Weekly summary 26/04

He said, she said

Disclaimer

LWS Financial Research is NOT a financial advisory service, nor is its author qualified to offer such services.

All content on this website and publications, as well as all communications from the author, are for educational and entertainment purposes only and under no circumstances, express or implied, should be considered financial, legal, or any other type of advice. Each individual should carry out their own analysis and make their own investment decisions.

Weekly macro summary

There have been quite a few interesting events to analyze this week, and below I list the most noteworthy news. Let's get started:

Tensions between the White House and the Federal Reserve have been a constant in recent years, and the rift between President Trump and Jerome Powell, whom he himself appointed in 2018, has resurfaced. The clash between Donald Trump and Jerome Powell has escalated to levels rarely seen between a president and the Fed chair. Powell’s refusal to cut rates under current conditions has led Trump, in his usual style, to intensify his public attacks and even reopen the possibility of firing him. Although the legal framework is not entirely clear, the mere suggestion of such a scenario creates an institutional uncertainty that is hard to overstate.

With costs dropping so well, as I predicted would happen, there almost cannot be any inflation, but there can be a SLOWDOWN of the economy, unless Mr. ‘Too Late,’ a major loser, cuts interest rates, NOW.

— Donald TrumpThe Federal Reserve Act states that governors can only be removed “for cause,” traditionally understood as misconduct rather than political disagreement. However, the law is silent on the specific limits regarding the removal of the Chair — a legal ambiguity that, in the hands of this administration, could open the door to an unprecedented conflict.

If Trump attempted to remove Powell as Chair but not as a governor, Powell would remain on the Board until 2028, and Trump could only appoint a new Chair from among the six current governors, two of whom were appointed by him. But even these — Waller and Bowman — have publicly defended the institution’s independence.

The more aggressive path, removing him as a governor, would trigger an institutional rupture of such magnitude that it would immediately be taken to the federal courts. Although Powell has the means to legally defend himself, even attempting it would seriously damage the Fed’s credibility and its already battered independence after Trump’s relentless attacks.

For now, it seems that some close advisers — including Kevin Warsh, a possible successor — have tried to restrain this impulse. But the fact that Trump is seriously considering this option confirms that his approach to monetary policy is not based on macroeconomic stability but on political control of key financial levers. The Fed remains one of the last independent institutions still standing. Its future, like that of the markets, hangs by an increasingly fragile thread.

There is often a perceived correlation between the Nasdaq and Bitcoin, and due to the former’s current weakness, a drop in the latter is also predicted; however, in reality, the correlation is not with the QQQ, but with global liquidity (which, of course, also affects the indices). In this sense, in recent months we have seen a sharp surge in M2. The following chart relates both dimensions (with a lag in the monetary mass) and shows the path I believe the crypto asset’s price will follow, culminating in a peak that could mark the end of this successful cycle in the summer.

After a few difficult weeks for the markets (following Liberation Day), Bitcoin’s price showed remarkable resilience, holding up well during the downturns and rebounding strongly now as the market recovers somewhat. In fact, even on the worst days when all correlations spiked to 1 and many funds and investors sold whatever they could, Bitcoin ETF outflows remained very moderate. Now, the trend has reversed, and capital has been flowing back in at a rapid pace, erasing all of the month’s outflows by a wide margin: $3.1 billion over the past 7 sessions and 33.5k BTC acquired (compared to 3.15k BTC mined this week).

Michael Saylor also remains deeply engaged in his personal crusade, accumulating Bitcoin week after week. His strategy and company are often ridiculed or even labeled as a fraud, but my honest opinion is that it will be successful and will turn a company with a worthless business into one of the largest corporations in the world — simply for having been an early visionary and consistent in execution.

Not everything is about improving fundamentals — the speculative spirit is also making a comeback in the sector. The president’s memecoin surged 65% after it was announced that the top 220 holders would have the chance to dine with the him. Far from helping attract serious new users, this kind of news deters any serious investor from taking the sector seriously — and it is even more concerning when promoted by the president of the world’s leading power...

The economic success of Javier Milei and his team in transforming Argentina is now undeniable. The economy grew by 0.8% month-over-month in February, and the level of activity is already the highest since May 2022. Except for that month (which will be surpassed and adjusted in March), economic activity in Argentina is now higher than at any other time during the previous administration. In fact, the IMF expects a 5.5% year-over-year real growth for the country.

Beyond the data, the government (a rare sight) is delivering on its promises, having already (partially) lifted currency controls and progressively cutting regulations and taxes. So far, energy exports have been one of Milei’s biggest allies, and now agricultural production could also join as a major support. The Buenos Aires Grain Exchange, which was already forecasting a record wheat harvest for Argentina in 2025/26, could further raise its estimates if the temporary cut in export taxes is extended beyond June. The current estimate of 20.5 million tonnes —already the second-largest in history— assumes a return to a 12% export tax starting in July. If Milei, under pressure from the agricultural sector, decides to extend the tax relief, we could be looking at a historic campaign. It’s worth remembering that in January, the government temporarily reduced wheat export taxes from 12% to 9.5% in an effort to boost foreign sales and bring in foreign currency, although Milei has insisted there will be no extension. However, political pressure from the agricultural sector and the new floating exchange rate —which weakens the peso and improves export incentives— could reopen the debate. In any case, the possibility of a "super harvest" of wheat adds another positive catalyst for the Argentine economy, which is increasingly dependent on agriculture as a source of fresh dollars.

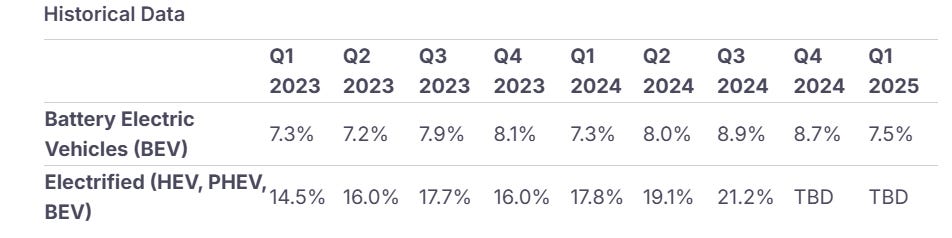

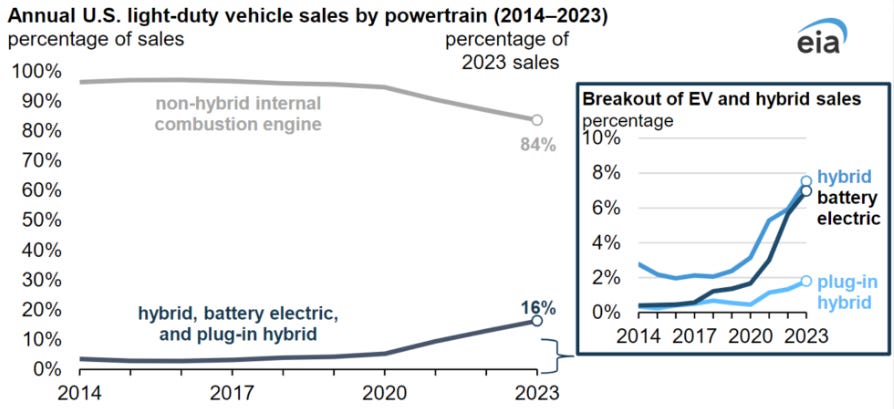

The adoption outlook for purely electric cars has been greatly exaggerated in recent years; as often happens with the arrival of a new technology, initial expectations and projections are overstated and, over time, are adjusted to reality (e.g., what happened with non-combustible products in tobacco companies in 2017). In this case, a rapid decline in sales and market share of internal combustion engine (ICE) cars was expected, along with their replacement by purely electric vehicles. Although we have explained on several occasions why this is impossible and why, in its current form, it is not a scalable technology, it is always good to confirm it with data. The market penetration of purely electric vehicles (BEVs) in new car sales is currently stagnant, whereas hybrid car sales are growing significantly.

Prior to 2023, BEVs showed a higher growth rate, but this now seems to have stalled in favor of the convenience and user experience offered by hybrid vehicles.

Why is this important to us? For two reasons:

It extends the terminal value of many oil companies and alters the sector’s balance sheet projections.

Hybrid cars use a higher amount of PGMs (Platinum Group Metals) than ICE vehicles, making this trend crucial for this investment thesis as well.

Bessent came to the market’s rescue this week. In a closed-door meeting, he confirmed what everyone already knows: the current tariff situation with China is unsustainable. The United States and China remain locked in a trade tug-of-war with no clear end in sight. Despite Donald Trump’s ambiguous statements —claiming there are ongoing meetings but refusing to name anyone— the signals from Beijing (for public consumption) are clear: China is in no hurry. Trump may say he is “ready for a deal” or that he “doesn’t need one,” but China’s response, for now, is cold silence.

Trump has raised tariffs on China to as much as 145%, in an escalation that Beijing has mirrored step by step —without yielding ground or showing any urgency to negotiate. Meanwhile, the U.S. president continues to insist that a full trade agreement could take 2 to 3 years to materialize, and that formal negotiations won’t begin anytime soon. It feels like a game of telephone, where institutional mistrust has become so normalized that we no longer know who to believe.

In parallel, Trump is sharply criticizing China’s treatment in multilateral organizations, calling it absurd that the World Bank still classifies it as a developing country, and demanding reforms both at the IMF and within China’s economic policy, directly targeting the need to move away from an export-led growth model and focus on domestic demand. Meanwhile, on the sidelines of the IMF and World Bank meetings, U.S. officials like Treasury Secretary Scott Bessent are trying to sell a narrative of rapid progress in bilateral deals —though privately, many Finance Ministers remain far more skeptical, warning about the growing risks to global growth and employment.

At the same time, and showing that they’re not immune to the conflict, China has begun exempting some U.S. products (such as pharmaceuticals) from the retaliatory 125% tariffs, suggesting a faint gesture of de-escalation, though without any clear agreement structure. Trump, for his part, has boasted of “200 deals” supposedly set to be finalized within weeks —but without offering details.

The market, hungry for any positive signal, managed to close the week in the green. But the damage has already been done: since Trump’s return to the White House, U.S. indices are down nearly 10%, the dollar is plummeting at unprecedented rates, and recession risks are growing on the horizon. Meanwhile, the EU and Asia have weathered the storm more effectively, fueling the perception that the United States is not only losing the trade war, but also isolating itself strategically.

The IMF has already downgraded its growth forecasts and, while global progress is expected, it would come at the slowest pace since the pandemic.

U.S. PMIs, for now, remain in expansion territory —but confidence is deteriorating rapidly, and unless there are some agreements that clarify the outlook and provide short-term stability, we could soon enter contraction territory.

This week we had one of the best U.S. inventory reports in recent months, further reinforcing our view that the market narrative is wrong. Let’s dive into the data (the EIA's weekly report, besides inventory numbers, includes a lot of demand information). Seasonally, oil demand in the U.S. this week is the highest on record, which starkly contrasts with the market sentiment.

Not only that, but implied production was 12.85 million barrels per day — almost 800,000 barrels per day less than what the agency’s models project! Looking at how product inventories have behaved, the idea of a large crude surplus or severe demand weakness quickly falls apart.

Here’s a table (h/t Gugo907) that compares, for week 16 (seasonality is crucial in crude oil), the inventories of the main products over the last 7 years and the associated crude price. It’s quite surprising.

Despite these fundamentals, which while not extraordinary are moderately positive, the market continues to react to headlines. This time, it's the problems within OPEC and its internal cohesion. Discipline within OPEC+ is visibly crumbling. Kazakhstan’s Energy Minister has made it clear that national interests outweigh any commitment to the cartel: Kazakhstan cannot reduce production in its older fields without causing irreversible damage, nor can it impose cuts on the major oil companies operating in its territory.

This is no minor detail: it means there is no realistic scenario in which Russia, the United Arab Emirates, Kazakhstan, or Iraq will offset the current overproduction. The lack of compliance is structural, not circumstantial.

Once the Saudis label a member as a “cheater,” there is no going back. Trust — which was the glue holding OPEC+ together — breaks, and with it, the cartel’s ability to effectively coordinate the oil market.

Model Portfolio

The model portfolio's return is -8.17% YTD compared to -5.76.% for the S&P500 (our portfolio mesured in € terms, which is weighting -10% in our portfolio this year vs the S&P in $), and +53.9% versus +36.3% for the S&P500 since inception (September 2022). The model portfolio, as of Friday's close, is as follows:

Keep reading with a 7-day free trial

Subscribe to LWS Financial Research to keep reading this post and get 7 days of free access to the full post archives.