Weekly summary 29/06

Weekly summary 29/06

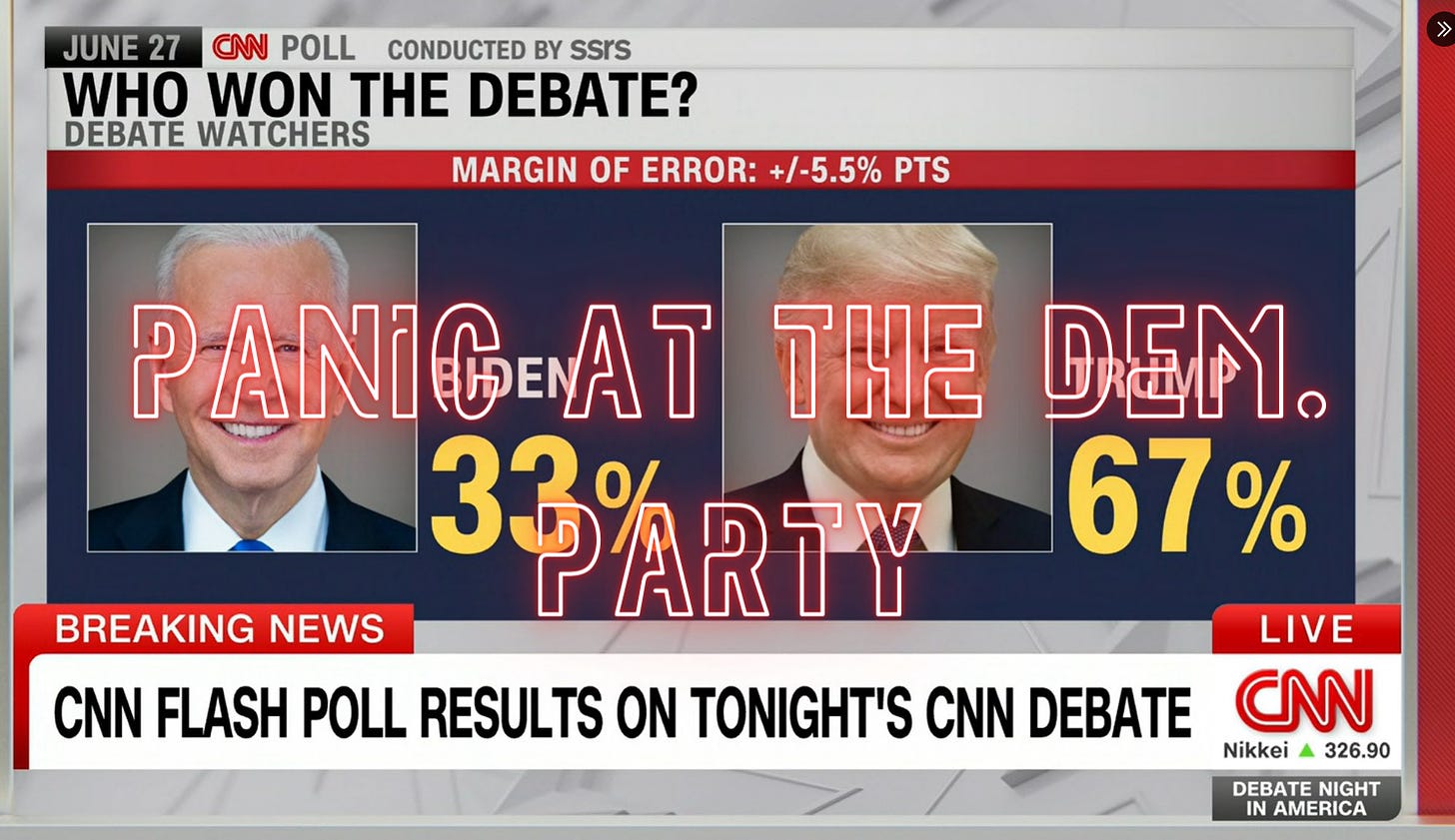

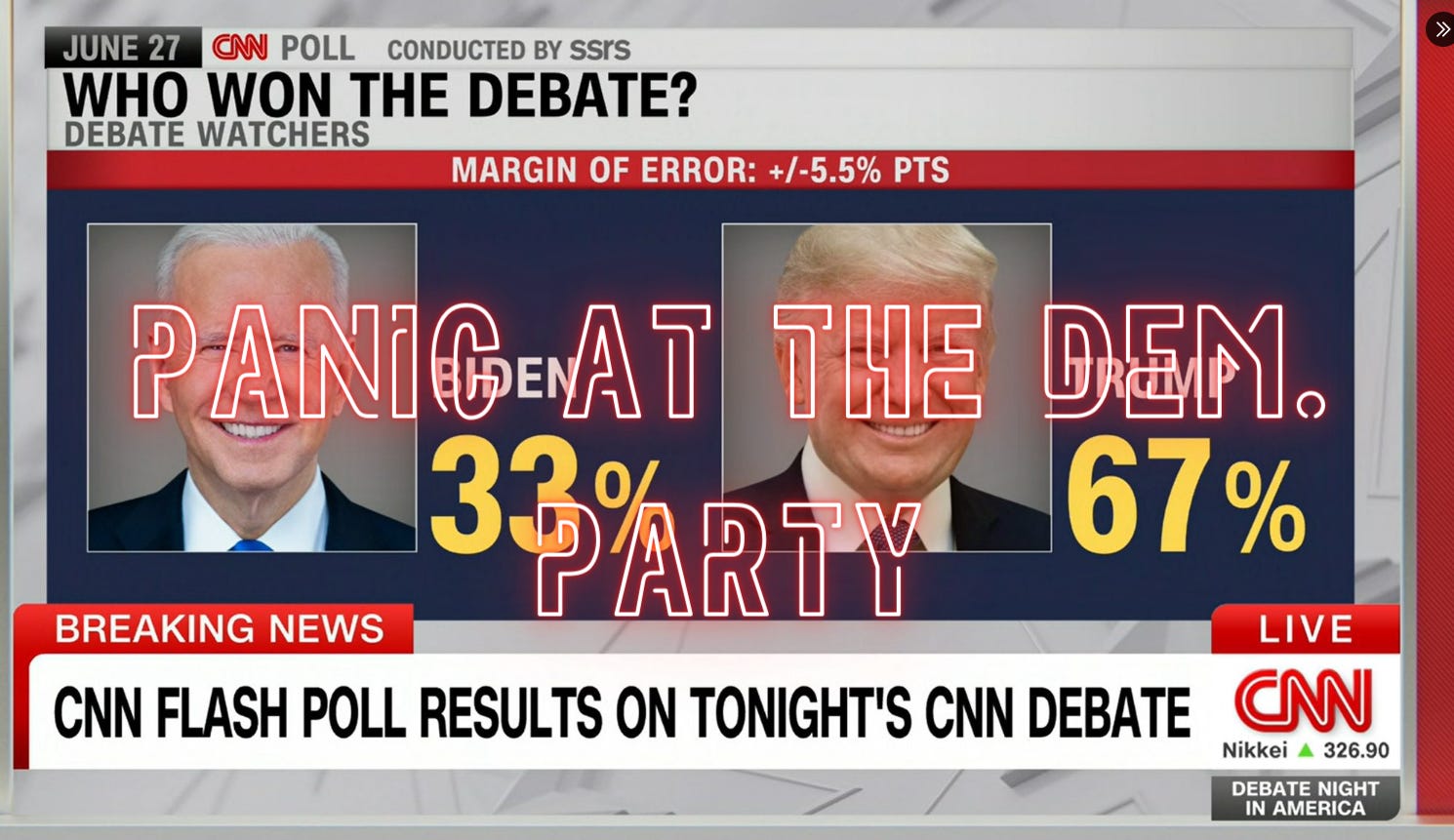

Panic at the Democratic Party

Disclaimer

LWS Financial Research is NOT a financial advisory service, nor is its author qualified to offer such services.

All content on this website and publications, as well as all communications from the author, are for educational and entertainment purposes only and under no circumstances, express or implied, should be considered financial, legal, or any other type of advice. Each individual should carry out their own analysis and make their own investment decisions.

Today we have the first edition of the in-person event by LWS Financial Research, a gathering space for our paying subscribers to strengthen the personal relationships that are being built day by day through conversations and debates on Discord. The community is a cornerstone at LWS Financial Research, enabling us to combine shared knowledge from many experts and minds to push further in our research, test our ideas, discover new ones, and provide support that makes this (often solitary) journey much more manageable.

We will continue to foster and promote initiatives like this from our end, and I hope this is just the beginning of what is yet to come.

Weekly macro summary

There have also been quite a few interesting events to analyze, and below I list the most noteworthy news. Let's get started:

The electoral debate on Thursday was a real nightmare for the Democratic Party. The feeling left among the listeners was that Biden is no longer capable of exercising leadership of the world's largest power, and although Trump's performance was not stellar either, the contrast in physical and cognitive capacity between both candidates is immense. If any voter still hadn't made up their mind about their vote, their choice is now clear.

Right now, there is a deep, a wide, and a very aggressive panic in the Democratic Party. It started minutes into the debate, and it continues right now. It involves party strategists and involves elected officials. It involves fundraisers, and they're having conversations about the President's performance, which they think was abysmal, which they think will hurt other people down the party on the ticket. They're having conversations about what they should do about it. Some of those conversations include: Should we go to the White House and ask the president to step aside? Should prominent Democrats go public with that call?

The re-election chances for Biden are virtually nil, and there are even doubts about whether he is capable of completing his term in office. Speculation, in fact, now focuses on whether it's actually a strategy of the party to replace the current president as a candidate: the swiftness and consensus in the reactions from Democratic politicians and political commentators about the need to replace the candidate suggest a kabuki theater act, with the debate as justification for what is about to happen.

Beyond the uncertainty about the technical feasibility of replacing Biden (he would need to step aside voluntarily), there would also need to be convincing Kamala (her poll numbers are abysmal) and finding a new partner... Newsom? After the California disaster, it's impossible for him to win nationally. Dimon? I don't think he wants to burn his political capital in this delicate situation. Hillary? Again? The Democratic Party now faces a complicated situation, and we will see if it's insurmountable.

Trump will not have an easy road ahead, with the growing fiscal deficit as the first hurdle for the long-term viability of the country and its position as a hegemon. The current competitiveness and demographics of the West are not compatible with the necessary economic growth to sustain this policy of continuous and increasing deficit. If these two fronts are not addressed, the only solution is containment of spending and the (likely) associated decline in quality of life, or the slow demise of the fiat system in these countries.

Luckily, for both, the Core PCE data (one of the main inflation measures) published on Friday were very positive, showing a downward trend and already very close to 2%. In fact, the monthly change would have been negative if it weren't for the significant rise in medical insurance costs.

Europe's largest renewable energy producer, Statkraft, is scaling back its expansion plans due to falling electricity prices and rising costs (sorry, there is no Moore's Law applicable here). Now, it plans to install 2-2.5GW annually of onshore wind, solar, and battery storage from 2026, instead of the previously planned 2.5-3GW from 2025 and 4GW from 2030. It has also reduced its offshore wind energy target to 6-8GW by 2040, down from the previous 10GW.

Despite the political push to increase renewable energy capacity, market realities have slowed these plans. Projects have become more technically complicated, and returns are insufficient, affecting the pace of the energy transition. Other European companies, such as Ørsted and EDP, have also reduced their targets due to market difficulties and economic conditions. This trend has been observed for some time, with companies like Siemens Gamesa openly acknowledging the economic viability issues of this technology, and investors turning away from a sector that has not delivered the promised returns.

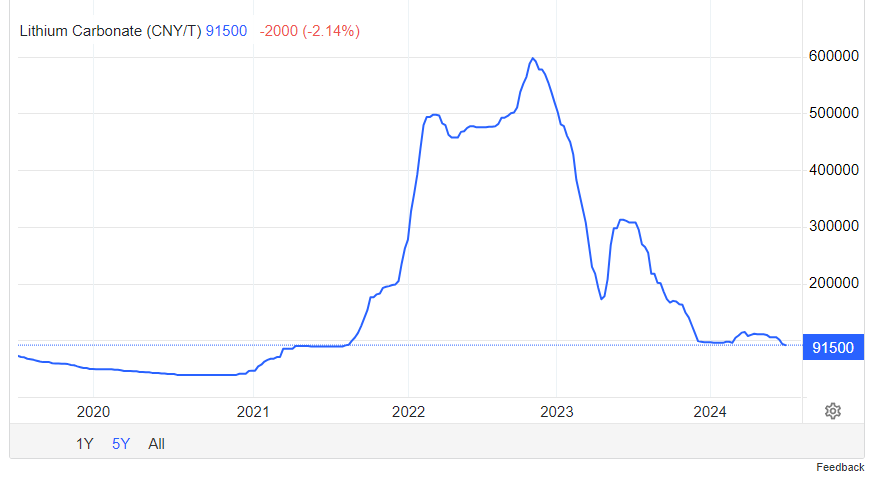

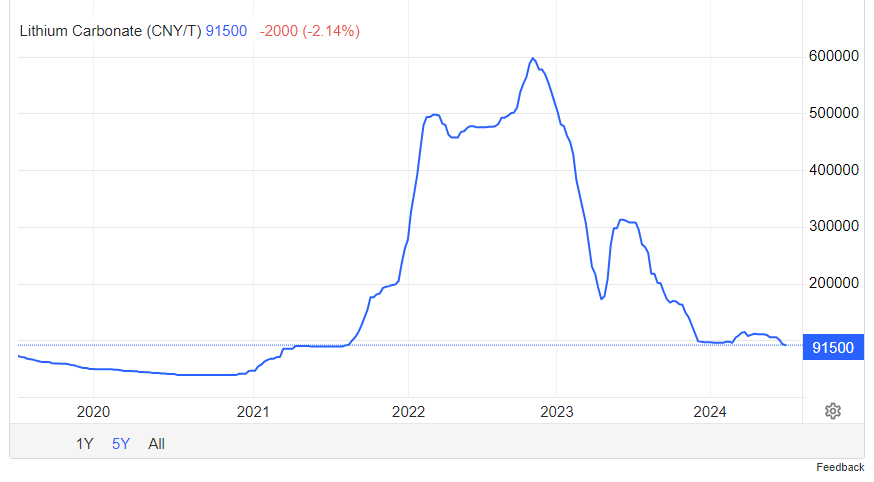

Some of the main winners of the last two years, like lithium, have returned to their starting point after an accelerated capital cycle, reaching prices that cannot incentivize new supply (according to Albemarle, one of the largest companies in the sector), which, on the other hand, is not needed right now. The conditions and environment for this metal and the major ESG champions seem to have found a certain floor, and we will see if they rebound during the next cycle of loose monetary policy towards which we seem to be heading.

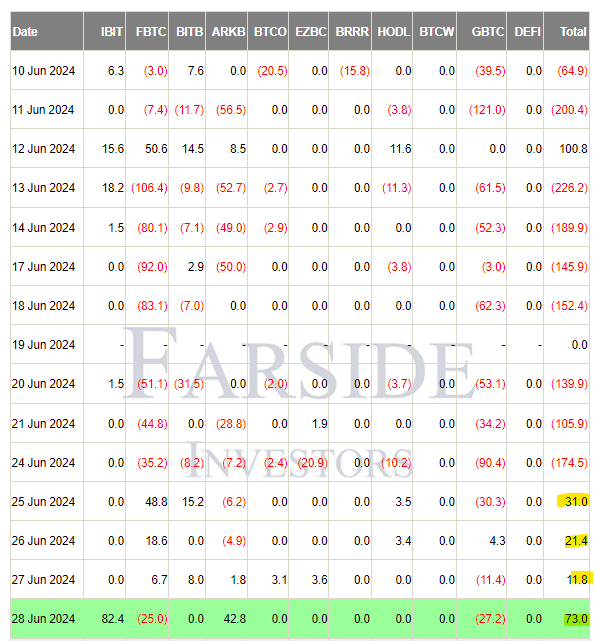

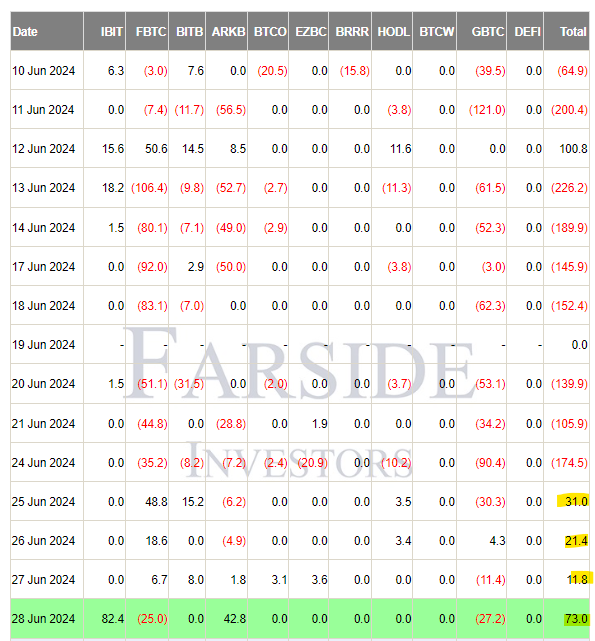

Barring any surprises, Ethereum ETFs will be approved and begin trading the week of July 8th (they were expected next week, but last-minute comments from the SEC and the July 4th holiday have postponed them). Although the level of investor interest they will attract is still uncertain, the fact that they have many proponents and a smaller market cap compared to Bitcoin suggests they will have a significant impact on the asset's price. After two weeks of more or less significant capital outflows from Bitcoin ETFs, we have returned to a positive trend in recent days, and the launch of similar vehicles for Ethereum could provide a new boost to sentiment.

On Thursday, VanEck went a step further and initiated the process to market a Solana ETF. Certainly, it seems very remote, as the SEC has made it quite clear that it considers Solana (probably rightly) a security, and although the momentum and change in discourse are evident, I see it as highly unlikely that they will greenlight this vehicle. However, with the increasingly likely election of Trump, everything could change very quickly: if he truly champions the crypto cause and replaces Gensler, all bets are off.

The weekly inventory data from the EIA continues to surprise with the significant adjustments shown and the distant relationship with demand and refinery utilization figures, which are positive: +3.591 million barrels of crude oil, -0.226 million barrels in Cushing, +2.654 million barrels of gasoline, and -0.377 million barrels of distillates. Q2 has indeed been weak from a fundamental standpoint for oil, with inventories reversing all the gains made in Q1 and key physical indicators showing a downward trend, which has reversed in the last month, suggesting a very different and bullish reality in Q3. This mixed reality, seemingly consigning prices to trade in a range throughout 2024, has led even prominent figures in the sector, such as Pierre Andurand, to exit the industry and seek greener pastures in other commodities like copper or cocoa.

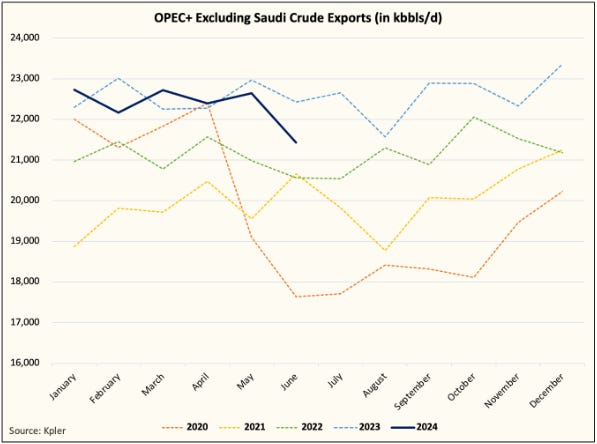

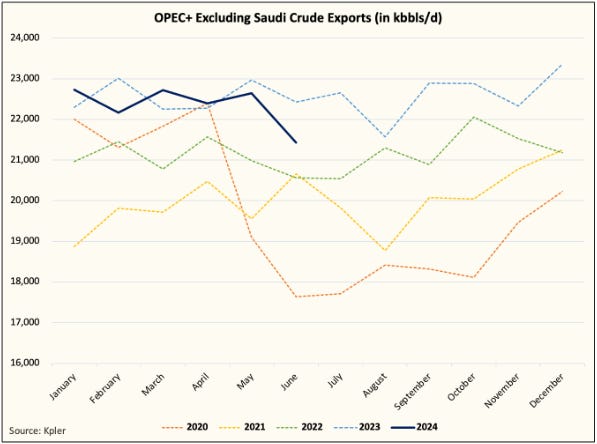

Saudi exports continue to fall (due to domestic consumption and the effect of voluntary cuts), reaching their lowest level since 2020 (5.2 million barrels per day)! The most positive aspect, however, is that the rest of the OPEC members, who have been less compliant with their commitments so far, appear to be changing their stance. The effects of these cuts will take about a month to be reflected in inventories, but this represents a significant supply shock. Real-time production data from the United States shows it is currently at the same level as in Q4 2023, and it is expected to end the year at 13.55 million barrels per day, with a growth of 350kb/d-450kb/d, well below the initial estimates from the EIA. Production is anticipated to peak in 2025 (below 14 million barrels per day), at which point we will see if the much-anticipated peak oil thesis indeed materializes.

Last week, we reported on Ford abandoning its electrification ambitions, but it's not the only manufacturer reconsidering its approach to electric vehicles; Volvo also plans to return to gasoline-hybrid engines due to stagnant demand for electric vehicles. Automakers failed to make profits despite large subsidies, low commodity prices, and low interest rates. The question arises whether they will ever be able to do so... Meanwhile, hybrids, which are a convenient and scalable reality, continue to grow at a pace that already surpasses pure electric vehicles (this fact has many implications for another of our theses, such as PGMs).

Despite the lack of clear catalysts for an increase in oil prices or a significant revaluation of energy stocks, there is much potential in the sector, which trades at very attractive valuations and has a clear path underway to return this value to shareholders. Patience.

Model Portfolio

After three challenging weeks, we have finally returned to a positive profitability trend, with a +1.8% for the week. As we have been emphasizing in recent weeks, fundamentals continue to improve, and it's only a matter of time before price and value (as always, inevitably) converge, especially as we enter the best season, seasonally speaking, of the year. Tomorrow, we will publish a new investment analysis on a special situation in the oil & gas sector for our paying subscribers.

The model portfolio's return is +16.52% YTD compared to +13.81% for the S&P500, and +53.39% versus +35.19% for the S&P500 since inception (September 2022). The model portfolio, as of Friday's close, is as follows:

Keep reading with a 7-day free trial

Subscribe to LWS Financial Research to keep reading this post and get 7 days of free access to the full post archives.