Disclaimer

LWS Financial Research is NOT a financial advisory service, nor is its author qualified to offer such services.

All content on this website and publications, as well as all communications from the author, are for educational and entertainment purposes only and under no circumstances, express or implied, should be considered financial, legal, or any other type of advice. Each individual should carry out their own analysis and make their own investment decisions.

Weekly macro summary

There have been quite a few interesting events to analyze this week, and below I list the most noteworthy news. Let’s get started:

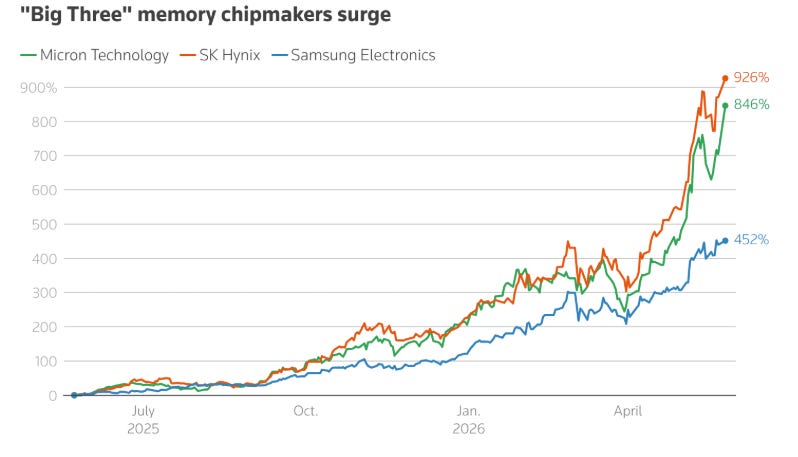

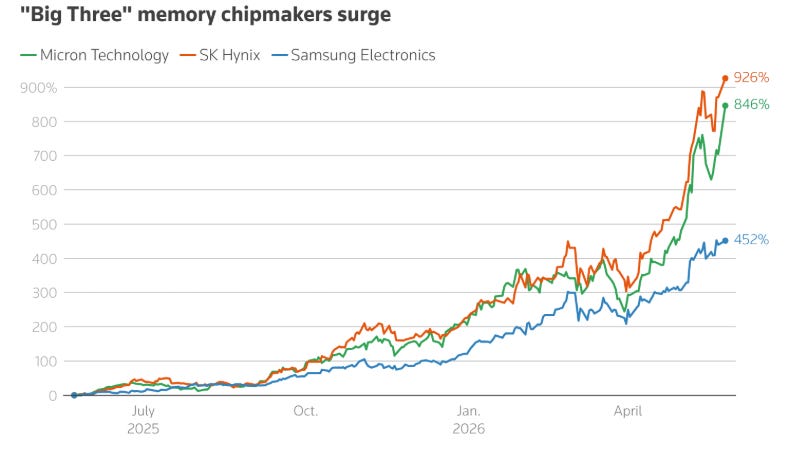

Samsung has managed to avoid a massive strike in its semiconductor business, but the price paid may end up being higher than it initially appears. The agreement reached with the unions, approved by 74% of the workers who voted, allocates 10.5% of the operating profit of the chip division to special bonuses for its employees. On paper, the news removes an immediate risk: a strike by 48,000 workers lasting 18 days, which would have hit not only Samsung, but also the South Korean economy and an already extremely sensitive global chip supply chain.

The problem is that the agreement breaks with a deeply rooted corporate norm in South Korea. Traditionally, bonuses were calculated after taxes and within a more discretionary structure. Here, however, Samsung has committed in writing to distributing a fixed percentage of the operating profit of a specific division. This creates a very uncomfortable precedent, because other unions could use it as a reference point to harden their own demands. It is no coincidence that South Korea’s president, business groups, academics, and even minority shareholders have expressed concern. The line between properly compensating key employees and structurally transferring part of the profit pool from shareholders to workers becomes increasingly blurred.

Artificial intelligence has driven a sharp increase in profits in the memory business, and workers in that division want to capture a proportional share of the cycle. Some employees could receive bonuses close to $416,000 this year, while other areas of Samsung, such as foundry or consumer electronics, will receive much lower amounts. This introduces a significant internal fracture. The same company, the same logo, but a completely different labor reality depending on the division in which one works. In such a large conglomerate, that disparity can erode morale and create management problems deeper than the wage negotiation itself.

Ultimately, Samsung has bought labor peace, but not necessarily stability. The agreement solves the immediate problem, avoids a potentially highly damaging strike, and allows the company to continue competing in the memory cycle. But it also opens a Pandora’s box: more union pressure, greater tensions between divisions, potential shareholder litigation, and a precedent that could spread across the rest of South Korea’s corporate landscape. As often happens in major investment cycles, when an industry starts generating extraordinary profits, the real dispute does not take long to appear: who gets to keep them.

China is executing a much colder and more calculated strategy than the market appears to be pricing in. Amid the tensions in Hormuz, Beijing is not resorting to the usual playbook of releasing strategic reserves to stabilize the market. Instead, it is forcing a much simpler adjustment: reducing imports, cutting refinery utilization, prioritizing gasoline and diesel, and sacrificing the petrochemical chain. The signal is powerful, because a country that has imported close to 11Mb/d in recent years saw its purchases fall to 9.3Mb/d in April, while maritime arrivals in May and June point to extraordinarily low levels, around 6.5Mb/d.

The key point is that China is not willing, at least for now, to open the tap on its strategic reserves. Unlike in other periods of tension, such as the 2021 energy crisis, when the mandate was to secure supply almost at any price, Beijing is now blocking the use of strategic inventories and allowing only adjustments in commercial inventories. But even there, refineries are reluctant to draw down their stocks, while state traders are taking advantage of the situation to resell expensive West African cargoes and accumulate discounted Russian barrels. The equilibrium point lies in refinery utilization. If China tried to maintain the average processing rate of recent years, close to 14.1Mb/d, a drop in maritime arrivals below 9.2Mb/d would quickly force it to choose between drawing on strategic reserves or returning to the international market and paying elevated premiums. That is why the most realistic scenario is a cut in refinery runs of around 5%, to roughly 13.4Mb/d. With domestic production and pipeline flows operating normally, that level would allow China to hold out for several months with maritime imports in the 7.9-8.5Mb/d range without triggering an immediate shock in essential fuels.

The problem is that the early figures for May and June are even below that threshold. If arrivals consolidate near 6.5Mb/d, the 5% adjustment is no longer enough and the system starts to come under physical strain. China could take the cut to 10%, but that would mean entering much more delicate territory: protecting gasoline and diesel at the expense of crushing the availability of naphtha, LPG and other petrochemical feedstocks.

The domestic alternative is coal. China is pushing its Coal-to-Chemicals complex as a strategic shield under the next five-year plan, using cheap and abundant coal to produce olefins and methanol. But this substitute has clear limits. The infrastructure is concentrated in inland regions such as Inner Mongolia, far from the manufacturing heartland of the southeastern coast, which introduces meaningful logistics costs. In addition, coal gasification-based routes cannot replicate the full range of aromatics or the specialized chemical chains linked to LPG. It works as a patch, not as a full substitute for the barrel.

Once again, the risks around the real profitability of artificial intelligence are moving back to the forefront. The market narrative continues to operate under an almost religious premise: AI will be transformational, therefore any investment made today will eventually be justified. But those two ideas are not the same. A technology can be revolutionary and, at the same time, destroy capital for years for those financing the infrastructure required to build it.

The first data points are starting to become uncomfortable. Microsoft has reportedly cancelled a large part of its Claude Code licenses due to cost, Uber has allegedly burned through its entire 2026 AI budget in just four months, and several executives are beginning to publicly acknowledge that costs are harder to justify than expected. There is even talk of companies spending hundreds of millions on tokens because of a lack of usage limits. These are anecdotes, yes, but they all point in the same direction: enthusiasm around adoption is still not translating into clear economic returns.

The problem is that the market appears to be ignoring that second derivative. Stocks remain at all-time highs, while the implied return numbers on AI capex are beginning to deteriorate. According to FT/Panmure Liberum estimates, even under extremely favorable assumptions — revenue against capex, with no operating costs — most hyperscalers would fail to cover their investment between 2025 and 2030. Microsoft, Alphabet, Meta and Oracle would generate negative returns; only Amazon would appear to be positive. And that is before factoring in accelerated GPU depreciation, electricity consumption, salaries, inference costs and technological obsolescence.

That is where the real risk lies. Not in AI “not working”, but in AI working without generating enough profitability to justify the amount of capital being deployed. Hyperscalers are spending historic sums on data centers, chips and energy under the assumption that future demand will catch up with present supply. But that is not a certainty; it is a leveraged bet on the adoption and monetization curve. The comparison with 2000 is not perfect, but it is useful. The internet was real. It changed the world. But that did not prevent a huge amount of the capital invested during the bubble from being destroyed. The infrastructure survived, the users arrived, the winners were extraordinary… but many investors who bought too early, at impossible multiples and extrapolating infinite growth, took decades to recover their money.

AI will probably follow the same pattern. The technology is real, the productivity shift will be real, and there will be enormous winners. But it does not follow from that that every hyperscaler will smoothly earn back its capex, or that any price is justified. For now, the market continues to reward the promise while looking the other way when the bills show up. The relevant question is no longer whether AI will matter. It will. The question is who captures the economic return, when, and how much capital will have been burned along the way.

This is the common picture for oil inventories across almost every region of the world: they are now dangerously close to the minimum operational level required for the system to function. And there is no real possibility of reversing the trend, because, due to the logistics of tanker flows, even if Hormuz were reopened today — which is unlikely — the trend would not change for at least another 2-3 months, by which point the peak summer demand season would already be over.

In fact, market participants seem to believe that everything is fine, based on the fact that crude prices are falling and equity indices are making new highs. Recency bias leads them to assume that, if everything is fine today, it will also be fine tomorrow. The only reason we have not yet seen a rebound and spike in crude prices is the release of strategic reserves, which are acting as a buffer. But that buffer has an expiration date, and it is rapidly approaching. Worse still, it leaves the system even more fragile than it was at the start of the conflict.

Peace headlines keep coming one after another, although none of them has materialized yet, and even Trump seems to be taking the resolution of the conflict for granted. I do think we will see the signing of an MOU soon, but one in which the United States will have conceded on the release of funds and on control of Hormuz, and, of course, where the nuclear issue will not be addressed at all. A total defeat that they are trying to hide at all costs, but where the economic pressure of strangling 20% of global oil flows has carried more weight than ballistics. The opportunity is the most asymmetric one in years.

Model Portfolio

Year to date, the model portfolio is up +25.23%, versus +11.98% for the S&P 500 (S&P in euros), and +222.8% since inception (September 2022), compared with +68.3% for the S&P 500. The model portfolio, as of Friday's close, is as follows:

⚠️Past performance does not guarantee future results. The historical performance of the model portfolio is shown for informational and educational purposes only and does not constitute investment advice or an offer to buy or sell securities. The returns shown may not include fees, taxes, or other associated costs.