibility and returns on an extremely capital-intensive infrastructure. If Anthropic manages to convince investors that its business model can scale profitably, it will validate a large part of the ecosystem. If, instead, its accounts reveal a structure that is too dependent on compute spending, cross-subsidies or constant external financing, it could open a crack in the narrative surrounding the entire sector.

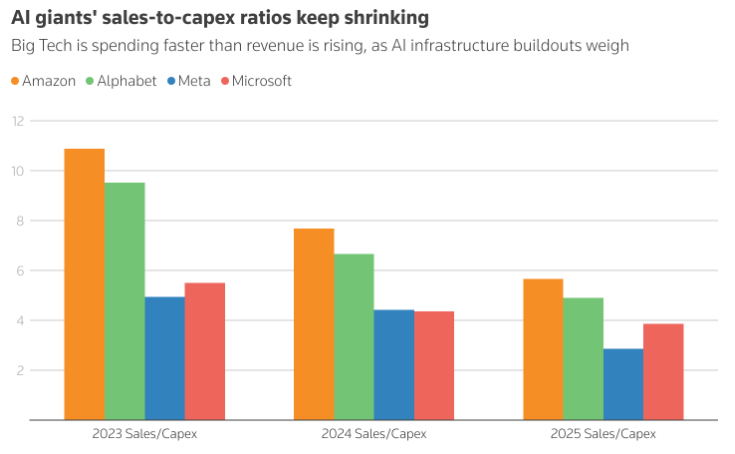

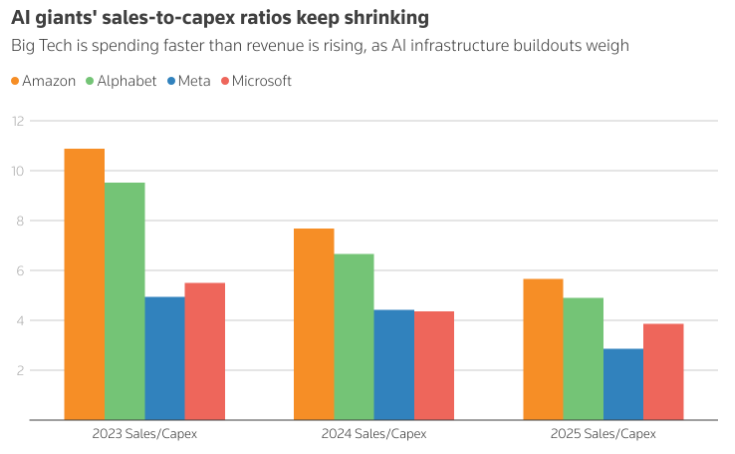

For its part, Alphabet has announced a capital increase of up to $80 billion to finance the expansion of its artificial intelligence infrastructure, in a move that confirms just how much the race for compute capacity has become a balance sheet war. The transaction includes a direct $10 billion investment from Berkshire Hathaway, split between Class A and Class C shares, at prices slightly below the market close. Alphabet had already raised its annual capex guidance to $180-190 billion, after acknowledging that demand for AI and cloud solutions is exceeding its available capacity. The problem is that this demand requires an increasingly aggressive investment scale. The company has raised more than $85 billion in debt over the past year, taking its total balance above $100 billion, and is now also turning to equity. In other words, even one of the best businesses in the world is beginning to need massive external financing to sustain the pace of the race.

Berkshire’s entry provides an important reputational endorsement. For the market, the fact that Buffett — or perhaps already Greg Abel — is strengthening Berkshire’s position in Alphabet lends credibility to the idea that AI spending is not simply a capex bubble with no return. But if a company with Alphabet’s cash generation needs to issue shares, raise debt and launch at-the-market programs to fund its rollout, then the capital intensity of the new technology cycle is far greater than many investors had been discounting. The market is valuing many companies as if we were facing a new Google Search, but the competitive structure looks much less like a natural monopoly and much more like an infrastructure race with uncertain returns.

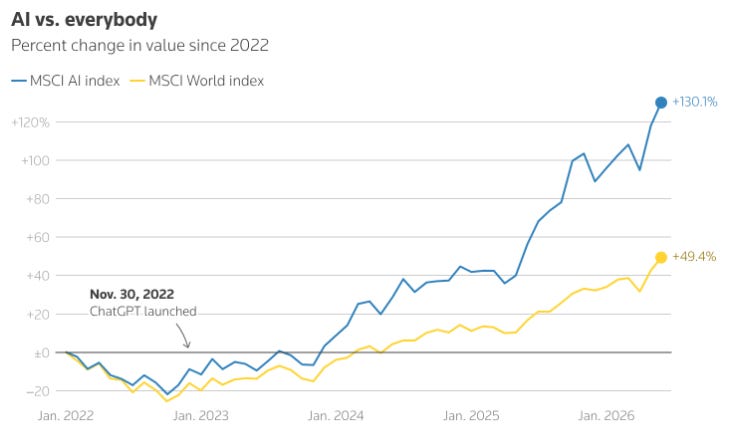

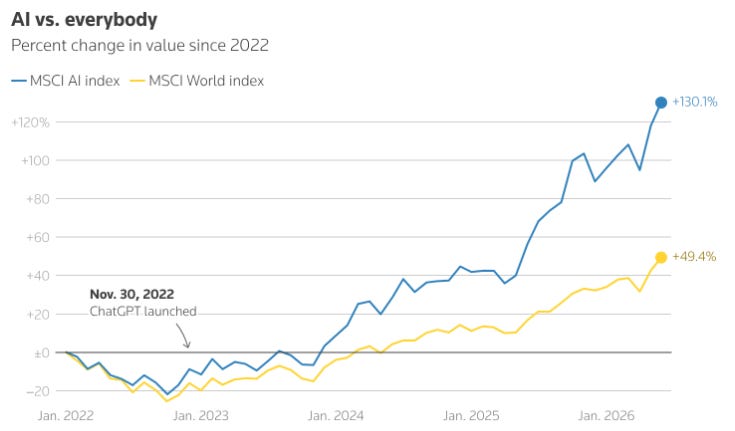

The key point is that “AI” is not a single market. In search, Google built a flywheel that was extremely difficult to replicate: more users generated more data, better results, more advertisers, more revenue, more investment, and the cycle started again. In addition, the product was cheap to serve relative to its monetization power. In generative AI, at least for now, the dynamic is different. Leading models are converging, they are trained on similar corpora, researchers move between companies, architectures are copied quickly, and end users can switch providers with relative ease. If the output of Claude, Gemini, ChatGPT or Llama ends up being “similar enough,” differentiation compresses. If there is no clear moat, there is no pricing power. And if there is no pricing power, massive capex becomes a dangerous bet. Everyone is investing as if they were going to capture monopoly rents, but perhaps the market will end up paying commodity-like returns.

The oil market is behaving as if it still had room to maneuver, but physical reality is starting to tell a different story. In theory, prices should be pricing in demand destruction to prevent global inventories from reaching minimum operational levels. However, the market seems more focused on headlines about memorandums of understanding, ceasefire rumors, and false diplomatic signals than on fundamentals.

The problem is that this is no longer a distant risk. According to this view, we could be just a few weeks away from reaching critical inventory levels. What appears to be taking place is one of the fastest declines in onshore oil inventories in history. Even if the Strait of Hormuz were to reopen immediately, a large part of the inventory drawdowns would already be inevitable because of the lag between supply, consumption, and replenishment. With strategic reserve releases close to 9-10 million barrels per week, preliminary estimates point to another 13-14 million barrel draw next week. In addition, with U.S. refineries processing around 17 million barrels per day, U.S. commercial crude inventories would begin to reflect the full pressure of the physical deficit.

The situation is starting to resemble living paycheck to paycheck. Immediate shortages may be avoided, but any additional disruption — a refinery outage, a pipeline issue, or a hurricane — could trigger real pressure in gasoline and distillates. The market continues to treat the closure or control of the Strait of Hormuz as a temporary event, when it could actually represent a structural change as long as the IRGC retains effective control over the passage. Governments are using strategic reserves as if they were a bridge for just a few weeks, but if the problem is not resolved quickly, those reserves merely buy time while commercial inventories continue to drain.

This is the real geopolitical fork in the road: either the IRGC controls the Strait of Hormuz, or it does not. There is no comfortable middle ground. Analysts keep looking for a path toward diplomatic normalization, but unless there are massive concessions, I see that as impossible. Investment banks are already starting to move toward this conclusion, and JPMorgan is laying out a base case with Brent around $100 per barrel through the end of the year, assuming the Strait of Hormuz reopens this very month. But each additional month of closure would add significant pressure: around $5 per barrel in the third quarter and up to $15 per barrel in the fourth quarter.

Model Portfolio

Year to date, the model portfolio is up +25.37%, versus +10.17% for the S&P 500 (S&P in euros), and +223.2% since inception (September 2022), compared with +65.6% for the S&P 500. The model portfolio, as of Friday's close, is as follows:

⚠️Past performance does not guarantee future results. The historical performance of the model portfolio is shown for informational and educational purposes only and does not constitute investment advice or an offer to buy or sell securities. The returns shown may not include fees, taxes, or other associated costs.