Disclaimer

LWS Financial Research is NOT a financial advisory service, nor is its author qualified to offer such services.

All content on this website and publications, as well as all communications from the author, are for educational and entertainment purposes only and under no circumstances, express or implied, should be considered financial, legal, or any other type of advice. Each individual should carry out their own analysis and make their own investment decisions.

Weekly macro summary

There have been quite a few interesting events to analyze this week, and below I list the most noteworthy news. Let’s get started:

Nationalization is back in fashion, and this time the target is not failed banks, electric utilities or strategic mines, but the major artificial intelligence companies. It is no longer just that Bernie Sanders is proposing that the state take 50% stakes in OpenAI, Anthropic and similar companies; Trump also appears to be exploring a similar idea. When two opposite political poles converge on the same point, it is usually a sign that the underlying consensus is changing.

The logic is that if AI is going to capture a huge share of future economic surplus, displace jobs and become critical infrastructure for national security, the state does not want to limit itself to regulating from the outside. It wants to participate in the capture of value. Sanders presents it as a way to socialize part of the benefits of a technology built on collectively generated data, knowledge and content. Trump frames it more as a partnership between companies and the American public, in line with his growing use of the state as a strategic shareholder. The precedent already exists. The administration took a 10% stake in Intel, as well as positions in rare earths and quantum computing companies. The difference is that applying this model to AI would have far greater implications, because these companies are not simple industrial suppliers, but potential central platforms of the future economy.

On the one hand, state ownership could reinforce the idea that these companies are too strategic to fail, reducing political risk and facilitating access to contracts, financing and infrastructure. On the other hand, it introduces a huge layer of uncertainty, with the politicization of governance, pressure on margins, possible limits on returns to private capital and the risk that the state increases its control over time. What begins as a minority stake can end up becoming a lever for intervention. We are entering a new phase of economic nationalism, where governments no longer trust the market to allocate capital neutrally in strategic sectors. Energy, semiconductors, uranium, rare earths, defense, quantum computing and now AI are all part of the same board. The underlying question is troubling: if artificial intelligence becomes infrastructure as essential as electricity, telecommunications or the financial system, will governments continue to treat it as a conventional private sector? Probably not. AI was born as a story of venture capital, technical talent and almost infinite scalability. It may end up looking much more like a strategic utility, with private shareholders, yes, but under ever greater state oversight and ownership. What worries me is the direction the United States has been taking lately… Who is John Galt?

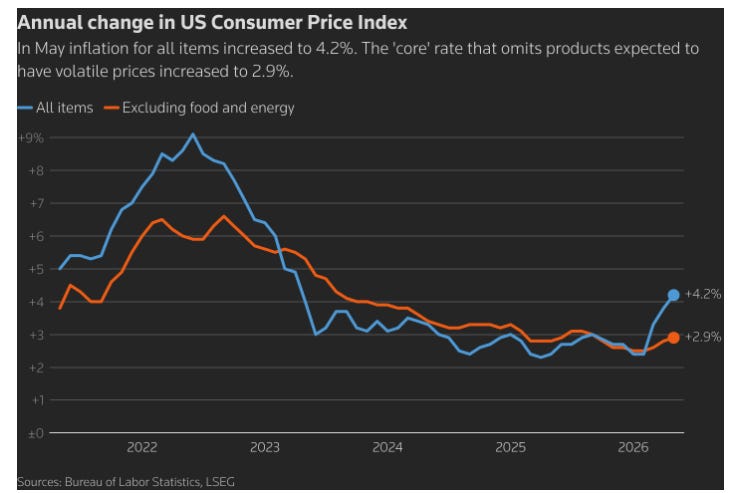

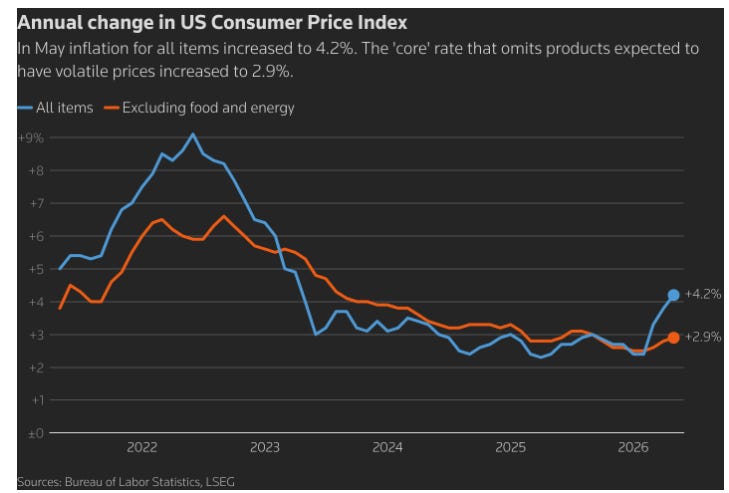

The May inflation data confirms that the normalization scenario many had expected is once again becoming more complicated. U.S. CPI rose 4.2% year-on-year, its fastest pace since April 2023, marking three consecutive months of strong price pressures. The main catalyst has been the energy shock caused by the conflict in the Middle East, with energy prices up 23.5% year-on-year and gasoline rising by more than 40%. In other words, this is not classic demand-driven inflation, but rather a renewed cost shock that puts the Fed back in an uncomfortable position. As a result, rate cuts are moving further away. The Fed will probably keep rates unchanged, but the important point is the shift in bias. Until recently, the debate centered on when monetary policy would begin to ease. Now, with oil under pressure, employment still resilient and headline inflation accelerating, the market is even starting to consider the possibility of further hikes, although the bar remains high. In practice, Powell does not need to raise rates to tighten financial conditions; he only needs to remove any expectation of cuts.

The key nuance is that core inflation remains much more contained than headline inflation. Core CPI rose 2.9% year-on-year and only 0.2% month-on-month, suggesting that, for now, the energy shock has not broadly filtered through to the rest of the basket. It also seems that the impact of tariffs is beginning to fade in goods, with declines in furniture, new vehicles and core goods. This reduces the urgency of an immediate hike, but it does not eliminate the problem. If energy remains elevated for longer, as we believe it will, the risk of second-round effects increases: transportation, airfares, fertilizers, food, services and inflation expectations.

For households, the data is more worrying than it is for macro models. Real wages fell for the second consecutive month, which explains why economic discontent is not merely a matter of perception. Inflation is once again eating into nominal income growth, especially for middle- and lower-income families. If consumption remains resilient, it is partly because households are still drawing on savings, a dynamic that cannot be sustained indefinitely. Politically, the data is dynamite. Trump won by promising to bring inflation down, but this renewed spike hits him just ahead of the November midterm elections. His response, saying that he “loves inflation” and that it will fall like a rock once the war with Iran ends, captures the problem well: the White House wants to frame the rebound as temporary and external, but voters do not pay for gasoline or groceries in terms adjusted for geopolitical narratives. They pay nominal prices.

SpaceX is coming to market in the middle of a technological storm, but it is doing so with demand bordering on the absurd, with more than $350 billion in indicative orders for a deal seeking to raise $75 billion. A 4-4.5x oversubscription which, beyond the headline number, confirms that appetite for the great private winners of the past decade remains intact, even in an environment of extreme volatility, sharp Nasdaq declines and bitcoin trading 37% below its highs.

SpaceX is probably the most coveted private asset in the world, with a unique combination of leadership in space launches, Starlink as a global connectivity business and a narrative of almost unlimited future optionality. The company is selling the market something far more ambitious than rockets or satellite internet: the possibility of building critical infrastructure beyond Earth, including data centers in orbit to solve the energy and computing bottlenecks of artificial intelligence. It is an incredibly powerful story, almost inevitably designed to capture capital in a cycle obsessed with AI.

But that is precisely where the risk lies. The presentation talks about a $23 trillion opportunity in artificial intelligence, supported by the idea that SpaceX can escape the physical limitations of terrestrial infrastructure. It is a brilliant narrative, but also a very demanding one. The market is not only valuing the current business, but a promise of dominance across several industries that have yet to fully materialize: launches, connectivity, defense, space computing and AI. In this way, with little tangible yet but enormous potential TAMs, it becomes much easier to sell both the idea and the valuation.

Massive institutional demand does not eliminate valuation risk. In fact, it often amplifies it. Buying pressure can become so strong that it distorts the market in the short term, and some analysts have even suggested that part of the recent weakness in risk assets could be related to selling in order to fund allocations to SpaceX. If that is true, this would be a deal capable of absorbing liquidity from across the entire technology ecosystem. The company probably deserves a premium over almost any traditional listed company. That is not the question. The question is how much future can be priced in before even an exceptional company has to prove it in the numbers.

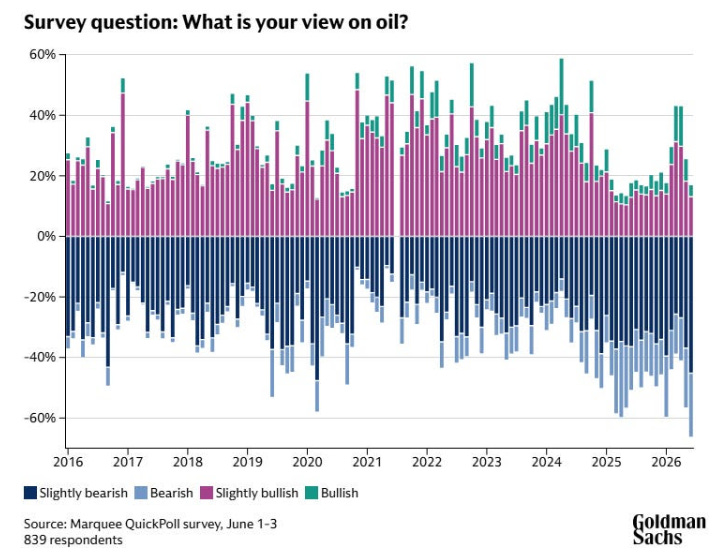

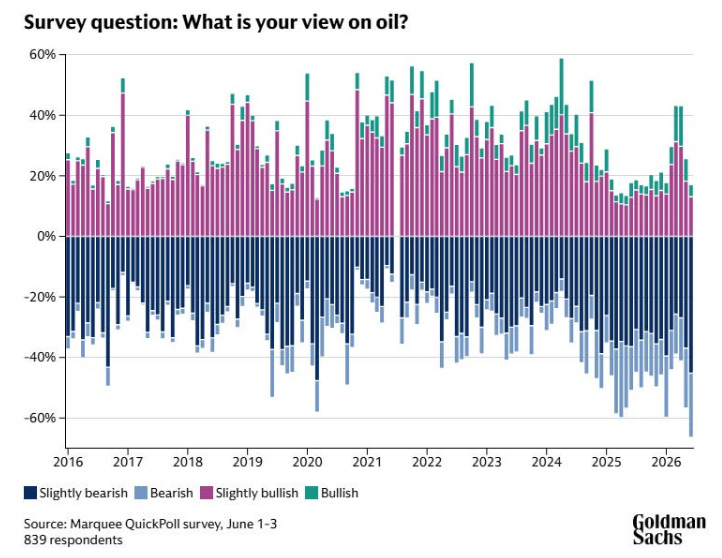

Positioning in oil remains extraordinarily attractive precisely because the consensus still fails to understand the basic arithmetic of the physical market. The survey shared this week by Goldman is almost a gift for anyone with a bullish view on crude, not because it provides new information, but because it confirms just how complacent the market still is. If onshore inventories are being drained at the fastest pace in history and there are still investors convinced that there is no supply problem, then the bearish narrative has not yet been purged. In fact, positioning is the most bearish ever recorded.

The confusion comes from looking only at the price of WTI. Because it is trading around $84, already far from the $100 seen just two weeks ago, many conclude that there cannot be a shortage. It is the classic mistake of extrapolating from the financial screen to physical reality. The price still does not fully reflect the tension because part of the adjustment has shifted from crude to refined products, and because governments have temporarily softened the shock through releases from strategic reserves. But that does not change the nature of the problem. What was once an obvious crude shortage has turned into a product shortage. China has restricted exports of refined products, independent refiners have stopped flooding Asia with cheap supply, and plants without sufficient access to crude have reduced throughput to preserve inventories. At the same time, SPR releases have artificially softened the crude market, shifting part of the pressure downstream.

The balance, in reality, remains very tight. Millions of barrels per day of production have been lost, and although part of that impact is offset by lower refining activity, reserve releases and inventory drawdowns, the lost barrel does not disappear from the math. If product inventories continue to fall globally and there is no COVID-style demand destruction, the deficit is still there. Whether it shows up in crude or refined products is more of an accounting distinction than an economic one. The important signal is that the market has managed to convince itself that there is no shortage. Even many oil traders seem to have accepted the idea that if the price has not exploded, the problem does not exist. But in commodities, the opposite is often true: the best setups appear when the consensus looks at the price, ignores inventories and underestimates the physics of the system. Here, complacency is not a risk to the bullish thesis; it is a central part of the opportunity.

Model Portfolio

Year to date, the model portfolio is up +24.86%, versus +10.75% for the S&P 500 (S&P in euros), and +221.9% since inception (September 2022), compared with +66.4% for the S&P 500. The model portfolio, as of Friday's close, is as follows:

⚠️Past performance does not guarantee future results. The historical performance of the model portfolio is shown for informational and educational purposes only and does not constitute investment advice or an offer to buy or sell securities. The returns shown may not include fees, taxes, or other associated costs.