Disclaimer

LWS Financial Research is NOT a financial advisory service, nor is its author qualified to offer such services.

All content on this website and publications, as well as all communications from the author, are for educational and entertainment purposes only and under no circumstances, express or implied, should be considered financial, legal, or any other type of advice. Each individual should carry out their own analysis and make their own investment decisions.

Weekly macro summary

There have been quite a few interesting events to analyze this week, and below I list the most noteworthy news. Let's get started:

Anthropic is an uncomfortable reminder that in AI, the technological “moat” is worth less than the market thinks once you collide with the State. State, Treasury, and HHS have ordered staff to stop using Claude by direct directive from Trump, joining the Pentagon, and redirecting teams toward alternatives like ChatGPT and Gemini, with fewer ethical constraints. This isn’t a vendor switch driven by performance—it’s a de facto political sanction: a way of turning a domestic player into an administrative pariah for not accepting the usage terms Washington wanted to impose, especially around military guardrails, autonomous weapons, and potential domestic surveillance. The administration is making it clear who runs the deployment chain when a technology is considered critical to national security and the country is in a global race against other powers like China. You can have the best model, but if you don’t accept the government’s operating framework, they flip the switch off—starting with the most visible and symbolic demand: federal usage. This also creates a second-order effect: if you’re blacklisted in core agencies, many vendors, integrators, and internal teams become allergic to reputational and compliance risk, and the ban becomes self-reinforcing even if there isn’t a broad “legal prohibition.”

For OpenAI and Google, this is close to an ideal scenario. They don’t just capture share—they also cement the standard. In fact, the text notes that OpenAI has already announced an agreement to deploy technology on the DoD’s classified network, and that Altman rushed to add a written clarification that it will not be intentionally used for domestic surveillance of U.S. citizens or nationals. In AI, the risk isn’t only competing against another model—it’s competing inside a framework where the dominant buyer can rewrite conditions, define acceptable uses, and pick winners by decree. The market tends to underweight this kind of risk until it materializes. It’s a shame, because Anthropic’s superior model has helped it gain enterprise market share exponentially, riding on Claude Code and specific plugins—but that may not be enough for total success.

The conversation around AI is still being framed as a stock-picking game, and that is why the essential point is being missed. If we really are entering a world where production is automated first on the cognitive side and then on the physical side, the natural outcome is not just higher productivity, but a structural decline in marginal costs and, with it, strong deflationary pressure. And deflation does not just lower prices—it erodes revenue pools in real terms and turns “advantage” into a battle to retain some share of the corporate surplus. The fact that a company can produce something more cheaply does not mean it will capture that margin for years, because everyone else is also lowering costs, and competitive equilibrium forces prices down. The second-order effect is that if labor is displaced, the personal income tax base shrinks, and the State will need another source of funding to sustain the social contract, probably through some form of UBI. That pushes political pressure toward capital and, in practice, toward the few winners that concentrate cash flow. You could end up with a toxic combination of falling prices, compressed margins, and rising effective tax rates. The transition itself may be highly profitable because the market takes time to price in these dynamics, but the end state does not look like infinite profits—it looks like an environment where part of the surplus is competed away and part of it is taxed. It is a plausible scenario that would destroy and reshape the structure of the equity market as we know it.

The operation in Iran has become far more complicated, and unlike in Venezuela, it is not clear what the objective is or how it is supposed to be achieved. Operation Epic Fury began with several objectives:

Destroy and eliminate the regime’s missile infrastructure.

Destroy the Iranian navy.

Bring about regime change and the end of the nuclear program.

But after a week since it began, the path to achieving those goals no longer seems clear at all. Iran, while it does appear to be something of a paper tiger — that is, its ability to inflict major damage (in terms of human casualties, infrastructure, security, and so on) on its enemies is limited — has chosen to pursue a strategy of chaos and broader Gulf involvement, which could drag the conflict out significantly (think back to the Red Sea and the Houthis...) and create strong economic pressure to bring it to an end. The first thing to blow up has been the price of oil, which is already flirting with $100/bbl, something that seemed unthinkable just a few weeks ago, especially if we take into account that physical market fundamentals clearly pointed to a surplus. Right now, crude is expensive relative to fair value, but cheap relative to the tail risk if logistics seriously break down. Two key factors are coming together:

Iran is one of the world’s largest producers, and any disruption to its operations could alter the market balance in a very significant way.

The world’s main maritime artery for hydrocarbon exports, the Strait of Hormuz, has its narrowest passage right next to the country’s border, meaning that the threat of attacks or a blockade of traffic could also cause major disruptions to trade flows.

Iran, despite sanctions, had been producing practically at full capacity (around 3.55 mb/d), so the optionality is only to the downside for prices. If one strips out the noise, WTI should be closer to $60/bbl in a base-case scenario. But we are already close to $90. That gap is, quite literally, the price of uncertainty. And here the usual problem in commodities appears: when the risk premium compresses or normalizes, it does so quickly and without warning. That is why the return/risk profile gets worse and worse as WTI approaches $100. Producers, for their part, are hedging aggressively. After more than a decade of a bear market in oil, now that prices have finally rebounded, nobody in the sector is willing to stay exposed to the market taking that margin away from them overnight. But the interesting thing is that nobody is increasing capex. According to the latest U.S. production estimates, if WTI stays around $70/barrel, production could rise to roughly 14 million barrels per day. If WTI averages $80/barrel, it could reach a peak near 14.5 million b/d, but that would be close to the ceiling. That implies relatively limited additional growth, between 350,000 and 850,000 b/d compared with December 2025 volumes. It is not an especially aggressive expansion.

As for maritime traffic, even if there were no attacks — and in fact, a physical closure of the strait is highly unlikely — security risk alone is enough to deter navigation. If insurers cancel “war risk” policies (or refuse to renew them) for vessels transiting the Gulf and the Strait of Hormuz, the strait does not actually need to be “closed” for flows to slow. It is enough for the cost and availability of coverage to make transport operationally unviable for a meaningful portion of the fleet. In practice, that means fewer ships willing to load, more waiting days, more delays, and a rapid rise in freight rates and insurance premiums. The oil may exist, but it may not get where it needs to go on time.

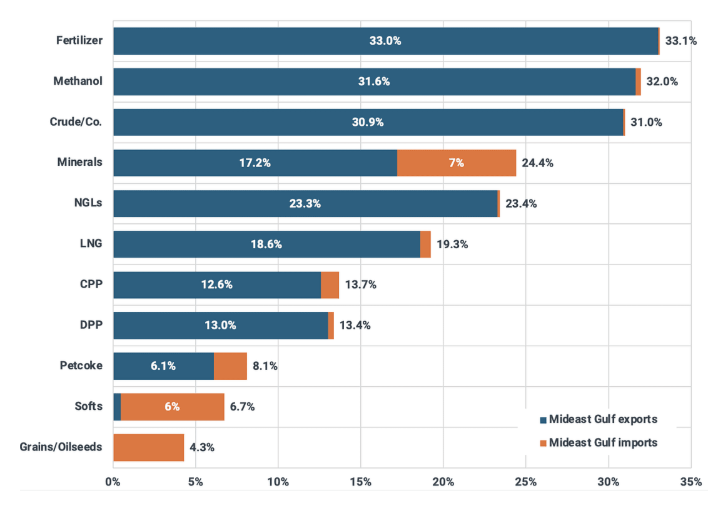

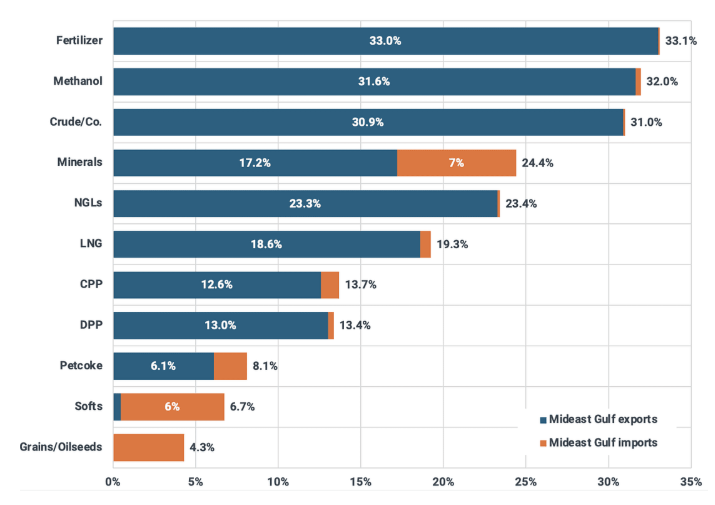

In the Iran disruption, everyone instinctively looks to oil, but the more interesting shock could end up coming through gas, and not through Europe and TTF, but through Henry Hub via LNG. It is important to understand that the Strait of Hormuz is a trade route of critical importance for a large number of commodities, and all of them are at risk of experiencing spikes like the one seen in oil.

So far, the consensus on U.S. gas had been clearly negative, with the heating season ending, inventories closing near the 5-year average, and the sense that 2026 is “well supplied.” On top of that, there is the whole set of arguments that has kept HH contained: fairly well-known structural LNG/Mexico demand with no major surprises expected until 2027, Lower 48 production still capable of growing, and a 2026 with more renewables that could once again reduce power burn if gas gets too expensive in the summer, in addition to the usual gas-to-coal switching when prices become too high. In parallel, the market had already been buying into the 2027–2030 narrative of a possible global LNG glut from new capacity, especially from Qatar, which in theory would limit growth in U.S. exports and put pressure on prices. Last weekend changed the variable that was not in the model: supply reliability. Qatar declaring force majeure on its production is a practical demonstration that LNG from the Middle East carries an interruption risk that buyers can tolerate when everything is normal, but not when there is sustained geopolitical tension. If the market moves into a regime where LNG shipping rates surge and the probability of disruption is no longer remote, the premium is not paid only in the spot price; it is paid in the kind of contract you want to sign and with whom. That is where the U.S. becomes the preferred supplier, not because it is the cheapest today, but because it is the most financeable and “insurable” in terms of country risk and continuity of flow.

On top of that, the U.S. starts with obvious advantages: it is already the largest exporter, shale producers still enjoy solid economics, and the Permian, because of its associated gas dynamics, can end up selling molecules at absurdly low prices or even negative prices during periods of congestion. That last point matters, because the market tends to think of HH as a standalone story, when in reality supply elasticity is constrained by infrastructure and by the relationship with oil. If the world is asking for more secure LNG, the bottleneck stops being just the resource itself and becomes capacity, contracts, logistics, and permits. The point is not that the U.S. will run short of gas tomorrow. The point is that the contract map may have shifted for years, and that is exactly the kind of change the market is usually slow to price in.

Model Portfolio

Year to date, the model portfolio is up +18.22%, versus +0.09% for the S&P 500 (S&P in euros), and +204.7% since inception (September 2022), compared with +50.4% for the S&P 500. The model portfolio, as of Friday's close, is as follows:

⚠️Past performance does not guarantee future results. The historical performance of the model portfolio is shown for informational and educational purposes only and does not constitute investment advice or an offer to buy or sell securities. The returns shown may not include fees, taxes, or other associated costs.