Whitehaven coal

(Even more) beautiful clean coal

Disclaimer

LWS Financial Research is NOT a financial advisory service, nor is its author qualified to offer such services.

All content on this website and publications, as well as all communications from the author, are for educational and entertainment purposes only and under no circumstances, express or implied, should be considered financial, legal, or any other type of advice. Each individual should carry out their own analysis and make their own investment decisions.

Introduction and business model

Whitehaven Coal is a producer of thermal and metallurgical coal in Australia, located in the Gunnedah Basin (New South Wales region), with its clients concentrated in Southeast Asia, with Japan (50%), South Korea (14%), and Taiwan (13%) representing the vast majority of its sales for thermal coal, and Europe, China, India, and APAC as its main markets for coking coal. Its assets, with very long production profiles, can provide coal in the coming decades. The company produces the highest quality coal in the export market, both for metallurgical (HCC) and thermal (Newcastle) purposes, which is used in High Efficiency Low Emissions (HELE) plants, which are much more environmentally friendly than traditional generators; in fact, at the end of last year, the company's CEO met with its largest customer in Japan, which already has 3000MW of HELE generation, and plans to replace other older generators with this new technology, which only operates with these coal specifications. There is a certain concentration risk in its customers, as the top three account for 43.4% of total sales.

Most of its production (82%) consisted of high-quality thermal coal (95% >5600kcal, and 40% >6200kcal) last year, but they are carrying out some expansion projects in the metallurgical segment, and recently (on April 2nd) they acquired the Daunia and Blackwater assets, formerly owned by BHP, which has shifted their mix to 70% metallurgical and 30% thermal. Specifically, the company currently operates 5 assets:

Maules Creek: A mine with a production of about 12 million tonnes per annum (Mtpa), of which Whitehaven owns 75%. Much of the production is open-cut, making it susceptible to production issues related to rainfall. The estimated remaining mine life is over 30 years.

Narrabri: A mine with a production of about 11 Mtpa, of which Whitehaven owns 77.5%. Production is improving as the longwall progresses, and with the recent extension approved by the government, the mine life has been extended until 2044. The government has also granted them two exploration licenses that could increase the asset's production.

Gunnedah: Comprised of the Werris Creek and Tarrawonga mines, it produces about 4 Mtpa, and Whitehaven owns 100% of the property. In three years, the operations at Werris Creek will cease (1.5 Mtpa), while the mine life of Tarrawonga (2.5 Mtpa) extends until 2032.

Daunia: Mine with a production of around 6Mtpa of metallurgical coal, with 100% ownership and an expected mine life of 17 years.

Blackwater: Mine with a production of around 14.8Mtpa of metallurgical coal, with 100% ownership and an expected mine life of >50 years.

With the acquisition of these two assets, the company has doubled its production compared to 2023.

In addition to the producing assets, they are developing the Vickery project, which is expected to start production in 2025 (a combination of metallurgical and thermal coal), at a rate of 10 Mtpa (initially 1.5 Mtpa). The Winchester South mine, focused on metallurgical coal, is currently in the study and permitting phase, providing organic growth opportunities. Both assets were acquired from Rio Tinto in 2010 and 2018.

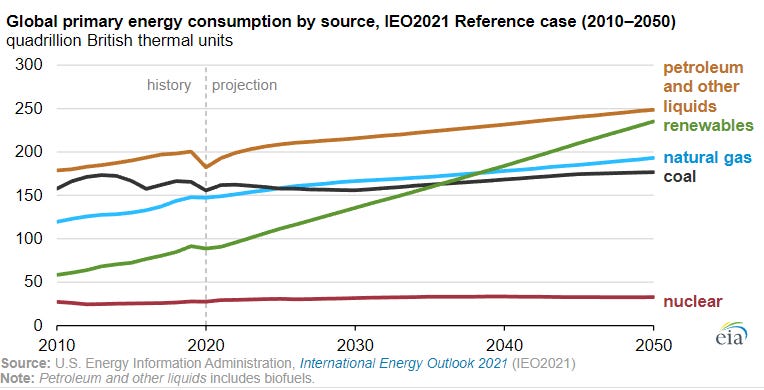

The sentiment in the sector is very negative, with the consensus being that this fossil fuel is in a phase of disappearance. Despite these exaggerated proclamations, we still need coal: we need it for power generation, industrial complexes, and steel manufacturing. These uses are crucial, and the demand will continue to increase until technological innovation finds a greener, cheaper, and more efficient solution for these processes. In the most pessimistic demand projections (from the IEA), contrary to the general belief of imminent ruin, coal demand remains stable for the next 30 years.

Other consulting firms, such as Wood Mackenzie, confirm this view: they expect demand to remain flat until 2030 for thermal purposes, and then begin to slowly decline. Nevertheless, it's better not to view demand as a whole, as there are significant geographical divergences: in developed economies, demand is already in a phase of slow decline, whereas in developing economies (many of which still use less energy-dense sources than coal, such as biomass), demand continues to increase, and at a very high rate; these areas, moreover, are experiencing the highest demographic growth, making them more relevant. By 2030, it's expected that 85% of coal-fired electricity generation capacity will be in emerging economies. However, in 2023, due to the significant increase in shale productivity and the normalization of inventories in Europe and Asia following the mild winter of 2022, the price of natural gas dropped sharply, to the detriment of the competitiveness of thermal coal, leading to the closure of 14GW of capacity in the USA (-41% accumulated since 2010).

The current supply is unable to meet these demand forecasts, and there are significant obstacles to the exploration and construction of new mines, especially in Western jurisdictions (in the USA, for example, coal production remains historically low, greatly affected by shale competition in recent years). Meanwhile, China acknowledges that coal is its most important energy source and is increasing production capacity.

In metallurgical coal, the outlook is even better, and there is currently no economically viable technological substitute for steel manufacturing, making the terminal value of these producers much less uncertain. Over the coming decades, demand is expected to continue growing steadily (aside from occasional bumps inherent in the economic cycle).

Commodity companies tend to be poor investments because when the supply-demand balance is in deficit and prices rise, high returns attract new investment, which eventually unbalances the scale in the other direction, causing price drops and losses to the sector. Coal could be an exception to this cycle, as new supply faces strong barriers to entry due to the difficulty of permits and financing, preventing the typical course of the capital cycle, especially in the metallurgical segment.

Investment thesis

There are many data points that make this company and sector interesting (in fact, they are some of my main positions). My investment thesis in Whitehaven Coal is based on the following two points:

Keep reading with a 7-day free trial

Subscribe to LWS Financial Research to keep reading this post and get 7 days of free access to the full post archives.