Disclaimer

LWS Financial Research is NOT a financial advisory service, nor is its author qualified to offer such services.

All content on this website and publications, as well as all communications from the author, are for educational and entertainment purposes only and under no circumstances, express or implied, should be considered financial, legal, or any other type of advice. Each individual should carry out their own analysis and make their own investment decisions.

Weekly macro summary

There have been quite a few interesting events to analyze this week, and below I list the most noteworthy news. Let’s get started:

The truce between the U.S. and Iran is once again on the verge of breaking down, although this comes as no surprise to us. The American proposal sought first to freeze the fighting and leave the more complex issues — the nuclear program, sanctions, security guarantees — for later. But Tehran’s response goes much further: an end to the war on all fronts, including Lebanon; compensation for damages; the lifting of the naval blockade; non-aggression guarantees; the reopening of oil sales; and recognition of its sovereignty over the Strait of Hormuz. In other words, unacceptable without an acknowledged humiliation on the part of the United States.

It is a maximalist position, but not an irrational one from Iran’s perspective. Tehran knows that its main leverage is not on the conventional battlefield, but in the energy market. Keeping Hormuz practically closed amounts to applying direct pressure on crude prices, American inflation, and Trump’s electoral calendar. With Brent above $109 and only a trickle of tankers passing through the strait, Iran is turning its military weakness into economic bargaining power. The problem for Trump is that the war is beginning to carry a visible domestic cost. Two out of three Americans believe he has not clearly explained the objectives of the intervention, and the rise in gasoline prices is arriving at the worst possible political moment, less than six months before key legislative elections. The administration can tighten sanctions, pursue Iranian crude shipments to China, or threaten to break the truce, but every day that Hormuz remains blocked increases the pressure on the American consumer and on the political credibility of the White House.

Moreover, Washington is still failing to build a solid international coalition. NATO allies do not want to send ships to reopen the strait without an international mandate and a broader peace agreement. The regional dimension is also becoming more dangerous, and according to The Wall Street Journal, the UAE has reportedly carried out attacks against Iranian targets, including a refinery on Lavan Island. Until now, several Gulf allies had tried to move cautiously, aware that they are vulnerable to Iranian retaliation. A more direct UAE involvement would open a new phase of the conflict, with a greater risk of horizontal escalation across energy, infrastructure, and maritime routes.

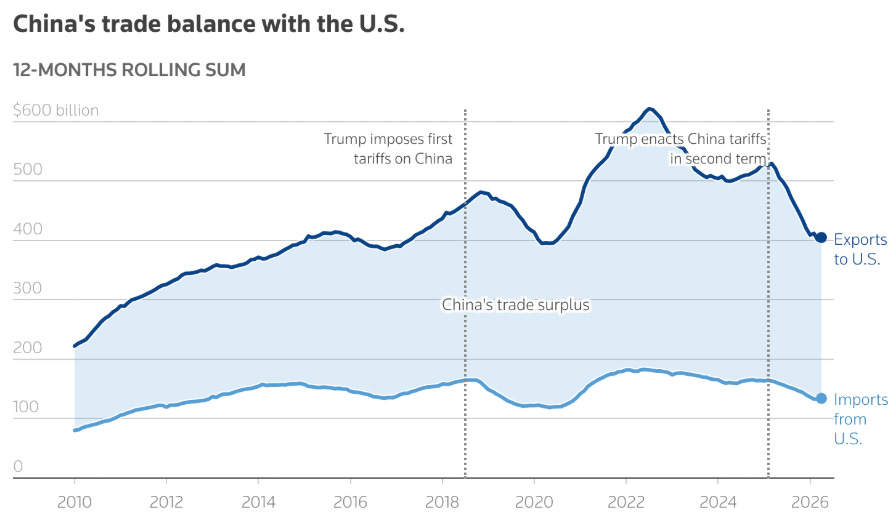

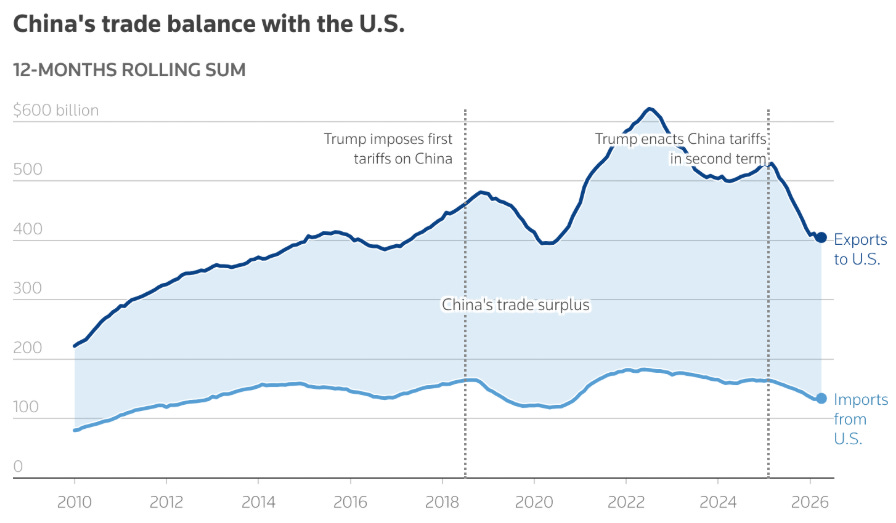

Trump’s visit to Beijing comes at a particularly delicate moment for U.S.-China relations, and it can be described as a total failure relative to the expectations that had been created. After last year’s clash, it was an attempt to stabilize a relationship that has become the central axis of the new geopolitical order: trade, critical minerals, Taiwan, AI, nuclear weapons, Russia, and Iran. Everything now runs through Washington and Beijing.

On the most tangible side, both countries seemed willing to announce mechanisms to facilitate trade and investment, as well as Chinese purchases of Boeing aircraft, agricultural products, and U.S. energy. This is the kind of agreement Trump understands well: visible headlines, American exports, industrial jobs, and a narrative of negotiating victory. The extension of the rare earths truce was also discussed, probably the most important point from a strategic perspective. China still controls a critical part of the global supply chain for essential minerals, and Washington needs to buy time while it tries to rebuild domestic capacity and diversify supply. The dependency remains, even if it is politically dressed up as an “agreement.”

But the truly relevant part lies in the difficult issues. Iran has become a central piece, since China is one of the main buyers of Iranian crude and therefore a key source of financing for Tehran. Trump wanted Xi to use that leverage to pressure Iran toward an agreement that would end the conflict that began after the U.S. and Israeli attacks in February, but the Chinese president offered no concession in that regard.

Taiwan will once again be the most structural point of friction. Beijing considers the island part of its territory and has intensified its military pressure in recent years, while Washington remains its main international backer and arms supplier. The Trump administration insists that its policy will not change, but the risk of miscalculation rises when both powers mix military rivalry, technological pressure, and domestic politics. It is the kind of tension that is not resolved by a summit; it can only be managed.

Meanwhile, after all the theatrics around last year’s tariffs, the trade deficit remains enormous, and it does not look likely to shrink much further.

In that sense, the trip has been an absolute failure for the United States from a strategic point of view, as it leaves without any major agreement, headline, or help on the Iranian front, where much of its hopes had been focused.

Inflation is once again complicating the macro picture in the United States. April CPI rose 0.6% month-on-month and accelerated to 3.8% year-on-year, the largest increase in three years, with a composition that is particularly uncomfortable for both the Fed and the White House: energy, food, and services all pushing higher at the same time.

The immediate cause lies in the energy shock triggered by the U.S.-Israel war with Iran. Gasoline rose another 5.4% after March’s record jump, diesel and other fuels advanced 17%, and energy accounted for more than 40% of the index’s monthly increase. The problem is that this no longer appears to be limited to the gas pump. Disruptions in the Strait of Hormuz, higher transport costs, and pressure on fertilizers threaten to spill over into the rest of the basket in the coming months. Moreover, for the first time in three years, prices are once again rising faster than wages, eroding real income and helping explain the deterioration in consumer sentiment.

Core inflation does not offer much relief either. Excluding energy and food, CPI rose 0.4%, the largest increase since January 2025. Part of the rebound is explained by a technical adjustment in rents after data collection problems during the government shutdown, but even so, the signal is clear: services inflation is still alive. With the labor market still solid and inflation once again moving away from target, the room for rate cuts disappears. In fact, the market is starting to assume that rates could remain in the current 3.50%-3.75% range until 2027.

Politically, the blow to Trump is obvious. His 2024 victory rested on the promise of reducing the cost of living, but the geopolitical conflict and rising energy prices have brought inflation back to the center of the debate just before the midterms — and the worst part is that this is a self-inflicted problem. The proposal to temporarily suspend the federal gasoline tax may ease the immediate pain somewhat, but it does not change the root of the problem, and stimulating demand in the face of a supply shock is a textbook example of what should never be done. Against such a complicated backdrop, Warsh takes over from Powell at the head of the Fed, facing a historic challenge with no clear solution in sight.

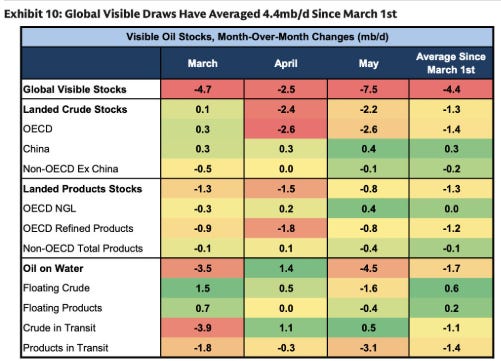

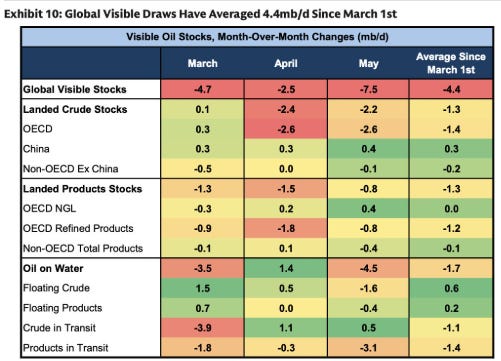

The oil market is entering a much more delicate phase than many analyses focused solely on “counting barrels” would suggest. The main idea is simple: the buffer has already been exhausted, and the damage has been done. First, the excess oil on water and floating storage disappeared; from now on, any further deterioration will have to show up as a visible decline in crude inventories, refined product inventories, or, ultimately, demand destruction. And that last part does not yet appear to be happening.

When refineries start running out of available crude in storage, their first reaction is not to shut down abruptly, but to try to protect throughput by buying more barrels in the physical market. That urgency translates into more aggressive backwardation in the front-month contracts. In other words, the market rewards the barrel available today far more than the barrel available in the future. That is why timespreads should remain strongly backwardated as long as the shortage is concentrated in physical crude rather than in a simple financial dislocation.

The natural consequence is that refining margins remain elevated. If the constraint is in crude, the regions with less access to sufficient inventories will have to pay more for the raw material, but they will also be able to pass that pressure on to refined products. Asia is the most vulnerable point: if its refineries cannot access the crude they need, they will begin importing more refined products. That additional demand from the East will pull margins higher in the West, first in Europe and then in the United States, incentivizing Western refineries to maintain or even increase throughput.

This process can feed on itself for some time. As Asia imports products, inventories of gasoline, diesel, and other refined fuels in Europe and the United States will fall quickly, perhaps within a matter of weeks. Western refineries, seeing better domestic prices, will have incentives to keep products in their own markets. Asia would then not only have a crude problem, but also a refined products problem. At that point, Asian margins could take another leg higher, allowing refineries to bid much more aggressively for any available physical barrel.

It seems that even the IEA, always so negative on crude, is now forecasting a deficit that will last at least until Q4, and probably beyond. That has very relevant implications not only for prices this year, but also for future years, given the pressure it places on inventories.

A few analysts, still not many, are already daring to put numbers on the physical reality we are observing and the consequences that follow from it. One example is Piper Sandler, which is now forecasting Brent above $100 for all of this year and next. Higher for longer.

Model Portfolio

Year to date, the model portfolio is up +21.9%, versus +9.77% for the S&P 500 (S&P in euros), and +214.2% since inception (September 2022), compared with +64.9% for the S&P 500. The model portfolio, as of Friday's close, is as follows:

⚠️Past performance does not guarantee future results. The historical performance of the model portfolio is shown for informational and educational purposes only and does not constitute investment advice or an offer to buy or sell securities. The returns shown may not include fees, taxes, or other associated costs.